In a volatile financial landscape marked by looming tariff announcements, deepening yield curve inversions, and skyrocketing living costs, The Oxford Club has introduced a compelling alternative to traditional stock market investing: the Oxford Bond Advantage. This service, featuring Chief Income Strategist Marc Lichtenfeld, promises retirees and risk-averse investors a way to “quit stocks” while still securing substantial, legally backed returns.

With a flagship offering dubbed the “Stock Quitters Portfolio,” the program centers on a unique type of fixed-income investment—superbonds—that aims to deliver stock-like gains without the rollercoaster ride of equities. This article delves into the details of the Oxford Bond Advantage, exploring its premise, mechanics, benefits, risks, and whether it lives up to its bold claims.

![]()

The Premise: A Response to Market Uncertainty

The Oxford Bond Advantage emerges against a backdrop of economic unease. As of March 28, 2025, the financial world braces for President Trump’s anticipated April 2 announcement on reciprocal tariffs, which could impose significant levies—20% on China, 25% on steel and aluminum, and 25% on Canadian and Mexican goods. Goldman Sachs warns that every 5% increase in U.S. tariffs could slash S&P 500 earnings by 1-2%, potentially triggering a 10-20% drop with tariffs reaching 50%. Coupled with a slowing Q1 GDP, a deepening yield curve inversion, and U.S. debt at 123% of GDP, the stage is set for what Lichtenfeld calls “the big one”—a market event that could devastate unprepared investors.

For retirees or those nearing retirement, this volatility is a nightmare. Traditional stock investments, while offering growth potential, carry the risk of sudden crashes—like the dot-com bust (Nasdaq down 70%), the Great Recession (S&P halved), or the 2022 bear market (worst since 2008). The *Oxford Bond Advantage* positions itself as a safe haven, targeting investors who “can’t afford another crash” and crave certainty over speculation.

What Is the Stock Quitters Portfolio?

At the heart of the Oxford Bond Advantage lies the “Stock Quitters Portfolio,” a curated selection of what Lichtenfeld terms “superbonds.”

Unlike traditional bonds—think U.S. Treasurys yielding 1-2% or corporate bonds at 3-4%—superbonds are speculative, high-yield fixed-income securities offering returns that rival or exceed the stock market. The flagship promise? A predetermined, contractually obligated return of over 200% in as little as four years, backed by legal agreements that eliminate the guesswork of equity investing.

These superbonds aren’t tied to stock price fluctuations. Lichtenfeld cites examples like Triumph Group, which delivered an 84% return over four years despite its stock dropping 43% in 2022, and Vital Energy, which yielded 88.41% in four years while its stock tanked 55%. The key differentiator is the legal contract: investors know their exact payout upfront, and as long as the issuing company avoids bankruptcy, that return is guaranteed upon maturity.

The portfolio isn’t about abandoning stocks entirely but diversifying away from their volatility. Lichtenfeld, a dividend stock advocate, encourages a balanced approach—keeping some equities for long-term growth while allocating a portion of one’s nest egg to superbonds for stability and predictable gains.

How Superbonds Work

Superbonds operate on a simple yet powerful principle: fixed returns determined at purchase. Here’s a breakdown based on Lichtenfeld’s explanation:

1. Investment Process: Investors access superbonds via a brokerage account using a nine-digit CUSIP code (akin to a stock ticker). For instance, a $10,000 investment in a Citigroup Global Markets superbond in early 2023 would have shown a 130% return over two years—turning $10,000 into $23,000—visible before committing a dime.

2. Predetermined Returns: Unlike stocks, where future value is a gamble, superbonds display their total return upfront. Examples include 117% in 2.5 years, 217% in 10 months, or even 1,091% in under three years—outpacing the S&P 500 by multiples.

3. Flexibility: While holding to maturity locks in the full return, investors can sell early. This carries some risk—returns aren’t guaranteed if sold prematurely—but Lichtenfeld notes he’s never taken a loss on early sales, and occasionally, selling early yields more than promised if demand spikes.

4. Yield Component: Superbonds also pay regular interest (yield), providing income alongside growth, much like dividend stocks but with greater principal protection.

Lichtenfeld’s system screens for companies with strong cash flow, liquidity, and leadership, targeting a Minimum Expected Annual Return (MEAR) that beats the stock market’s average. Examples include a 211.15% return by 2029 from a Fortune 500 media giant or 342% from Liberty Interactive by 2029.

