In the shadowed halls of the State Department, far from congressional oversight and public scrutiny, President Trump has quietly engineered the most significant monetary transformation in over half a century — the birth of America’s Silicon Dollar, a bold reset poised to reshape global finance and create a new generation of millionaires for those who act decisively.

The Silent Revolution Reshaping Global Finance

In the quiet corridors of power, away from the glare of congressional debates and Senate votes, a profound transformation is underway that could redefine the very foundation of American economic supremacy for generations to come. Porter Stansberry, the renowned financial researcher and founder of Stansberry Research, has stepped forward with a compelling analysis that connects decades of monetary history to the urgent realities of today’s technological landscape. What he describes is nothing less than the birth of a new monetary order—the Silicon Dollar—poised to succeed the venerable but fading petrodollar system that has underpinned global trade since the 1970s.

This shift, orchestrated under President Trump’s leadership through executive actions, strategic alliances, and massive private-sector mobilizations, represents far more than a policy tweak. It is a deliberate, multi-trillion-dollar pivot designed to anchor the U.S. dollar to the indispensable physical resources powering the artificial intelligence revolution. For everyday investors, understanding this transition is not optional; it could mean the difference between thriving amid unprecedented wealth creation or watching purchasing power erode as the old rules give way to the new. Stansberry’s insights, drawn from meticulous research and a proven track record of spotting pivotal market moments, offer a roadmap for those ready to position themselves on the winning side of this historic divide.

Imagine a world where the currency that dominates global commerce is no longer tied primarily to black gold extracted from distant deserts, but to the intricate matrix of minerals, semiconductors, energy systems, and data infrastructure that makes modern AI possible. This is the vision Stansberry articulates—one where nations seeking technological leadership must engage with American-controlled supply chains, thereby sustaining demand for the dollar in ways that echo, yet surpass, the petrodollar era. As someone who has guided hundreds of thousands of subscribers through major economic inflection points, from the dot-com boom to the financial crisis and beyond, Stansberry emphasizes that those who grasp these dynamics early stand to build lasting prosperity for their families.

The urgency cannot be overstated. With foreign nations diversifying away from U.S. Treasuries, central banks stockpiling gold, and the original petrodollar arrangements expiring without renewal, the window for proactive positioning is narrowing. Yet, as Stansberry points out, this apparent vulnerability is being met with bold innovation. By December 2025, key international agreements had already been inked, setting the stage for a public unveiling that could accelerate capital flows into specific sectors. Readers who subscribe to forward-thinking research services like those from Porter & Co. gain exclusive access to detailed briefings, such as The Silicon Dollar Playbook, that translate these macro shifts into actionable investment ideas—often at introductory prices that make professional-grade analysis accessible.

This comprehensive article delves deeply into Stansberry’s thesis, expanding on the historical parallels, geopolitical maneuvers, technological underpinnings, and specific investment opportunities. It aims not merely to inform but to empower you with the knowledge needed to navigate what may prove to be one of the most lucrative eras in financial history. By the end, you’ll understand why subscribing to expert guidance could be one of the smartest financial decisions you make this year.

Rewinding to 1974: The Birth of the Petrodollar and Its Enduring Impact

To fully appreciate the magnitude of the emerging Silicon Dollar, it is essential to revisit the events of July 1974, when the U.S. dollar found itself adrift following President Nixon’s decision to abandon the gold standard. In a move shrouded in secrecy, Treasury Secretary William Simon embarked on a diplomatic mission that would reshape global finance. His true destination was Jeddah, Saudi Arabia, where he proposed a groundbreaking pact to King Faisal. Saudi Arabia would price its oil exports exclusively in U.S. dollars and recycle the resulting revenues back into American Treasury securities. In return, the United States pledged military protection for the kingdom.

This arrangement, conceived with input from Henry Kissinger, was elegant in its simplicity and revolutionary in its consequences. Oil, the lifeblood of the modern industrial economy—consumed at a rate of approximately 100 million barrels per day—became the anchor for dollar demand. Every nation needing energy had to acquire dollars, creating a perpetual global appetite for the currency. The inflows financed U.S. deficits, fueled domestic growth, and positioned America as the indispensable architect of the postwar economic order.

The results were staggering. Fortunes were minted not only in oil majors like ExxonMobil and Chevron but across interconnected sectors. Banks such as JPMorgan and Goldman Sachs became conduits for these capital flows. Defense giants like Lockheed Martin and Raytheon benefited from arms deals funded by petrodollars. Industrial and tech leaders—General Electric, Caterpillar, IBM, Microsoft, and Apple—expanded into a world awash with cheap liquidity. According to Federal Reserve data referenced in Stansberry’s analysis, the number of U.S. millionaires exploded from roughly 180,000 in 1974 to nearly 24 million today, a more than 130-fold increase. The S&P 500 delivered approximately 100-fold returns over the subsequent five decades, creating what many consider the greatest bull market in history.

