Managing an inheritance can be both exciting and challenging, especially as you look to grow this financial windfall. While strategizing for the future, it’s crucial to make informed decisions that maximize your returns and align with your personal goals. In this guide, we’ll walk you through seven strategic steps tailored for April 2026 to ensure your inheritance is wisely invested. From understanding your financial objectives to exploring diverse investment options, these insights will empower you to secure your financial future. Let’s embark on this journey to amplify your wealth effectively and responsibly.

Brief Overview

Managing inheritance wisely involves strategic planning to maximize returns and align with personal goals. The guide provides seven steps tailored for 2026, highlighting the necessity of creating a financial plan and understanding timeframes in investment decisions. It’s crucial to assess your financial status, consider tax obligations, and build an emergency fund before diving into investments. Diversifying your portfolio to manage risk and optimizing tax efficiency are essential strategies. Estate planning, with a focus on long-term benefits beyond 2026, ensures your financial legacy is secure. Professional advice and continuous learning further enhance your investment outcomes.

Key Highlights

- Creating a financial plan is essential for effectively managing an inheritance, aligning priorities, and setting realistic goals.

- Assessing current financial status, including building an emergency fund, is critical before investing inheritance money.

- Diversify investments across various asset classes to mitigate risk and enhance returns for long-term growth.

- Understanding tax implications is fundamental to preserving inheritance through strategic planning and tax-efficient investments.

- Developing a comprehensive estate plan ensures financial wishes are honored, protects assets, and provides for future generations.

Understanding the Importance of a Financial Plan

Investing an inheritance requires careful consideration and a robust financial plan. Creating a financial plan provides direction and allows you to set clear goals, especially when managing inheritance money. Before embarking on your investment journey, understanding the essence of financial planning is crucial. This process involves aligning your priorities, setting realistic goals, and preparing for future contingencies. By focusing on these aspects, you ensure that your personal finance decisions are well-informed and purposeful. Let’s delve deeper into how to kickstart your financial planning and explore the role of timeframes in your investment strategy.

How to Start Creating Your Financial Plan

When managing inheritance, one of the first steps is to establish a comprehensive financial plan. This task might seem daunting, especially if you’re new to personal finance, but breaking it down into manageable steps can simplify the process. Begin by assessing your current financial status. This includes analyzing your income, expenses, assets, and liabilities. Knowing your starting point is vital for informed decision-making and helps you outline a realistic approach to wealth management.

Next, define your financial goals. Whether it’s saving for retirement, buying property, or funding education, having clear objectives will guide your investment choices. Prioritize these goals based on your personal values and timeframes, as this will influence your investment strategy. For instance, short-term goals might necessitate more liquid, low-risk investments, while long-term aspirations might allow for more aggressive growth opportunities.

Consulting a financial advisor can be a wise step in this journey. With their expertise in wealth management and financial planning, they provide insights that can optimize your investment strategy. A financial advisor can help you navigate complex fiscal landscapes, draft a personalized plan, and reassess your approach as circumstances change. This professional guidance is particularly beneficial when dealing with inheritance, as it often involves substantial sums and intricate tax considerations.

Moreover, developing a budget is crucial in this phase. It ensures that your daily expenses align with your broader financial plan, helping you avoid unnecessary spending and encouraging disciplined investing. A well-crafted budget acts as a blueprint, keeping your personal finance journey on track.

Lastly, consider insurance and risk management. Protecting your assets against unforeseen events is a critical component of financial planning. Assess your insurance needs and adjust your coverage accordingly to safeguard your inheritance and investment portfolio.

Whether it’s life insurance, health insurance, or property coverage, having adequate insurance plays a pivotal role in your overall strategy.

Starting your financial plan with these components lays a solid foundation for your wealth management journey. By taking a strategic and informed approach, you ensure that your inheritance is invested wisely, setting the stage for financial growth and security. Engaging with a professional and adhering to a disciplined budget are just the starting points in transforming an inheritance into long-term wealth for yourself and your family.

Building a solid financial foundation is crucial when managing an inheritance. Here are some essential steps to help you start a successful financial plan:

- Conduct a thorough assessment of your current financial situation to identify strengths and weaknesses.