Benefits of the Oxford Bond Advantage

The Oxford Bond Advantage offers several compelling advantages:

– Certainty in Chaos: With returns locked in by contract, investors sidestep stock market volatility. Tariffs, trade wars, or recessions won’t derail payouts unless the issuer defaults.

– High Returns, Lower Risk: Superbonds deliver stock-like gains (50% to over 200% in 4-5 years) with only one major risk—company bankruptcy—versus stocks’ dual risks of price drops and total loss.

– Legal Protection: Bondholders are paid before stockholders in bankruptcy, reducing loss severity compared to equities. Occidental Petroleum’s stock fell 65% from 2019-2021, losing shareholders over half their investment, while its bondholders earned $3,750 on $20,000.

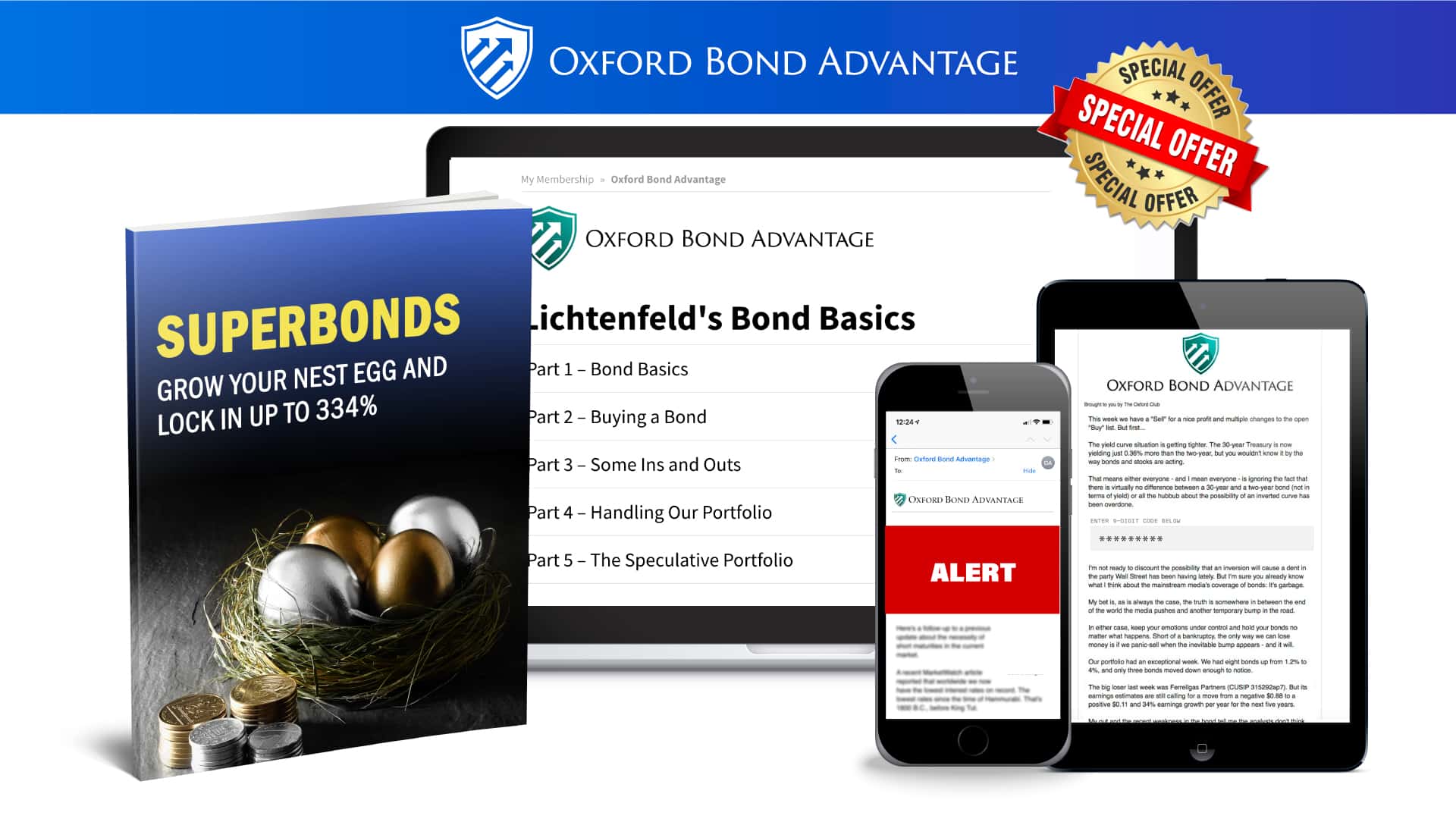

– Accessibility: The service demystifies bonds for novices via a five-part training series, “Lichtenfeld’s Bond Basics”, and weekly updates, making it approachable even for those new to fixed income.

