Navigating the financial landscape can be a daunting task, especially when markets become unpredictable. Retirees often find themselves at a crossroads during market fluctuations, wondering how significant drops might impact their nest eggs. A 10% market drop, while seemingly minor to some, can stir anxiety for those reliant on fixed incomes. By understanding how such declines affect retirement plans, retirees can better safeguard their financial security. Our guide dives into strategic insights and expert advice to help you embrace market volatility with confidence, ensuring your golden years remain as bright as your dreams.

Brief Overview

Navigating a 10% market drop can be intimidating, especially for retirees who depend on fixed incomes. However, understanding the historical context and potential effects of such declines can illuminate strategies to mitigate risks and safeguard retirement savings. Retirees are encouraged to explore conservative withdrawal tactics, consult financial advisors, and maintain diversified portfolios to foster stability. Adjusting financial plans to market conditions and leveraging expert advice ensures retirees can weather economic turbulence without compromising their long-term goals. Emphasizing proactive risk management and strategic planning fortifies retirement investments against market volatility.

Key Highlights

- A 10% market drop impacts retirees’ financial security; proactive strategy adjustments are crucial.

- Historical market drops reveal patterns, emphasizing the importance of diversified investments.

- Adopt flexible withdrawal strategies to preserve capital and ensure income sustainability.

- Rebalancing portfolios during bear markets enhances stability and mitigates risks.

- Regular budget reviews and professional advice ensure financial resilience amidst market changes.

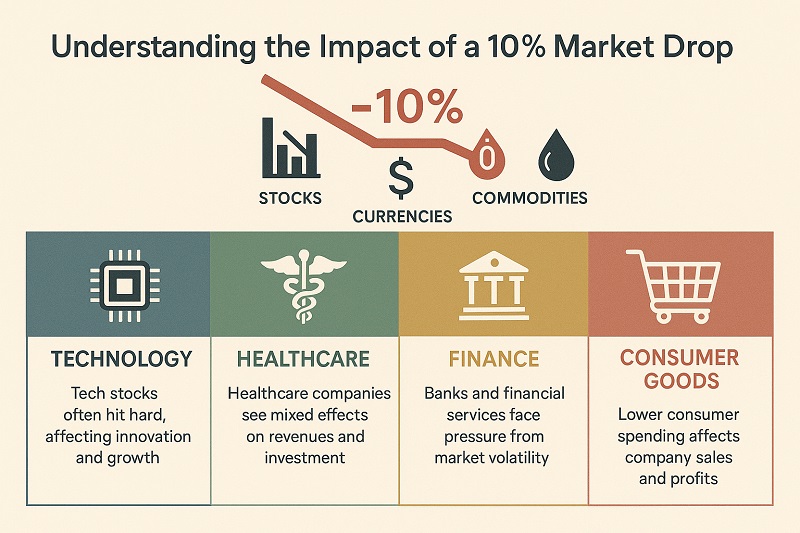

Understanding the Impact of a 10% Market Drop

A 10% market drop can stir anxiety among investors, yet understanding its impact sheds light on potential opportunities or risks. Historically, the economy has weathered numerous downturns, revealing patterns of recovery. For retirees, maintaining a steady portfolio is crucial, as fluctuations in stocks directly affect retirement income and savings. Delving into the historical context reveals how past market conditions have shaped today’s financial strategies. Additionally, comprehending what this drop means for retirees will help align personal finance goals with market realities, ensuring they navigate their retirement years with enhanced financial security.

Historical Context and Effects on the Market

Understanding a 10% market drop’s historical significance provides insight into how the stock market typically reacts to such events. Historically, the stock market has experienced similar downturns, with some leading to a bear market and others recovering quickly. Examining past market drops gives retirees a clearer picture of potential outcomes, helping them align their investment strategies accordingly. In the 1980s and early 2000s, the market dropped significantly but eventually rebounded, solidifying investor confidence over time. These historical trends highlight the dynamic nature of the market, emphasizing that downturns are often temporary and lead back to economic growth.

