With the ever-evolving landscape of investing, finding the best strategies to grow your $2k–$3k can set the foundation for future financial success. Whether you’re a seasoned investor or just tipping your toes into the water, 2026 brings forth innovative avenues that promise high returns and diversified portfolios. In this guide, we’ll unravel the top investment strategies, providing insights on varying options like stocks, bonds, real estate, and cutting-edge tech ventures. Get ready to empower your financial journey with practical tips designed to maximize growth and minimize risk, ensuring your investment decisions are well-informed and strategically sound.

Brief Overview

Discover exciting investment strategies for 2026 to effectively grow your $2k–$3k. This guide highlights diversification benefits, recommending a mix of stocks, bonds, and real estate to mitigate risks while enhancing returns. High-yield savings accounts provide secure, steady growth with easy access, while Roth IRAs offer long-term tax advantages. For short-term goals, money market accounts balance safety with higher returns. Embrace these strategies for a balanced approach that optimizes growth and stability, adapting to your financial goals. Start your journey with our investment guide and take steps toward financial independence.

Key Highlights

- Diversification reduces risk and can enhance growth by spreading investments across various asset classes.

- High-yield savings accounts offer stable returns, ideal for investors seeking safety and growth.

- Stocks and ETFs provide dynamic opportunities with potential high returns, suitable for portfolio diversification.

- Money market accounts offer a blend of safety and liquidity for short-term financial goals.

- A Roth IRA offers tax-free growth and flexibility, complementing long-term investment strategies.

Understanding the Importance of Diversification

Investors often find themselves drawn to the latest investment strategies but may overlook the vital concept of diversification. In today’s volatile market, spreading your investments can be the key to financial security. By putting your $2k–$3k into a well-diversified portfolio, you can reduce risks while aiming for steady returns. This approach doesn’t just safeguard your money but enhances potential growth by capitalizing on multiple asset classes. Delving into why diversification matters and how to diversify effectively can equip you with powerful insights to bolster your financial future.

Why Diversification Matters in Investing

Diversification is a cornerstone of sound investment strategies, especially crucial in the ever-evolving landscape of trading and the stock market. When you diversify, you’re not just buying into a single asset or investment; you spread your budget across various sectors, which can significantly mitigate risk. Imagine investing solely in the technology sector, and a sudden downturn hits, your entire investment could be at stake. By having a mix of investments, such as stocks, bonds, and alternative investments, you minimize exposure to any single market’s volatility.

This strategy ensures that if one area experiences losses, the stability or even growth in others can help cushion the fall. For investors, diversification isn’t merely about safety; it’s about crafting a dynamic portfolio that adapts and thrives in multiple financial conditions. In practical terms, diversifying allows you to engage in strategic investment, capitalizing on different asset classes’ unique growth potentials. The financial jargon may sound complex, but it boils down to a simple philosophy: “Don’t put all your eggs in one basket.”

Moreover, diversification taps into insurance against unforeseen economic shifts. With diverse allocations, your investments become a financial moat, safeguarding your money against volatile events. The key is not just the variety but the synergy between chosen investments, each complementing and enhancing overall portfolio performance. By embracing diversification, you’re not just investing; you’re taking a clear way to reinforce your financial resilience. Whether you’re dabbling in real estate or contemplating limited trading in precious metals, this approach beckons seasoned and new investors alike to hedge effectively against uncertainties and explore compounded growth over time.

How to Effectively Diversify with $2k–$3k

With a $2k–$3k budget, you may wonder how to create a diversified portfolio that effectively balances risk and potential reward. The truth is, even with this modest sum, there’s a robust strategy available. Start by allocating your money intelligently across different asset categories. Consider putting a portion into stocks and funds that mirror the broader stock market; these can provide growth and are a staple in any diversified strategy. Stock market investments offer various entry points, allowing you to buy stocks that are well-positioned for future growth, grounding your portfolio in stability.