– Discounted Entry: A $2.5 million discount pool slashes the $4,000 annual fee to $1,495 for the first 1,000 subscribers—a 62% reduction—sweetening the deal.

– Guarantee: Lichtenfeld promises a 50% return opportunity within a year, backed by a free second year or a $1,495 credit if unmet, ensuring confidence in the strategy.

Risks and Caveats

Despite its allure, the Oxford Bond Advantage isn’t risk-free:

– Bankruptcy Risk: If a company goes bankrupt, bondholders may not recover their full investment. Lichtenfeld mitigates this by targeting financially sound firms, but the risk remains.

– Speculative Nature: Superbonds are high-yield, high-risk bonds, more volatile than Treasurys or investment-grade corporates. While Lichtenfeld’s track record shows no losses, past performance isn’t a guarantee.

– Early Sale Uncertainty: Selling before maturity voids the predetermined return, potentially resulting in a loss, though Lichtenfeld’s experience suggests this is rare.

– Not a Stock Replacement: For long-term growth, stocks may still outperform. Superbonds suit those prioritizing safety over speculative upside.

– Limited Availability: The $1,495 discount is capped at 1,000 subscribers, and sales are final to prevent abuse, requiring swift commitment.

The Oxford Bond Advantage Experience

Subscribers to Oxford Bond Advantage receive:

– Stock Quitters Portfolio Report: Details three superbonds, including one with a 211.15% return by 2029 from a media titan reaching 200 million homes.

– Weekly Updates: Emails with market insights and 2-3 monthly bond recommendations.

– Training Series: “Lichtenfeld’s Bond Basics” covers buying, managing, and diversifying superbonds.

– Support: A dedicated team assists via phone, ensuring no one’s left confused.

Testimonials highlight success: Matt Hannon saw over 40% returns on six $10,000 investments in 18 months, while Dr. Joseph Rocca grew $10,000 to $37,000. Susan Breeze, a bond novice, credits the service with transforming her retirement strategy.

Why Now? The Timing Argument

Lichtenfeld argues that 2025 is a golden window for bonds. Falling interest rates amid a weakening economy boost bond prices (inversely related to rates), enhancing returns. The April 2 tariff “shocker,” as dubbed by Yardeni Research, could tank stocks, making superbonds’ stability timely. With U.S. credit card debt at $1.2 trillion and savings dwindling, the need for a reliable income stream is urgent.

Who Should Join?

The Oxford Bond Advantage targets:

– Retirees or near-retirees with limited recovery time.

– Risk-averse investors tired of stock market drama.

– Those seeking predictable, high returns without daily monitoring.

It’s less suited for young investors with decades to weather crashes or aggressive traders chasing exponential stock gains.

Marc Lichtenfeld’s Oxford Bond Advantage: Real Users Reviews

Here’s a summary of what people are saying about Marc Lichtenfeld’s *Oxford Bond Advantage* service based on reviews and comments from Stock Gumshoe, as of the latest available feedback. The sentiments reflect a mix of experiences, ranging from enthusiastic praise to sharp criticism, centered on the service’s bond recommendations, performance, and overall value.

Summary of Opinions

Reviews on Stock Gumshoe reveal a polarized reception of the Oxford Bond Advantage.

Positive comments highlight the service’s potential for solid returns, low risk, and educational value, especially for those who appreciate steady income from bonds. Subscribers who’ve had success often cite specific gains and praise the simplicity of the strategy when followed carefully.

However, negative feedback is significant, with many users reporting substantial losses due to bond defaults, criticizing the service for overhyped promises, poor customer service, and questionable reliability of Marc Lichtenfeld’s claims (notably his assertion of never losing money). Bankruptcy of recommended companies like Peabody Energy and Oasis Petroleum is a recurring grievance, leading some to label the service as misleading or a “scam.” The non-refundable $1,495–$4,000 subscription fee adds fuel to the dissatisfaction for those who feel burned.