- Define clear financial goals for both short-term needs and long-term wealth growth.

- Consult with a financial advisor to explore diverse investment opportunities that align with your objectives.

- Educate yourself on tax implications to optimize your inheritance and minimize liabilities.

- Create a comprehensive budget to ensure all expenses are well-managed and aligned with your financial goals.

- Consider setting up an emergency fund to safeguard against unforeseen financial challenges.

- Regularly review and adjust your financial plan to accommodate life’s changes and market fluctuations.

- Incorporate estate planning to preserve wealth for future generations and fulfill your legacy wishes.

By taking these proactive steps, you can effectively integrate your inheritance into a solid financial plan, ensuring sustained growth and security for your financial future.

The Role of Timeframes in Investment Decisions

Timeframes are fundamental to crafting an effective investment strategy, especially when managing inheritance. Understanding your investment horizon is key to balancing risk and reward, ultimately guiding your financial decisions. Short-term timeframes generally span less than three years, and during this period, it’s crucial to focus on stability. Investments such as bonds or money market funds can offer lower risk and predictable returns, making them ideal for preserving capital.

For those with a medium-term timeframe, typically three to ten years, investments can be slightly more adventurous while still incorporating elements of security. Here, you might consider diversified portfolios that blend stocks and bonds. This approach allows for some growth potential while maintaining a level of stability, making it a balanced option for investors seeking moderate gains.

Long-term timeframes, which exceed ten years, present opportunities to invest in assets with higher growth potential. Historical data shows that the stock market generally outperforms other asset classes over long periods, despite its inherent volatility. This makes equities an attractive option for long-term investors looking to maximize returns on their inheritance. Understanding the market trends and leveraging compounding interest can substantially increase your wealth over decades.

Your personal circumstances and risk tolerance also play a significant role in defining your timeframe. For instance, younger investors with an inheritance might be inclined towards longer time horizons, allowing them to take on more risk with the promise of greater rewards. Conversely, those nearing retirement may favor shorter timeframes to preserve capital and ensure liquidity.

Aligning timeframes with life goals is another critical aspect of investment decision-making. Significant life events, such as retirement, purchasing a home, or funding a child’s education, should influence your investment horizons. Planning around these milestones will ensure that your financial plan remains relevant and adaptable to changing needs.

It’s essential to revisit and adjust these timeframes regularly. Market conditions, life circumstances, and financial goals evolve over time, necessitating periodic reviews of your strategy. The role of a financial advisor becomes invaluable here, as they can provide objective insights and adjustments to your investment plan, ensuring alignment with your timeframes and goals.

Timeframes impact not just investment risk, but also the liquidity of your assets. Striking a balance between accessible resources and locked-in investments is crucial for flexibility and security in your financial plan. Ultimately, understanding and effectively managing timeframes helps in making informed investment decisions, maximizing the return on your inheritance while safeguarding its value across different life stages.

Assessing Your Financial Status

After understanding the importance of a financial plan, it’s crucial to assess your financial status to effectively manage your inheritance. Knowing your current financial standing provides a foundation for making informed investment decisions and avoiding potential risks. This assessment involves building an emergency fund to safeguard against unforeseen expenses and calculating what you’ll owe in taxes. These steps ensure that your personal finance is organized and prepared for any challenges ahead. Let’s explore the importance of establishing an emergency fund and understanding your tax obligations.

Building an Emergency Fund Before You Invest

Building an emergency fund is an essential step in financial planning, especially when you’re about to invest your inheritance. This fund acts as a safety net during financial emergencies, preventing the need to liquidate investments prematurely, which could lead to losses or tax implications. Ideally, your emergency fund should cover three to six months’ worth of living expenses, providing peace of mind and flexibility in difficult times.

To start, assess your monthly expenses to determine a reasonable amount for your fund. This involves scrutinizing costs such as rent, groceries, utility bills, and any recurring payments. Financial planning is not just about securing future wealth; it’s also about managing current expenses to maintain your standard of living even when unforeseen events arise. Building an emergency fund aligns with prudent personal finance strategies, ensuring you’re prepared without derailing your broader financial goals.