Next, think about branching out into bonds or money market accounts, which offer stable, albeit lower, returns while adding a layer of safety to your investment strategy. These financial products act as a cushion during market fluctuations, ensuring your investments have a buffer against volatility. Additionally, think about alternative investments, real estate crowdfunding or REITs can offer intriguing opportunities and act as a hedge against inflation.

Insurance in diversification also comes in the form of different asset classes like commodities or index funds, which can be surprisingly profitable. With commodities, you’re betting on tangible resources, often moving inversely to stocks, providing a beneficial balance. Index funds, tracking specific financial markets or sectors, offer a diverse yet low-maintenance investment approach.

Moreover, leverage online platforms that allow fractional purchase of high-value stocks or digital investment strategies using ETFs, expanding your exposure efficiently without the hefty cost. These innovative tools allow investors to access a broader spectrum of investments, maximizing opportunities within budget constraints. The goal is to craft a diverse portfolio, robust against the whims of market movements, while leveraging each financial product’s unique strengths.

Remember, effective diversification isn’t just about having a mix of investments but curating a well-balanced ensemble that sings in harmony with your financial objectives. By understanding how diverse asset classes interact, you’ll not only protect but also strategically enhance your investment potential. Embrace this diversified approach to safeguard your money’s future and pave the way for growth.

Invest in a High-Yield Savings Account for Steady Returns

If you’re eyeing consistent returns without the volatility of more risky investments, a high-yield savings account could be an ideal fit for your financial strategy. Offering a higher interest rate than traditional savings accounts, these accounts can boost your financial growth with minimal risk. For investors holding $2k–$3k, placing funds into a high-yield savings account can ensure financial security while still benefiting from potential earnings. Let’s explore what makes these accounts an attractive option in 2026, and delve into their benefits for prudent investors seeking stability and growth.

Exploring High-Yield Savings Options for 2026

As interest rates fluctuate in response to monetary policy shifts, high-yield savings accounts stand out as a reliable place for investors to park their funds in 2026. These accounts offer higher returns compared to standard savings accounts, presenting a safe and appealing option for investors prioritizing capital preservation and moderate growth. When you’re investing $2k–$3k, maximizing the yield on every dollar is crucial. High-yield savings accounts can provide returns that consistently outpace inflation, which is a vital factor for preserving the purchasing power of your invested money over time.

One of the key features of high-yield savings is the extreme flexibility they offer. Unlike more complex financial products, you can easily access your funds without penalty. This liquidity is especially beneficial if you’re balancing your portfolio with more aggressive investments that require time to mature. Additionally, these accounts are typically insured by the FDIC up to $250,000, ensuring your money is secure even amid financial uncertainty. This can be a comfort for investors who are cautious about market volatility or those seeking a dependable fallback fund.

For investors planning their 2026 strategies, reviews and ratings of financial institutions are instrumental. Opting for well-rated banks or credit unions that offer competitive bonuses or incentives for opening a high-yield savings account can enhance your returns. Some banks might offer a welcome bonus for new accounts or specific perks for meeting certain deposit criteria, making these opportunities worthwhile for new investors. Conducting thorough reviews of financial services ensures you’re selecting an institution that aligns with your investment goals.

Moreover, in the landscape of 2026, where economic conditions can be unpredictable, having a portion of your portfolio in a stable high-yield savings account provides a buffer against more speculative investments. This account serves as a balancing force within a diversified strategy, offering peace of mind and assuring steady returns. By committing a portion of your $2k–$3k investment to such accounts, you underpin your broader financial plan with a steady, dependable base. Consider high-yield savings accounts an essential part of your financial toolkit, complementing more dynamic investments in stocks and ETFs. This multidimensional approach ensures you’re not just investing but strategically tailoring your portfolio to meet both immediate and long-term financial goals.