When considering the impact on the overall economy, a 10% market drop might initially trigger fears of financial instability. However, it’s vital to view these changes as a natural part of the market’s cycle. Such drops often reflect market volatility, which, while concerning, doesn’t always translate to long-term economic decline. Investors need to recognize that the market operates in cycles, each influenced by unique financial and geopolitical factors. By understanding these cycles, retirees can better prepare for potential fluctuations in their retirement income and investment portfolios.

Market volatility following a drop affects various sectors differently, offering savvy investors opportunities to recalibrate their strategies. During these times, retirees should pay attention to how stocks in their portfolios perform and make adjustments to protect their retirement savings. It’s also essential to consider how the economy adapts to these changes, often with fiscal policies aimed at stabilization. Retirees can leverage this knowledge to make informed decisions, ensuring their financial strategies are robust enough to withstand market uncertainties. By learning from historical patterns and effects, retirees can avoid knee-jerk reactions, opting instead for a balanced approach that keeps their long-term retirement goals intact.

What a Market Drop Means for Retirees

A 10% market drop can directly impact retirees’ financial landscapes, affecting everything from retirement savings to retirement income. For those relying heavily on investments for their retirement, such a drop might mean re-evaluating their financial strategies to ensure stability. It’s critical for retirees to understand how market volatility can influence their long-term financial security. Typically, when the market dropped, retirees often found that their portfolio faced immediate stress, particularly if heavily vested in stocks. This highlights the importance of diversifying investments to mitigate risks associated with sudden market changes.

Retirees might need to adjust their withdrawal strategies during turbulent times to maintain their income streams. This involves exploring more conservative withdrawal tactics that ensure longevity of their savings. By adapting their personal finance strategies to market conditions, retirees can better manage their retirement budgets, avoiding significant changes to their lifestyle. When market drops occur, maintaining a balanced portfolio becomes paramount, involving a strategic mix of stocks and other financial assets. This balance provides a safety net during times of market volatility, securing retirees’ financial futures.

In light of potential market uncertainties, retirees should also consider the benefits of consulting with financial advisors. Experts can offer tailored advice on adjusting portfolios and managing retirement spending, helping retirees navigate fluctuations with confidence. Additionally, retirees should remain informed about economic trends and financial news to make timely adjustments to their investments. This proactive approach helps mitigate the impacts of a market drop, ensuring continued income stability. With comprehensive planning and adaptability, retirees can protect their savings and maintain their desired lifestyle, even when faced with unpredictable economic shifts.

As market volatility becomes a constant companion in investment environments, it’s crucial for retirees and investors to have adaptable strategies. Navigating these turbulent times can protect your financial portfolio from potential downturns, ensuring a balanced approach to investments. These strategies focus on adapting your withdrawal approach and exploring conservative withdrawal tactics, both instrumental in safeguarding your retirement income during unpredictable market conditions. By implementing these approaches, you can maintain steady financial growth and secure your retirement goals, even in the face of market uncertainties.

Adapting Your Withdrawal Approach

When market volatility hits, particularly with events like a 10% market drop, it’s pivotal to rethink your traditional withdrawal approach. For retirees, this means assessing how withdrawals from your portfolio impact long-term sustainability. A smart investor knows that maintaining equilibrium during financial fluctuations can preserve investments. One effective tactic is adopting a flexible withdrawal rate, adjusting your financial strategy according to the economic climate. If your portfolio grows beyond expectations, consider withdrawing more. Conversely, reduce withdrawals during downturns to preserve capital, enhancing your portfolio’s resilience against market turbulence.