Yet, as Stansberry meticulously details, this success carried a profound shadow side. The “exorbitant privilege” of dollar dominance fostered fiscal complacency in Washington. Unlimited borrowing seemed sustainable because global demand for dollars appeared inexhaustible. The inevitable consequence was monetary debasement: from 1974 to the present, the U.S. dollar has lost more than 84% of its purchasing power. A grocery bill that cost $100 in the mid-1970s now exceeds $600. This erosion disproportionately harmed diligent savers who held cash or relied on fixed-income assets, while those invested in appreciating equities, real estate, and commodities captured the upside.

The wealth divide became entrenched. Today, the top 10% of Americans own about 93% of stock market wealth. Families who owned productive assets rode the wave of globalization and cheap capital. Those who did not—despite hard work and prudent saving—found themselves on the losing side of a generational shift. Stansberry’s message resonates deeply here: understanding monetary resets is not an academic exercise but a practical necessity for protecting and growing family wealth. His own journey, from lifeguarding at Disney World to building one of America’s largest independent financial research firms, underscores the power of timely insight. Subscribers to his services have benefited from calls like Amazon at $3, Qualcomm at $4, warnings on Fannie Mae and Freddie Mac ahead of 2008, and inflation predictions during the COVID era.

As the petrodollar system matured, it enabled America’s geopolitical heft but also sowed seeds of its own challenge. Over-reliance on this arrangement led to unprecedented debt levels, now exceeding $39 trillion, and vulnerability to de-dollarization efforts by BRICS nations and others. China has reduced its Treasury holdings by over 45% from peaks, while central banks globally have accelerated gold purchases. The original deal’s expiration in June 2024 passed without renewal, signaling a tectonic change.

Signs of the Petrodollar’s Demise and the Imperative for Renewal

The erosion of the petrodollar is not happening in isolation. Stansberry points to a confluence of indicators that paint a picture of systemic strain. Foreign dumping of U.S. debt, while fluctuating (with a notable surge in holdings recently to near-record levels), reflects broader diversification trends. Jim Rogers and Ray Dalio, titans of macro investing, have warned of the breakdown in the existing monetary order, drawing parallels to the declines of previous reserve currencies throughout history.

Empires, from ancient Rome to Great Britain, typically overextend through debt and currency debasement before losing creditor confidence. The U.S. faces similar pressures, compounded by geopolitical tensions, including conflicts that highlight energy and resource vulnerabilities. Yet, Stansberry argues persuasively that this is not destined to end in collapse. Instead, proactive leadership is engineering a successor system tailored to the 21st century’s defining technology: artificial intelligence.

This reset is already manifesting in confusing headlines—trade wars, tariffs on semiconductor giants like TSMC (prompting $250 billion in U.S. commitments), renewed interest in obscure metals, nuclear plant restarts, and high-profile summits with tech CEOs like Sam Altman, Larry Ellison, Mark Zuckerberg, and Jeff Bezos. These are not random events but coordinated elements of a strategy to secure the “AI matrix.” Stansberry’s research reveals how executive orders, national security declarations, and bilateral deals are bypassing traditional legislative channels to mobilize resources at wartime speed, reminiscent of FDR’s industrial conversions in the 1940s.

For investors, the implications are immense. Just as the petrodollar redirected capital into specific choke points, the Silicon Dollar promises to do the same—only faster and on a larger scale. Trillions in projected infrastructure spending, including over $400 billion already committed by major tech firms for data centers (rising to $650 billion in 2026), dwarf historical projects like the Apollo program or the interstate highway system. Those positioned early, through informed subscriptions to research like Stansberry’s Silicon Dollar Playbook, can capture this flow before mainstream awareness drives prices higher.

Unveiling Trump’s Silicon Dollar: Pax Silica, FORGE, and the G20 Catalyst

At the heart of this strategy lies Pax Silica, signed on December 12, 2025, by representatives from 13 nations in a State Department ceremony. Named evocatively after the Pax Romana—the era of Roman peace and trade dominance enforced by infrastructure and law—this initiative establishes a coalition for secure technology supply chains encompassing minerals refining, energy, semiconductors, advanced manufacturing, and AI infrastructure. Under Secretary of State Jacob Helberg has articulated its core objective: the nation controlling AI’s industrial foundations will lead the century.