Benefits of a High-Yield Savings Account

When thinking about financial security and growth, the benefits of a high-yield savings account are compelling for investors. These accounts offer a blend of security, flexibility, and return on investment (ROI) that can be rare in the volatile financial markets. One primary advantage is the high interest offered, significantly better than the near-zero interest rates of traditional savings accounts. This enhanced interest rate ensures your money is working for you, steadily growing in a low-risk environment over time.

Another standout advantage is liquidity. Investors often gravitate toward liquid financial instruments to maintain the option of accessing their funds swiftly and without restrictions. High-yield savings accounts excel here, offering easy access when needed, ideal for financial goals with uncertain timelines. This liquidity doesn’t compromise earnings, making these accounts a versatile tool for managing cash reserves while planning investments with a longer horizon, such as real estate or stocks.

Safety is a paramount concern for every investor, and high-yield savings accounts answer this with their FDIC insurance, which covers up to $250,000 of your investment, protecting against bank failures. This assurance is invaluable amidst fluctuating market dynamics, acting as a safety net that preserves your financial assets. When diversifying an investment portfolio, blending low-risk financial products with higher returns ensures that you can rely on stable segments of your financial strategy, mitigating risk and enhancing overall performance.

Additionally, the simplicity of managing a high-yield savings account appeals to both new and seasoned investors. Unlike stock market investments requiring constant attention and strategic timing, these accounts offer a “set-it-and-forget-it” nature. This ease of management can be beneficial when diversifying with other investment vehicles that demand more active oversight. Furthermore, leveraging interest calculators can help you map out how your savings grow monthly or annually, providing transparency and investment insights that bolster long-term planning.

Investing in a high-yield savings account can be a wise step within a broader, diversified strategy. By anchoring your financial ventures with a secure and profitable foundation, these accounts provide a dual function of safety and incremental growth. When you balance your approach with high-yield savings, you buffer against market volatility and allow for calculated risks elsewhere in your portfolio. Positioning your financial future with this combination of security and growth not only achieves immediate aims but also fosters sustainable, long-term wealth accumulation.

Maximize Returns with Stocks and ETFs

When it comes to building a solid financial future, stocks and ETFs present some of the most dynamic opportunities for investors looking to maximize their returns. These investment vehicles allow you to participate in market movements, earning potentially higher returns compared to traditional savings accounts. To make the most of your $2k–$3k investment, understanding how stocks and ETFs function is crucial. By comparing these vehicles and learning effective strategies for beginners, you can enhance your financial strategy with both stability and growth.