Consider setting up a dedicated savings account specifically for this purpose. High-yield savings accounts or money market accounts can be excellent options as they offer accessibility combined with better interest rates than traditional accounts. Make regular contributions to this fund from your primary income or returns from other safe investments. Budgeting for this fund should be a top priority in your financial plan, allowing you to invest inheritance money with greater confidence.

The importance of having an emergency fund cannot be overstated when you’re beginning to invest. It reduces the emotional burden during market fluctuations, allowing you to focus on long-term financial objectives. Moreover, having this buffer can support strategic decision-making, such as holding onto investments until they appreciate rather than selling in haste during unforeseen financial challenges.

Building an emergency fund is not just a task to check off. It reflects a proactive approach towards managing risk and securing financial stability. Without it, you’re more vulnerable to falling behind on bills or accumulating debt during emergencies. Engaging with a financial advisor can give further insights into determining the ideal fund size tailored to your personal circumstances, thereby enhancing the resilience of your financial plan.

Calculating What You’ll Owe in Taxes

Understanding what you’ll owe in taxes is a fundamental part of managing your inheritance efficiently. Tax liabilities vary depending on factors such as the size of the inheritance, where you live, and the type of assets inherited. To invest tax-efficiently, it’s crucial to comprehend how inheritance tax, income tax, and capital gains tax can impact your financial status. This knowledge is vital in avoiding unexpected tax bills and optimizing your investments.

Start by familiarizing yourself with local and federal inheritance tax laws. Some regions impose their own inheritance tax, adding to the complexity of financial planning. Knowing these details allows you to plan your finances accordingly, ensuring you’re not blindsided by hefty tax debts. Employing tax planning strategies is essential to manage these liabilities efficiently, enabling you to maximize the inheritance benefits.

Seeking the expertise of a tax advisor or accountant can be invaluable in this process. They can provide personalized advice on how to navigate tax landscapes, ensure compliance, and identify areas where you can legally reduce tax burdens. These professionals can help you explore options such as trusts or gifting strategies that can effectively manage or defer taxes on inheritances.

Further, investments that you’re considering post-inheritance will also have tax implications. Understanding capital gains tax, for instance, is crucial when selling any inherited property or assets. Tax-efficient investing involves choosing assets that align with your investment strategy while also considering their tax impact. This can include focusing on tax-advantaged accounts or investments like IRAs and 401(k)s, where potential tax liabilities are deferred or lowered.

In terms of real estate, if inherited, calculating its fair market value as of the date of death is essential, as this could affect future capital gains tax when you decide to sell. Awareness of this can significantly affect your decision on whether to sell or hold onto the property as part of your investment portfolio.

Ultimately, understanding what you’ll owe in taxes helps prevent the erosion of your inheritance through inefficient tax management. It empowers you to make informed decisions about how to allocate funds, which investments to pursue, and when to execute transactions. This proactive approach not only enhances your financial standing but keeps your investment plans aligned with your overall financial goals. Engaging in comprehensive tax planning fortifies the foundation laid by previous financial planning steps and equips you to manage your inheritance with confidence for the long term.

Strategies to Invest Inheritance Effectively

When you invest inheritance money, it’s all about strategic thinking and planning for both immediate gains and long-term security. To invest smartly in 2026, it’s crucial to consider how taxes can impact your decisions, as well as how diversifying your portfolio can help manage risk. These strategies will not only help maximize your financial growth but also ensure that your investments remain resilient in fluctuating markets. By investing tax-efficiently and embracing a diversified investment strategy, you can transform your inheritance into a lasting legacy.

How to Invest Tax-Efficiently in 2026

Investing tax-efficiently in 2026 means understanding and navigating the complex landscape of taxes to preserve as much of your inheritance as possible. To begin, awareness of the tax regulations applicable to inheritance is vital. Given the intricacies of tax laws that can change frequently, staying updated is crucial. It’s beneficial to familiarize yourself with both federal and state tax obligations, as differences can greatly affect your financial planning.