Example of a Positive Review

Comment from a “Chairman’s Circle” member (November 7, 2023):

– Feedback: “About 7 years ago I paid $5k to be a ‘chairman’s circle’ member of the Oxford Club so all the VIP newsletters are now included in a $125 annual renewal. This latest, the Bond Advantage, is one of the best. This gives me the opportunity to make very good money with quite low risk. I’ve bought most of his recommendations so far, all at par or a discount with the expected return on these short-term bonds averaging about 8%. That is great in this environment.”

Example of a Negative Review

Comment from an anonymous user (undated but part of ongoing microblog discussion):

– Feedback: “My recommendation based on personal experience: DO NOT subscribe to the Oxford Bond Advantage. I have been purchasing Steve McDonald’s recommendations over the last few years in a highly diversified portfolio i.e. 2-4 bonds per company that HE RECOMMENDED. His recommendations of Alpha Natural, Arch Coal, Walter Energy, Peabody Energy, Key Energy, Noranda Aluminum have ALL FILED FOR BANKRUPTCY. Another of his recommendations, Petroquest has stopped paying interest and will, no doubt, be filing for bankruptcy… Literally any income I am receiving from ALL THE OTHER BONDS HE RECOMMENDED is more than offset by the huge losses of these bankrupt bonds. If you subscribe to the Oxford Bond Advantage, keep plenty of antacids around.”

Overall Takeaway

The Oxford Bond Advantage garners praise from those who’ve navigated it successfully for decent yields (e.g., 8% returns) and value its bond-focused approach, but it’s heavily criticized by others who’ve suffered from defaults and feel misled by bold performance claims.

The service’s success seems to hinge on execution and luck with avoiding defaults, with subscribers split on whether it’s a worthwhile investment or a risky disappointment. As of March 28, 2025, these sentiments provide a snapshot of past experiences, though newer feedback might shift with Lichtenfeld’s current picks.

Conclusion

The Oxford Bond Advantage and its “Stock Quitters Portfolio” offer a tantalizing proposition: ditch stock market uncertainty for legally backed, triple-digit returns. Marc Lichtenfeld’s superbonds blend high yields with principal protection, backed by a proven track record and a robust support system. At $1,495 (with a $2,505 discount), plus a 50% return guarantee, it’s a low-barrier entry into a niche Wall Street overlooks.

Yet, it’s not a panacea. Bankruptcy risk and the speculative nature of superbonds demand caution, and it’s not a full stock replacement. For those who can’t stomach another crash—or who value sleep over stress—it’s a compelling lifeline. As George Rayburn quips, “Who doesn’t want to sleep better and not worry about their money?” If that’s you, the *Oxford Bond Advantage* might just be worth a call to 888.570.9830—or a click here —before the 1,000 spots vanish.

FAQ: Oxford Bond Advantage and Stock Quitters Portfolio

What is the Oxford Bond Advantage?

The Oxford Bond Advantage is a research service led by Marc Lichtenfeld, Chief Income Strategist at The Oxford Club. It focuses on “superbonds”—high-yield, speculative bonds that offer predetermined, legally backed returns exceeding stock market averages. It’s designed for retirees and risk-averse investors seeking stability amid market volatility, promising gains like over 200% in four years without the ups and downs of stocks.

What are superbonds, and how are they different from regular bonds?

Superbonds are a special type of high-yield corporate bond that Marc Lichtenfeld targets for their exceptional returns (e.g., 50% to over 200% in a few years). Unlike traditional bonds like U.S. Treasurys (1-2% yield) or standard corporate bonds (3-4%), superbonds are more speculative but offer stock-like gains with a legal contract guaranteeing the payout at maturity, as long as the issuing company doesn’t go bankrupt.

What is the Stock Quitters Portfolio?

The “Stock Quitters Portfolio” is a report included with an Oxford Bond Advantage subscription. It details three superbond recommendations, including one from a Fortune 500 media company promising over 211.15% by 2029. It’s aimed at helping investors “quit stocks” by locking in high, predictable returns, offering a model portfolio for retirement growth.

How do superbonds work?

You buy superbonds through a brokerage using a nine-digit CUSIP code, which shows the exact return upfront (e.g., 130% over two years). Hold to maturity for the guaranteed payout, or sell early with potential (but not assured) gains. They also pay regular interest, combining income and growth, and are unaffected by stock price drops unless the company goes bankrupt.

Why is now a good time to invest in superbonds?