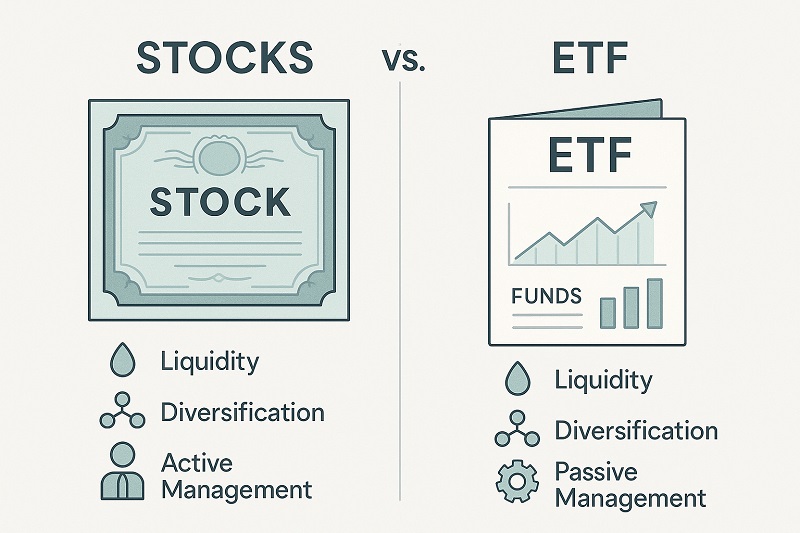

Comparing Stocks and ETFs as Investment Vehicles

Investing in the stock market can initially seem daunting; however, understanding the fundamental differences between stocks and ETFs can demystify the process and unlock strategic opportunities. Stocks represent a piece of ownership in individual companies, meaning when you buy stocks, you’re directly buying a slice of the company’s potential success. Stocks are ideal for investors looking to capitalize on company-specific growth stories, often providing returns that mirror the fortunes of the sector or industry they represent. However, investing in stocks requires thorough research and informed decisions, as individual stocks can be volatile and influenced by myriad market factors.

On the other hand, ETFs, or Exchange-Traded Funds, offer a simpler way to invest by allowing you to buy a collection of stocks bundled together. ETFs mimic the performance of specific indexes or sectors, offering an inherently diversified investment approach, thereby reducing the single-stock risk associated with individual stocks. With ETFs, your $2k–$3k can spread across different industries or geographic markets, effectively diversifying your portfolio without the complexity of managing numerous individual stocks. This diversity forms an integral part of comprehensive investment strategies, allowing investors to mitigate risks while achieving exposure to broader market performance.

For those determined to explore investments but perhaps hesitant about where to start, ETFs offer a user-friendly pathway. With lower capital requirements than buying an equivalent diverse spread of stocks individually, ETFs democratize access to market returns. They provide an automated approach to investing, where fund managers take on the responsibility of maintaining the right balance of assets. This makes them a compelling choice for those looking to balance investing with everyday commitments, providing an accessible entry into the world of stock market investments. For many investors, this relatability to daily financial life is invaluable, splitting the intricate world of stock trading into manageable chunks.

One strategic advantage of ETFs is their adaptability to both passive and active investment strategies, honing in on specific market segments or trends based on your financial goals. ETFs can be easily bought and sold through a brokerage account, just like stocks, offering liquidity and the flexibility to swiftly respond to market fluctuations. By combining stocks and ETFs in your investment strategies, you not only enhance diversification but also blend short-term liquidity with long-term growth potential. For investors, this balanced approach aligns with diversified portfolio planning, maximizing gains while securing against market downturns.

In summary, both stocks and ETFs can effectively contribute to your financial growth, each offering distinct advantages. By weighing the immediacy and potential of individual stocks against the broad, diversified appeal of ETFs, investors can tailor a well-rounded financial strategy that not only aims for resilience against market volatility but also capitalizes on diverse growth opportunities. As you navigate your investment choices, integrating stocks and ETFs can provide a comprehensive framework for achieving your long-term financial goals, ensuring that your $2k–$3k investment is both strategic and rewarding.

Continue by exploring specific considerations when choosing between stocks and ETFs for your investment strategy:

- Assess your risk tolerance to determine the preferred level of investment volatility.

- Evaluate the time you can dedicate to researching and managing investments.

- Examine your financial goals and the timeframe for expected returns.

- Consider the advantages of diversification versus potential for individual stock growth.

- Balance liquidity needs with the desire for potential long-term gains.

- Analyze fees and expenses across different investment vehicles for cost-effectiveness.

- Explore sector-specific interests to align investments with personal interests or ethical beliefs.

These factors will help you align your investment strategy more closely with personal financial goals and preferences.

Tips for Beginners Looking to Invest in Stocks

Embarking on your stock market journey with a $2k–$3k budget might seem challenging at first, but it offers a fantastic starting point to begin your portfolio. For beginners, understanding the stock market’s nuances can make all the difference between a successful investment and a costly mistake. The first step is setting up a brokerage account, which acts as your gateway to buying and selling stocks. Many online brokerage platforms provide user-friendly interfaces tailored for beginners, offering educational resources and tools to assist you in learning how to trade effectively.