Understanding the intricate balance between withdrawals and market performance is especially vital in safeguarding retirement income. Facing a market drop, retirees should analyze their withdrawal strategy in the context of liquidity needs and investment horizons. For example, utilizing a bucket approach can differentiate the funds needed for current spending from those allocated for future growth. Short-term cash funds provide immediate income, protecting against having to sell stocks at a loss. Meanwhile, a separate portion of your investments can be locked into long-term growth opportunities, offering a hedge against market instability.

Successful investors also advocate for continuous portfolio reviews to ensure strategies align with personal and market dynamics. Retirees need to continually reassess their spending habits, as overspending in a volatile market can quickly deplete financial resources. Consider aligning your withdrawal approach with financial monitoring tools that respond to market volatility, delivering actionable insights promptly. Such measures support informed decision-making, preserving both wealth and investment longevity.

Additionally, this flexible approach provides peace of mind. Knowing you can adapt your strategy to current market conditions ensures you’re not cornered into a fixed withdrawal pattern. By being proactive, you minimize risks while optimizing your financial outcomes, securing both near-term and future income streams.

Exploring Conservative Withdrawal Tactics

In pursuit of securing reliable income amidst a volatile market, exploring conservative withdrawal tactics becomes essential. As markets fluctuate, maintaining retirement account stability demands a strategic, cautious approach. For retirees, understanding how to optimize withdrawals without compromising future growth is integral. Employing conservative strategies, such as the “4% rule,” can help in determining withdrawal rates that balance income needs with sustainability. This rule suggests that you withdraw 4% of your portfolio in the first year of retirement and adjust for inflation thereafter, ensuring a steady income flow.

Investors often maintain a portfolio balance that incorporates conservative stocks and diversified financial assets. Emphasizing low-risk investments can act as a buffer against market downturns. This approach should also involve reviewing tax implications on withdrawals, ensuring decisions don’t inadvertently increase liabilities. The aim is to preserve capital while generating income, even during unpredictable market conditions.

Building a diversified portfolio, comprising bonds, dividend-paying stocks, and other stable financial products, typically aids in minimizing risks associated with market volatility. It’s about more than just having a mix of assets; it’s about selecting the right combination that supports your income needs and financial goals. By choosing financial instruments that not only offer potential growth but also income, balance between security and upward potential is achieved.

Conservative withdrawal tactics must also account for potential longevity, ensuring assets last throughout retirement. This means taking a long-term view, recognizing the financial market’s cyclical nature. By anticipating these cycles, investors can position their accounts to withstand periods of downturn. Regularly evaluating withdrawal plans ensures they stay aligned with life expectancy and changing market conditions, which is crucial to maintaining a stable income.

Ultimately, exploring these tactics provides a competitive edge. Retirees who harness conservative withdrawal strategies align their investments with prudent financial planning, leveraging market insights to protect their portfolios. This careful approach helps in maintaining financial independence and confidence, no matter what challenges market conditions may present. By adapting to market changes with clear, calculated withdrawal strategies, you can secure not only your current lifestyle but also a dependable future.

Protecting Your Retirement Portfolio in a Bear Market

Facing a bear market is daunting, especially when protecting your retirement portfolio. Understanding how to safeguard investments during these downturns is critical for preserving your retirement income and goals. Two key strategies arise: rebalancing stocks for enhanced stability, and maintaining long-term retirement objectives amid financial volatility. Both strategies provide a framework for continuing your financial journey without succumbing to market uncertainties. By taking thoughtful steps now, retirees can bolster their portfolios against market upheavals, ensuring both short-term stability and long-term growth.

Rebalancing Stocks for Stability

Rebalancing your portfolio during a bear market is a proactive step to enhance financial stability. This involves adjusting the weightings of various asset classes to maintain your desired risk level. Doing so can help buffer your retirement portfolio against severe market volatility. Consider this: if stocks have significantly underperformed while bonds or other financial instruments have held steady, your asset allocation might be skewed. Regular rebalancing corrects these imbalances, ensuring that your investment portfolio aligns with your financial goals and risk tolerance.