Complementing Pax Silica is the FORGE Alliance (Forum on Resource Geostrategic Engagement), launched in early 2026 with participation from dozens of countries and mobilizing $30 billion in critical minerals investments on day one. FORGE succeeds earlier partnerships like the Minerals Security Partnership, focusing on policy coordination and project-level execution to build resilient supply chains free from adversarial dominance.

These frameworks are not abstract diplomacy. They translate into tangible actions: tariffs pressuring supply chain reshoring, government equity stakes in domestic mining firms such as MP Materials and Lithium Americas, rollbacks on certain climate policies to prioritize energy security, and massive deals channeling private capital—potentially $3 trillion combined from tech and international partners—into American AI infrastructure. Pressure on mineral-rich regions, from Greenland to Canada and beyond, underscores the resource focus.

The December G20 summit at Trump’s Doral Resort in Miami serves as a pivotal stage. With the agenda refocused on AI regulation, energy supply chains, and innovation, Stansberry anticipates this as the moment the Silicon Dollar steps into the global spotlight—not as a proposal, but as an accomplished reality. Investors subscribing now to specialized briefings gain foresight into these catalysts, positioning portfolios ahead of the surge.

Decoding the AI Matrix: The New Oxygen of Global Commerce

What exactly constitutes this new foundation? Stansberry describes the AI matrix as the scarce, physical ecosystem without which no advanced AI can function: vast quantities of rare earth elements, copper, lithium, and specialized metals; precision-engineered semiconductors and GPUs; colossal energy and water inputs; and hyperscale data centers straining engineering limits. Every ChatGPT query, autonomous vehicle mile, or algorithmic trading execution traces back to this tangible base, valued in the tens of trillions.

Unlike software abstractions, these elements create natural choke points—narrow gateways through which capital must flow. NVIDIA’s GPUs, for instance, require specialized power delivery systems, cooling infrastructure, networking, and reliable energy. Control these, and you control the economics of the AI age. This mirrors oil’s centrality but elevates it to a more complex, multifaceted domain where U.S. leadership in innovation and alliances provides a competitive edge.

The scale is breathtaking. Data center investments alone eclipse prior megaprojects in speed and magnitude. As Vladimir Putin and others have noted, dominance here equates to global influence. Trump’s approach—securing domestic production, allied coordination via Pax Silica and FORGE, and excluding rivals from key inputs—aims to make participation in the AI economy dependent on dollar-linked systems.

Choke-Point Investments: The Stocks Set to Define the Era

Stansberry’s Silicon Dollar Playbook identifies companies occupying these irreplaceable positions. Here is an in-depth exploration to inform your decisions—though for complete theses, price targets, and risks, dedicated subscribers receive the full forensic analysis.

Broad Exposure Through REMX: The VanEck Rare Earth and Strategic Metals ETF provides immediate, diversified access to critical materials. Having delivered over 160% returns in the recent period amid rising demand, it serves as a foundational holding for those entering the theme. Its basket approach mitigates single-stock risks while capturing the upstream mineral surge essential to chips and infrastructure.

AI Power Delivery Leader: One standout is a specialized U.S. manufacturer (producing in Massachusetts) holding proprietary patents for power systems enabling high-density AI servers. NVIDIA’s advanced chips demand precise, high-current, low-voltage delivery that conventional designs cannot sustain. This firm’s solutions have been validated through ITC infringement cases, generating royalties, with a backlog surging 70% and revenues projected up 34%. Tariffs on Chinese alternatives further entrench its moat. Stansberry likens it to Qualcomm’s wireless dominance, which delivered thousands of percent gains for early investors. Near-term doubling or tripling potential makes it a compelling choke-point play.

Mining Royalty Innovator: Applying the proven Franco-Nevada model—where investors collect percentages of production without operational headaches—this younger firm holds royalty streams on silver, copper, and gold across continents. These metals are foundational to AI hardware. Revenues are scaling dramatically from $12 million in 2024 toward $100 million this year and potentially $300 million by 2028, all with minimal capex. Royalty structures offer leveraged exposure to commodity upside, low risk, and high margins—the “toll road” Stansberry has championed for decades. Early positioning here could mirror Franco-Nevada’s extraordinary compounding.

Dominant Natural Gas Producer: AI’s energy appetite is voracious, with data centers rivaling small nations in consumption. Natural gas remains the scalable, reliable bridge fuel. This low-cost producer accounts for roughly 6% of U.S. output, generating massive free cash flow (up to $1 billion in peak months). As scarcity drives prices, incremental gains flow disproportionately to the bottom line. Stansberry dubs such players “Gods of Gas,” highlighting their role in powering the matrix without reliance on intermittent renewables.