Marc Lichtenfeld highlights 2025 as ideal due to looming market risks—like the April 2, 2025, tariff announcement—and falling interest rates, which boost bond prices. With economic uncertainty (e.g., 123% debt-to-GDP, $1.2 trillion credit card debt), superbonds offer stability and high returns when stocks are volatile.

What kind of returns can I expect?

Returns vary but can be substantial: 117% in 2.5 years, 217% in 10 months, or even 1,091% in under three years historically. The flagship promise is over 200% in four years, with examples like 211.15% by 2029 or 342% from Liberty Interactive. Typical targets are double-digit returns within five years, often outpacing the S&P 500.

What are the risks involved?

The main risk is company bankruptcy, which could reduce or eliminate payouts, though bondholders are paid before stockholders in liquidation. Selling early voids the guaranteed return, potentially leading to a loss (though Lichtenfeld has never seen this). Superbonds are speculative, carrying more risk than traditional bonds but less than stocks.

Can I lose money with superbonds?

Yes, if the issuing company goes bankrupt, you might not recover your full investment. However, Lichtenfeld has never lost money on a superbond recommendation or personal investment. Holding to maturity ensures the promised return, and even in bankruptcy, bondholders have legal priority over stockholders, reducing total loss risk.

How much does it cost to join Oxford Bond Advantage?

Normally $4,000 per year, but a $2.5 million discount pool slashes it to $1,495 for the first 1,000 subscribers—a 62% reduction. This includes the “Stock Quitters Portfolio” report, weekly updates, and a five-part training series, Lichtenfeld’s Bond Basics. All sales are final to prevent abuse.

What’s the guarantee offered?

Lichtenfeld guarantees a chance at a 50% return on one recommendation within a year. If unmet, you get a free second year or a $1,495 credit toward another Oxford Club service. If you quit for any reason, you keep the report and training series, with the credit as a parting gift.

Do I have to quit stocks entirely?

No. Lichtenfeld encourages diversification, suggesting superbonds for stability while keeping stocks for long-term growth if you have the time horizon. It’s ideal for those who can’t risk a crash, but you can still hold dividend stocks or other equities alongside superbonds.

How do I get started?

Click here or call 888.570.9830 (or 410.864.3090). Fill out the form, and you’ll gain immediate access to the report, training, and weekly emails. Act fast—only 1,000 discounted spots are available, and they’re expected to fill quickly.

Why haven’t I heard of superbonds before?

Brokers rarely promote superbonds because they earn minimal commissions compared to stocks. Wall Street prioritizes high-fee products, leaving these high-yield opportunities to elite investors like David Tepper or Carl Icahn. Oxford Bond Advantage makes them accessible to regular investors.

How long do I need to hold superbonds?

Average holding time is around four years, though some mature faster (e.g., 10 months for 217%) or slower (up to five years). You can sell early, but holding to maturity locks in the full return. Lichtenfeld staggers maturities for continual payouts.

Is this suitable for beginners?

Yes. Most subscribers, like Susan Breeze, had no bond experience. The service includes step-by-step guidance via Lichtenfeld’s Bond Basics and a support team, making it beginner-friendly despite the complexity of superbonds.

What happens if I sell a superbond early?

Selling before maturity means the return isn’t guaranteed—you might profit less, break even, or rarely lose money. Lichtenfeld has never taken a loss on early sales and sometimes scores bigger gains if demand rises, but it’s riskier than holding to maturity.

Can superbonds protect me from a market crash?

Yes, as long as the issuing company stays solvent. Stock drops (e.g., Boeing’s 60% decline) don’t affect superbond payouts, which remain fixed. They’re a buffer against volatility, though not immune to issuer-specific risks.

How does Oxford Bond Advantage support its members?

Members receive weekly email updates, 2-3 monthly bond picks, the “Stock Quitters Portfolio” report, and the Lichtenfeld’s Bond Basics series. A phone support team assists with questions, ensuring a stress-free experience.

Are the returns really legally backed?

Yes. Superbonds are legal contracts between you and the issuer, specifying the exact payout at maturity. As long as the company doesn’t default, you’re guaranteed that return—unlike stocks, where no such promise exists.

Who is Marc Lichtenfeld, and why trust him?

Marc Lichtenfeld is The Oxford Club’s Chief Income Strategist with over a decade of experience. A former Wall Street trader, he’s never lost money on a superbond personally or professionally. His dividend stock expertise is featured in bestselling books, and testimonials praise his reliable, transparent guidance.