Engaging with a tax advisor is not just a smart move; it’s indispensable in this scenario. These professionals can help you comprehend inheritance tax ramifications, whether your concern is federal estate taxes or more localized levies. Utilizing their expertise can aid in identifying potential exemptions and planning strategies that align with current laws. They might suggest placing parts of your inheritance into tax-advantaged accounts, such as IRAs or 401(k)s, which can offer deferrals or reductions in tax liabilities.

Moreover, explore the potential benefits of setting up trusts. Trusts can be a powerful tool for tax-efficient investing. They not only help manage taxes but also provide additional control over how and when the inheritance is distributed. Specific trusts, like irrevocable trusts, can remove assets from your taxable estate, potentially lowering your future tax burdens.

Investments themselves need careful consideration regarding tax efficiency. Prioritize assets that offer favorable tax treatment. For instance, municipal bonds are often appealing due to their tax-exempt status at the federal level and potentially at the state level, depending on where you live. Such assets contribute to a diversified investment strategy with the added benefit of tax savings.

It’s also wise to manage capital gains tax effectively. This involves being strategic about when and how you sell investments to avoid unnecessary tax hits. Implementing a buy-and-hold approach can defer capital gains, while periodic reviews can ensure alignment with your broader tax planning objectives.

The evolving digital asset space in 2026 also presents opportunities for tax-efficient investing. Cryptocurrency investments continue to mature, offering varying degrees of tax implications. Understanding how these assets fit into your investment strategy and their tax considerations is essential for future-proof financial planning.

Ultimately, investing tax-efficiently means keeping more of your inheritance working for you. By planning your taxes meticulously, you ensure that the wealth you’ve inherited is optimized for performance, safeguarding it against unnecessary drains. This approach not only enhances financial growth but also supports a sustainable investment strategy that aligns with your long-term financial goals.

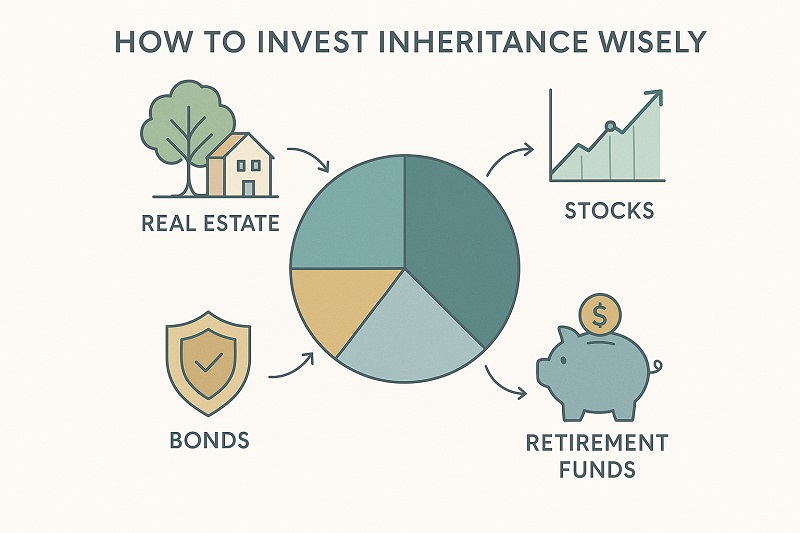

Divide Your Investments to Manage Risk

Implementing a diversified investment strategy is essential when you aim to invest inheritance money while managing risk effectively. Diversification involves spreading your investments across various asset classes to mitigate risk and enhance returns, making this approach crucial for any investor looking to maximize their inheritance’s potential.

Begin by understanding the broad categories of investments available: stocks, bonds, real estate, and alternative assets. Each class differs in risk and reward potential. Stocks, for instance, offer growth opportunities but come with market volatility. Conversely, bonds typically provide steady income but with lower returns. By allocating your inheritance across these different classes, you balance the growth potential of more volatile investments with the stability of safer ones.

Constructing a diversified portfolio involves more than just picking various asset classes. It requires a strategic approach to how you split your assets within each class. In the world of stocks, diversification could mean investing in a mix of industries or geographies. An undercurrent of emerging market stocks might offer high growth potential, while stable blue-chip stocks provide reliable dividends. This alignment ensures your portfolio is equipped to weather economic shifts.