Permian Basin Royalty Holder: Owning 87,000 mineral acres in America’s premier energy basin—now also a data center hotspot due to cheap gas—this passive royalty collector benefits automatically from surging demand. No drilling expenses, just steady “mailbox money” as producers ramp output to fuel AI. The Permian supplies half of U.S. oil and critical gas, positioning this firm at the energy-AI intersection.

Produced Water Infrastructure Specialist: A hidden gem in the Permian, this company manages the largest network for handling oil production wastewater, a bottleneck threatening output. Regulatory shifts boosted its market share to 39%, supporting 50% EBITDA margins. Without efficient water management, cheap Permian energy falters—making this an ultimate enabler for AI power needs. Undervalued as a “boring” pipeline yet essential to the matrix.

Additional high-conviction names include NVIDIA (GPU dominance, +1,200% recent gains), Vertiv (cooling systems, +500%), GE Vernova (power infrastructure, +700%), Taseko Mines (copper), Arista Networks (networking, +750%), and others like Celestica, Eaton, Quanta Services, and Corning. These represent the physical backbone where capital converges.

Stansberry contrasts these with “tenant” companies that merely use AI without owning infrastructure; they will pay tolls rather than collect them. China-exposed supply chains face particular risks due to the strategic decoupling.

Crafting a Resilient Portfolio: Strategies, Risks, and Timing

Successful navigation requires more than stock picking. Diversify across the matrix layers—minerals (REMX), power/semiconductors, energy, and infrastructure—while maintaining long-term horizons spanning decades. Dollar-cost averaging mitigates volatility, and position sizing (e.g., 5-10% per idea) manages risk. Monitor policy developments, G20 outcomes, and capex announcements as catalysts.

Risks abound: execution delays, regulatory shifts, technological disruptions, geopolitical escalations, or AI hype cycles bursting. Inflation, recession, or accelerated de-dollarization could intervene. However, the structural tailwinds—inescapable AI demand and allied coordination—suggest asymmetric upside for the prepared.