Rebalancing isn’t just about maintaining balance; it’s also a vital risk management tool. By periodically adjusting your investment holdings, you mitigate the impact of market drops on your retirement income. Rebalancing encourages a disciplined approach, prompting you to periodically review and adjust your portfolio based on market conditions. This method helps prevent emotional decision-making, such as panic-selling during downturns, which can lock in losses and compromise your long-term financial strategy.

Investors may also consider diversifying across different sectors or geographic regions to balance their portfolios better. Diversification helps distribute risk, shielding your investments from sector-specific downturns. Incorporation of international or emerging market funds, for instance, could provide alternative growth opportunities when domestic markets are bearish. This balanced approach stabilizes your portfolio, guarding against isolated market dips that might otherwise threaten your retirement stability.

Furthermore, consulting with a financial advisor can provide valuable insights into effective rebalancing strategies tailored to your financial situation. Advisors might recommend dynamic asset allocation strategies that adapt to market changes, or the inclusion of safer financial products, like bonds, that cushion against stock volatility. Partnering with a financial expert ensures your portfolio remains aligned with your evolving retirement goals, integrating their expertise with your personal insights.

In summary, rebalancing offers a methodical path to preserving your retirement portfolio’s value during uncertain times. It instills discipline, encourages smart diversification, and adapts your investment strategy to market realities. Rebalancing isn’t just a precaution, it’s a proactive measure that keeps your retirement ambitions intact while fostering financial stability amid market turbulence.

Continue building your financial strategy with these rebalancing tips to ensure long-term investment growth and stability during turbulent market conditions:

- Evaluate your portfolio quarterly to monitor and adjust asset allocations.

- Use automated rebalancing tools to maintain discipline and consistency.

- Focus on low-cost index funds to reduce fees and increase diversification.

- Incorporate alternative assets, like real estate, for broader market exposure.

- Adjust bond holdings based on interest rate trends for better stability.

- Periodically review risk tolerance as life circumstances change.

These strategies, when combined, create a strong foundation for maintaining your investment goals in any market climate.

Maintaining Long-Term Retirement Goals

Ensuring your retirement goals remain on course during a bear market demands steadfastness and strategic oversight. It’s essential to remember that retirement is a long-term journey, and short-term market fluctuations shouldn’t deter you from your planned financial path. In fact, maintaining a focus on long-term objectives often leads to better outcomes, even during challenging economic climates.

Investors must resist the urge to make hasty decisions based on temporary market dips. A bear market is usually defined by a 20% drop, but your focus should be on how your overall retirement strategy aligns with these fluctuations. It’s crucial to balance immediate financial impacts with your ultimate aim of a secure retirement. Part of this involves examining your retirement spending; understand what’s essential and consider deferring large expenses until market conditions improve, thus preserving your resources.

Also, maintaining a diversified portfolio designed to endure such market conditions will align your investments with these long-term goals. Mix of bonds, stocks, and other financial products can provide a buffer, helping you ride out volatile times without derailing your retirement plans. By strategically selecting investments that offer stability and potential growth, you’re less likely to be swayed by temporary market setbacks.

A long view also means regularly reviewing and adjusting your financial strategy to reflect both market conditions and personal circumstances. During a bear market, reinforcing your financial knowledge becomes indispensable. Stay informed about ongoing economic trends and adjust your strategies as needed. Keeping abreast of potential opportunities or risks ensures you’re well-equipped to make timely adjustments.

Moreover, a strategic withdrawal plan is vital to fulfilling long-term retirement goals, promoting a steady income flow while preserving your portfolio’s longevity. Aligning your withdrawal strategies, such as the percentage of withdrawal or timing, with market realities helps in conserving assets during downturns. By adopting this adaptive approach, you’re also setting a foundation for lifelong financial independence.