Consider real estate investments as a means to add tangible assets to your portfolio. Investing in property can provide consistent rental income and long-term capital appreciation. Real estate investment trusts (REITs) offer a less capital-intensive entry into property investing, providing exposure to multiple property types and diversified markets without the demands of direct property management.

Alternative investments like commodities, hedge funds, or even digital currencies are becoming a staple in modern portfolios. While these carry higher risk, they can offer diversification benefits, especially since they sometimes move independently of traditional markets. Exploring avenues like gold, which is often seen as a safe haven in tumultuous economic times, can further solidify your diversified investment strategy.

Moreover, actively managing your investments by regularly reviewing and adjusting your portfolio is a critical component of managing risk. Engage with financial advisors to understand the market trends and make informed adjustments to your investments. Their input is invaluable for identifying when to rebalance your portfolio, ensuring it remains aligned with your risk tolerance and investment objectives.

Embrace the concept of diversification beyond traditional boundaries by considering asset allocation strategies that fit specific goals and timeframes. For instance, using a barbell strategy where you invest in very low-risk and very high-risk assets simultaneously could potentially offer stability while capturing substantial upside.

In summary, a diversified investment strategy acts as a safety net, protecting your inheritance from market fluctuations. By wisely structuring your investments across various sectors and assets, you’re not only mitigating potential losses but also positioning your portfolio for consistent growth. This prudent approach ensures the money you’ve inherited continues to thrive, regardless of market conditions, securing a robust financial future.

Estate Planning Considerations

Having a solid estate plan is essential not only for managing your inheritance wisely today but also for securing long-term success. With careful estate planning, you’ll ensure that your wealth management and financial planning efforts are in the right direction, catering to both personal and familial needs. We’ll delve into how developing a comprehensive estate plan can significantly benefit your heirs and why considering the long-term aspects of estate planning beyond 2026 is crucial. Estate planning isn’t just about today; it’s setting the foundation for enduring financial health and stability.

Developing a Comprehensive Estate Plan

Creating a comprehensive estate plan is not just a legal requirement; it’s a crucial step in wealth management that ensures your financial wishes are honored both now and in the future. An estate plan involves more than just drafting a will, it requires careful thought about how to distribute your wealth, taking into account the financial planning needs of your heirs. As an investor, you know that the markets are unpredictable, and the same applies to life events. Developing a robust estate plan can offer peace of mind, knowing that your financial affairs are organized and protected no matter what comes your way.

Central to any effective estate plan is a thorough understanding of your current financial situation. Start by cataloging your assets, including investments, real estate, and any significant possessions. This inventory serves as the foundation of your estate plan and provides clarity on what there is to distribute. It’s vital to align this with your estate planning goals, whether that’s wealth preservation, providing for your family, or supporting charitable contributions.

Incorporating a living trust into your estate plan is a savvy move to consider. A living trust can help bypass probate, ensuring your estate is settled swiftly and privately. This is particularly advantageous for investors with substantial portfolios, where probate delays could affect market-tied assets. Additionally, trusts can control how and when your heirs receive their inheritance, safeguarding potential windfalls from premature or imprudent spending.

Consider a durable power of attorney and a healthcare proxy as part of your estate plan. These documents allow trusted individuals to manage your financial and healthcare decisions if you’re incapacitated. They provide an additional layer of security, ensuring your intentions are respected during critical times. As you move through life stages, it’s essential to revisit and revise your estate plan periodically. The plan should evolve as your circumstances and goals change; perhaps you’ve amassed additional assets or your family dynamics have shifted.

Engaging with an expert in estate planning can provide invaluable insights. An estate planner can guide you through complex tax regulations and offer strategies for minimizing your estate taxes. With their guidance, you can ensure that more of your inheritance is preserved for your heirs, enhancing your overall wealth management strategy.

As 2026 approaches, consider how evolving financial and legal landscapes might impact your estate planning. Investors must remain adaptable, revisiting their plans with new economic realities in mind. By prioritizing estate planning, you’re not simply managing your legacy; you’re actively shaping it to benefit your heirs confidently and sustainably.