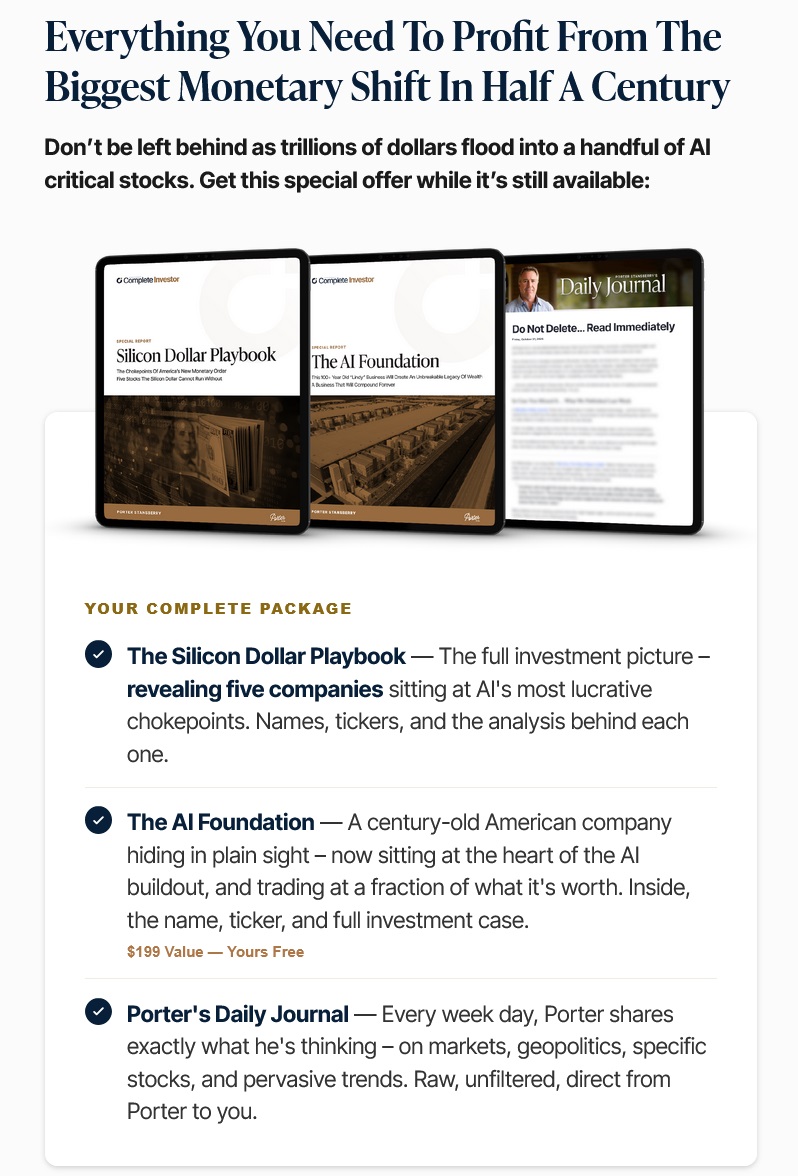

Stansberry’s track record, including Adobe (3,000%+), Regeneron (5,000%+), Cheniere, Shopify, and Texas Pacific Land, provides confidence. His latest offerings, including The Silicon Dollar Playbook and complimentary The AI Foundation report (detailing a century-old supplier with a massive CEO insider buy), are available at accessible pricing around $199 for comprehensive research plus ongoing insights via daily journals. Subscribing equips you with proprietary analysis unavailable elsewhere, timed perfectly before broader market recognition.

Embracing the Opportunity Before the Divide Widens

The Silicon Dollar era is not a distant forecast but a present reality, with agreements signed, capital mobilized, and companies already surging. Porter Stansberry’s analysis illuminates the path: own the choke points, understand the reset, and act decisively. Those who do will echo the petrodollar winners, building generational wealth. Those who hesitate risk repeating the mistakes of past transitions.

The choice is yours. Click through to explore Stansberry’s research today and secure your copy of the playbook. With trillions on the move and December’s spotlight approaching, informed subscribers are best positioned to prosper. The monetary order is evolving—ensure your portfolio evolves with it.

Frequently Asked Questions About Porter Stansberry’s Silicon Dollar Thesis

What exactly is Trump’s “Silicon Dollar” and how does it differ from the petrodollar?

The Silicon Dollar refers to a new monetary framework designed to replace the fading 50-year-old petrodollar system. Instead of anchoring global demand for the U.S. dollar to oil, it anchors it to the physical infrastructure of artificial intelligence — including critical minerals, semiconductors, energy systems, and data centers. Through agreements like Pax Silica and the FORGE Alliance, the U.S. and its allies aim to control the “AI matrix,” ensuring that nations wanting to participate in the AI economy must engage with American-controlled supply chains. This creates sustained demand for the dollar similar to how oil did in the 1970s, but for the dominant technology of the 21st century.

Is this Silicon Dollar shift already underway, and what role does the December G20 summit play?

Yes, the shift is well underway. Key agreements such as Pax Silica (signed December 12, 2025) and the FORGE Alliance have already been established behind the scenes. The upcoming G20 summit at Trump’s Doral Resort in Miami is expected to serve as the public unveiling moment, where the new priorities — AI regulation, secure energy, and technological innovation — will effectively launch the Silicon Dollar on the world stage. Investors who position themselves before this event could benefit from the anticipated surge in awareness and capital flows.

Which stocks or investments does Porter Stansberry recommend for the Silicon Dollar era?

Stansberry highlights companies sitting at critical “choke points” in the AI matrix. Key ideas include the VanEck Rare Earth and Strategic Metals ETF (REMX) for broad mineral exposure, specialized AI power delivery firms, mining royalty companies modeled after Franco-Nevada, dominant low-cost natural gas producers, Permian Basin royalty owners, and produced water infrastructure specialists. Additional names frequently mentioned are NVIDIA, Vertiv, GE Vernova, Arista Networks, and others involved in chips, cooling, networking, and energy infrastructure. These are detailed with full investment theses in The Silicon Dollar Playbook.

Why does Porter Stansberry believe this creates a major wealth divide?

Just like the petrodollar era created winners (those who owned stocks in oil, banks, defense, and tech) and losers (cash savers eroded by inflation), the Silicon Dollar is expected to concentrate massive capital flows into a narrow group of companies controlling essential AI resources. Those who understand and invest in the physical backbone of AI early could see extraordinary gains, while those who remain in cash or traditional assets risk losing purchasing power as the monetary order resets. Stansberry’s goal is to help regular investors get on the right side of this shift.

How can I access Porter Stansberry’s Silicon Dollar research and recommendations?

You can get immediate access to The Silicon Dollar Playbook — which includes detailed analysis on five high-conviction choke-point stocks, price targets, risks, and catalysts — along with the complimentary report The AI Foundation. This comprehensive package is currently available for a one-time introductory price of $199. It also includes Porter’s Daily Journal for ongoing insights. To secure your copy and position yourself before the December catalyst, visit the order page here.