Once your account is set up, a crucial tip is to prioritize research over impulsive stock trading. Understanding a company’s fundamentals, such as financial health, market position, and growth potential, can guide your decision-making when opting for stocks to buy. For those new to investing, it might be tempting to chase the latest “hot stock” or succumb to market hype. However, success often lies in patiently building a diverse portfolio grounded in thorough research and strategic planning, rather than speculative foresight.

It’s essential to start investing with a clear financial plan and specific goals in mind. Determine if your focus is on short-term gains or long-term wealth accumulation, as this will influence whether you opt for safer, established companies or growth-oriented stocks. Scaling your investments according to risk preferences can help in aligning your stock purchases with your overarching financial strategy. Additionally, tracking your investments routinely, while being open to adjustments based on market conditions, ensures that your strategy remains dynamic and adaptable.

As a beginner, diversifying within your stock portfolio is a defensive move against potential market downturns. Allocating your budget across multiple sectors can shield you from the impact of sector-specific volatility. This mix fosters stability and provides a broader exposure to potential growth areas within the economy. Furthermore, technological advancements and financial innovations have brought forward themes like digital transformations, which can be particularly lucrative for forward-thinking investors. These sectors can redefine traditional market boundaries, presenting unique investment propositions.

Lastly, continuous learning is a cornerstone of successful stock market investing. Keeping abreast of financial news, understanding economic indicators, and leveraging educational resources can greatly enhance your investment acumen over time. Participating in investor workshops or online forums can provide community support and additional insights into investment strategies that suit your personal finance goals. These combined practices encourage not only confident investing but also foster a mindful approach that recognizes the balance between risk and reward. With patience and thoughtful strategy, investing in stocks can become a rewarding venture, laying the groundwork for financial growth in 2026 and beyond.

Exploring Money Market Accounts for Short-Term Goals

As an investor, when you think of securing your $2k–$3k investment for short-term goals, money market accounts might be just what you’re looking for. These accounts offer a blend of safety and higher yield compared to traditional savings accounts, making them ideal for financial goals that require liquidity paired with some growth. Understanding money market functionalities and best investment practices can bolster your financial strategies, ensuring that your investments remain available yet productive, setting a solid foundation to pursue more aggressive opportunities later on.

Understanding How Money Market Accounts Work

Diving into the mechanics of money market accounts, these financial products strike a balance between savings and investment benefits. For investors, understanding this account’s structure is crucial to aligning it with your savings goals. Money markets often offer higher interest rates compared to regular savings accounts due to their investment strategy, which often involves buying into short-term, low-risk securities like Treasury bills or commercial paper. This ensures that while your money is accessible, it’s also working harder, providing a reliable return on your investment.

One significant appeal of money market accounts is their FDIC insurance. This insurance guarantees protection of up to $250,000, safeguarding your finances against institutional failures, much like other savings deposits. This feature enhances their role as a dependable choice within diversified investment strategies, creating a safety net amidst more volatile financial products like stocks or equity investments. With financial stability as a priority, such assurance brings peace of mind, which is invaluable in unpredictable economic conditions.

However, liquidity is another critical factor in money market accounts. While not as fluid as standard savings, these accounts typically allow investors to withdraw money without penalties or excessive delays. This makes them preferable when compared to certificates of deposit (CDs), where funds are locked for a fixed period. Generally, money markets offer check-writing privileges, further augmenting their flexibility for transactions, which can be strategically useful for investors needing immediate access to money for other financial opportunities.

Nevertheless, while interest rates in money market accounts are not as high as equity investment returns, they offer a stable growth means. For short-term financial goals or when you’re waiting to deploy funds into more aggressive investing options, money market accounts serve as a strategic holding area. They’re a way to keep your money growing while maintaining accessibility, embodying a practical choice for anyone prioritizing both short-term liquidity and gradual growth within their overall investment strategies.