Long-term Benefits of Estate Planning Beyond 2026

While immediate financial considerations may dictate the initial formation of an estate plan, it’s the long-term benefits of estate planning that truly underscore its importance. As investors, appreciating how estate planning can extend its impact far beyond 2026 grants a clearer view of its value proposition. In a constantly evolving economic environment, having established controls and contingencies can significantly influence the financial stability of heirs.

At its core, estate planning ensures continuity in wealth management. This facet is indispensable when considering the growth potential of your investments post-2026 and the implications for estate beneficiaries. A well-structured estate plan protects assets through legal mechanisms like trusts, shelters wealth from potential mismanagement, and aligns with the evolving market trends that dictate future financial opportunities.

Consider the tax implications and savings as a cornerstone of long-term estate planning benefits. By strategically structuring your estate plan with tax efficiency in mind, you preserve more wealth for subsequent generations. Techniques such as gifting assets during your lifetime can reduce the estate’s taxable footprint, allowing for more control over asset allocation among heirs. Another benefit is effective liquidity management, preventing the need for estate liquidation to cover taxes.

Furthermore, estate planning can encompass elements of philanthropy, which reinforce the impact of your wealth beyond personal and familial boundaries. Establishing charitable trusts or foundations can fulfill personal philanthropic goals while also offering tax advantages. This presiding commitment to philanthropy resonates long-term, fulfilling the dual objectives of giving back and fostering economic benefit.

An often-overlooked advantage of strategic estate planning is its potential to educate heirs about financial responsibility. By involving family members in your planning process, you create opportunities for financial literacy and preparedness. This dialogue can impart an understanding of fiscal discipline, investing prudently, and recognizing the importance of maintaining and growing inherited wealth.

As 2026 nears, there will be unique economic paradigms and investment opportunities. A forward-thinking estate plan should remain adaptive, with provisions that accommodate changing financial landscapes. Leveraging financial advisors to periodically reassess your plan ensures it is as resilient as your investment portfolio.

Ultimately, estate planning transcends mere financial preparation; it is an enduring strategy that safeguard’s an investor’s legacy, provides for heirs, and accommodates future growth potentials. This approach allows for a robust, responsible wealth transfer mechanism that aligns with one’s values and financial foresight. As you focus on investing your inheritance today, keeping an eye on the future through comprehensive estate planning ensures you optimize not just current assets but also the far-reaching impacts of your financial legacy.

Making wise investment decisions can significantly impact how your inheritance grows over time. By methodically following these seven smart steps, you’re well-positioned to create a robust portfolio that aligns with your future goals. Remember, seeking professional advice and continuously educating yourself on market trends can bolster your investment strategy. With prudent planning and attention to detail, you’re setting the groundwork for a secure financial future. Don’t let this opportunity go to waste, start crafting your legacy today and make the most out of your inheritance.

FAQ: How to Invest Inheritance Money

Why is creating a financial plan crucial for managing an inheritance?

A financial plan provides direction and allows you to set clear goals, especially when managing inheritance money. It helps align your priorities, set realistic goals, and prepare for future contingencies. You ensure that your personal finance decisions are well-informed and purposeful.

What steps should you take before investing your inheritance?

Before investing, assess your current financial status, build an emergency fund to cover unforeseen expenses, and understand your tax obligations. These steps ensure that your financial situation is stable enough to support investment endeavors without unexpected hurdles.

How does diversifying investments help in managing an inheritance?

Diversifying your portfolio involves spreading your investments across various asset classes to mitigate risk. This approach enhances returns and ensures your inheritance is protected against market volatility, increasing the potential for long-term growth.

How important is understanding tax implications when managing inheritance money?

Understanding tax implications is crucial to preserving inheritance. Strategic planning and tax-efficient investments help avoid unexpected tax bills and optimize your finances. Knowledge of local and federal tax laws helps you plan effectively, saving money and maximizing your returns.

What role does estate planning play in securing a financial legacy?

Estate planning ensures that your wealth management and financial intentions are honored over the long term. It includes creating trusts, wills, and other legal mechanisms that safeguard assets and support future generations, aligning with both personal and familial needs.