Understanding money market account intricacies will enable you to utilize them effectively within a broader short-term financial framework. As you consider avenues for the $2k–$3k investment, exploring these accounts can offer insight into optimizing fund allocation. For those balancing risk and return, deploying a portion of your funds into these accounts can buffer your financial portfolio, allowing for strategic maneuvers in response to market conditions, ultimately complementing longer-term investment goals.

Best Practices for Investing in Money Market Accounts

Investing strategically in money market accounts requires a clear understanding of your financial goals. As an investor, defining whether you seek accessible funds for emergencies or a cushion to balance riskier investments can drive your approach. Money market accounts can be particularly beneficial for maintaining liquidity while earning a stable interest rate, beneficial when planning for short-term market fluctuations or unexpected expenses.

When looking to invest in a money market account, conducting thorough research into financial institutions is essential. Not all accounts are created equal; some may offer competitive interest rates, while others provide additional benefits or features that suit your specific financial strategy. Scrutinizing account terms, such as minimum balance requirements or associated fees, is pivotal in selecting an account that maximizes your investment return without imposing detrimental constraints on your finances.

Moreover, it’s crucial to periodically review the account’s performance against your financial objectives, ensuring it delivers expected outcomes. Interest rates can fluctuate in response to wider market trends, and keeping abreast of these changes ensures you’re always making the most of your money. If an account no longer meets your needs, re-evaluating and reallocating funds could preserve and enhance investment growth. Taking a proactive stance on managing these accounts aligns with broader financial benchmarks, aiding in achieving both short-term goals and paving the way for wealth creation in the longer term.

Additionally, positioning money market accounts alongside other investments in your portfolio can create a financial synergy. They’re effective as both a buffer and a bridge within a diversified strategy, providing the liquidity to seize new investment opportunities as they arise. This seamless transition supports the overarching goal of financial flexibility, allowing for a dynamic approach to money management as fiscal landscapes evolve.

Investor insights and reviews of account options can further guide choices. Leveraging community forums or consultations with financial advisors can uncover lesser-known perks or potential risks, enhancing account value. This commitment to informed investing reinforces prudent decision-making, balancing short-term needs with aspirational financial horizons.

Ultimately, the key to successfully using money market accounts lies in integrating them within a broader, dynamic investment strategy. By recognizing their role and limitations, you can harness these accounts to stabilize and grow assets. Adaptability and forward planning reinforce your ability to leverage diverse financial products, ensuring your $2k–$3k investment serves both immediate needs and long-term ambitions, paving a sustainable path toward financial prosperity.

Leverage the Power of a Roth IRA for Retirement

Tapping into a Roth IRA can significantly bolster your retirement savings with its tax-free growth and withdrawals. This investment vehicle not only offers a strategic advantage for long-term savings but also provides flexibility unmatched by traditional IRAs. Setting up a Roth IRA involves understanding the nuances of this account type, which presents opportunities for financial growth and security. The benefits for long-term investors are numerous, as you can access your contributions tax-free at any time, creating a secure foundation for your retirement planning. Prepare to unlock the potential of this powerful retirement tool.

Setting Up a Roth IRA: A Step-by-Step Guide

Establishing a Roth IRA can be a straightforward process if you take the right steps and understand the intricacies involved. To start, assess your eligibility based on the IRS’s income limits; it’s essential for maintaining the tax advantages that come with a Roth IRA. Once eligibility is confirmed, choose a financial institution that aligns with your needs. Many banks, investment companies, and online platforms offer Roth IRAs with varying features, including fees and investment options. Compare reviews and features to determine the best fit for your investment strategy.

After selecting a provider, opening your account can usually be done online by filling out a straightforward application. Be prepared to provide personal information, including your Social Security number and bank details, to facilitate future transactions. The next vital step involves determining your initial investment. With as little as $2k–$3k, you can start investing, taking advantage of the compound interest potential over time.

Once your account is open and funded, choose your investments wisely. A Roth IRA can hold various investment vehicles, such as stocks, ETFs, mutual funds, or bonds. Diversify your portfolio to balance risk and maximize potential gains. Many platforms offer tools and educational resources to help you select the right mix of investments that align with your financial goals.

Regular contributions are key to leveraging the full power of a Roth IRA. Keeping in mind annual contribution limits as stipulated by the IRS, ensure that your contributions are consistent and automated if possible. This reinforces disciplined saving habits while capitalizing on the long-term benefits of compounding returns. Lastly, keep track of your investments and performance, adjusting as necessary to align with evolving financial situations and retirement goals.

Benefits of a Roth IRA for Long-Term Investors

The primary appeal of a Roth IRA lies in its tax-free growth and withdrawals, a feature that sets it apart from traditional IRAs. For long-term investors, this translates to potentially substantial savings on taxes, especially if you anticipate being in a higher tax bracket during retirement. Every dollar you contribute now grows tax-free, maximizing your retirement nest egg’s potential.

Flexibility is another standout advantage. Unlike traditional IRAs, a Roth IRA allows you to withdraw your contributions (not earnings) at any time without penalties or taxes. This accessibility offers an additional layer of financial security, serving as a buffer for unforeseen expenses while preserving your retirement savings. Such liquidity is invaluable in maintaining financial peace of mind over time.

Moreover, Roth IRAs do not require mandatory distributions at age 72, unlike traditional IRAs. This means your funds can continue to grow tax-free for as long as needed, providing more control over your financial planning. This feature is particularly beneficial for crafting a long-term strategy, whether you wish to leave a legacy or ensure ample funds throughout a potentially long retirement.

When considering retirement investing strategies, the Roth IRA stands out for its ability to complement other investment vehicles, such as a high-yield savings account or stocks and ETFs. By integrating it into a diversified portfolio, you can buffer market volatility while optimizing for growth and stability. An informed approach with a Roth IRA can significantly bolster your financial resilience, ensuring a robust nest egg for the golden years.

Remember, your financial health in retirement hinges not just on saving but strategically growing your money. A Roth IRA offers the tools for both, underscoring its importance for investors committed to long-term wealth accumulation. As you consider your 2026 investment strategies, capitalizing on a Roth IRA’s benefits could well be a cornerstone of robust financial planning.

Investing $2k–$3k in 2026 offers unique opportunities to grow your wealth, whether you lean towards stocks, peer-to-peer lending, or diversifying via index funds. Each option presents different levels of risk and reward, and the best strategy will depend on your financial goals and risk tolerance. Start small, stay informed, and consider consulting with financial advisors to maximize your returns. For more personalized strategies, download our free investment guide, and get started on your path to financial independence today. Remember, the key to successful investing is consistency and patience.

FAQ: 7 Best Ways to Invest $2k–$3k

What investment strategies are recommended for 2026 with a $2k–$3k budget?

In 2026, consider diversifying across stocks, bonds, real estate, and cutting-edge tech ventures. High-yield savings accounts offer secure growth, while Roth IRAs provide tax advantages. Money market accounts can balance safety with returns for short-term goals.

Why is diversification important in investing?

Diversification reduces risk by spreading investments across various asset classes. This strategy minimizes exposure to any single market’s volatility, ensuring that losses in one area can be cushioned by gains in another.

What benefits do high-yield savings accounts offer?

High-yield savings accounts provide stable returns with minimal risk, offering higher interest rates than traditional savings accounts. They ensure financial security while providing easy access to funds.

How do stocks and ETFs contribute to a dynamic investment portfolio?

Stocks offer growth by investing in individual companies, while ETFs provide diversified exposure to various sectors. Both can enhance portfolio returns by offering high potential growth and liquidity.

What advantages does a Roth IRA provide for retirement planning?

A Roth IRA allows tax-free growth and withdrawals, providing flexibility and security for long-term savings. Contributions can be accessed anytime tax-free, and there’s no requirement for mandatory distributions at age 72.