Ultimately, a bear market challenges your resolve but provides an opportunity to reaffirm your financial strategies. Ensuring your retirement goals stay intact amidst market volatility requires diligence, informed decision-making, and strategic planning. With a clear focus on the long term, your portfolio becomes a bastion of stability, safeguarding your retirement dreams against unpredictable economic shifts.

Managing Retirement Spending During Market Fluctuations

When market fluctuations hit, retirees must adapt their strategies to safeguard retirement spending. Adjusting budgets and plans becomes vital during economic downturns, as it ensures financial security despite the volatility. We’ll delve into the importance of re-evaluating expenditure, alongside practical steps to take when adjusting retirement income sources. These approaches empower retirees to maintain stability and maximize their financial potential, regardless of market changes.

Adjusting Budgets and Plans

Adapting to market fluctuations is crucial for maintaining a stable financial life during retirement. Retirees often find that their spending habits need tweaking to safeguard their overall retirement income, particularly during volatile market periods. When the economy undergoes significant changes, revisiting your budget isn’t just prudent, it’s necessary for effectively managing retirement spending. Understanding the intricacies of market impacts becomes key as this helps retirees plan their monthly funds more effectively, avoiding overspending that could deplete their savings prematurely.

An essential step is to establish a flexible budgeting approach that accounts for variations in both the economy and personal life circumstances. This dynamic budgeting method allows retirees to adjust their expenditures promptly. Begin by evaluating all money inflows, pensions, social security, and any other retirement income, and match them against essential living expenses. Including a buffer for inflationary effects and unexpected costs ensures that your financial plan doesn’t waver during uncertain times.

The next move involves re-assessing your financial plans with a sharp focus on spending habits. Look at discretionary spending and identify areas where cuts can be made without significantly impacting your lifestyle. Shifting priorities, like moving funds from non-essential expenses to crucial needs or savings, can provide a stronger financial cushion. Implementing these changes not only aids in coping with market fluctuations but also aids in aligning retirement plans with prevailing economic conditions.

Retirees should also engage in regular financial reviews, recalibrating their plans to reflect the current state of the market. This exercise should consider the impact of taxes on your income and withdrawals, knowing how they affect net earnings. Analyzing tax obligations ensures that withdrawals from retirement accounts meet immediate needs without incurring unnecessary liabilities. Moreover, understanding the tax brackets can lead to strategies that optimize tax-efficient planning when dealing with retirement accounts.

Lastly, maintain an open line of communication with a financial advisor. Their expertise can provide a broader understanding of how your personal financial dynamics interact with market realities. Advisors can offer tailored strategies to address market fluctuations, ensuring your retirement income remains stable and your financial goals stay on course. Leveraging professional advice, paired with personal planning, helps mitigate the impact of economic unpredictability, allowing retirees to enjoy their golden years with less financial stress. Remember, flexibility is the pillar upon which stable retirement spending stands, particularly in times of market uncertainty.

While a 10% market drop can be concerning for retirees, it’s important to remember that volatility is a part of investing. By diversifying investments, maintaining a long-term perspective, and consulting with financial advisors, retirees can weather these fluctuations. Establishing a solid financial plan ensures that unforeseen market changes do not derail retirement goals. Proactively addressing potential risks, coupled with strategic financial resilience plans, can provide comfort and stability. Download our comprehensive guide to bolstering your investment strategy and securing your retirement nest egg against market shifts.

FAQ: What a 10% Market Drop Would Mean for Retirees

How does a 10% market drop affect retirees?

A 10% market drop impacts retirees by affecting their retirement savings and income. This requires proactive adjustments to financial strategies to maintain stability and security in their golden years.

Why is diversifying investments important during market volatility?

Diversifying investments helps mitigate risks associated with sudden market changes. A balanced portfolio can stabilize financial assets and protect against the impact of market downturns.

What strategies should retirees adopt to handle market fluctuations?

Retirees should adopt strategies like flexible withdrawal rates, regular portfolio rebalancing, and consulting financial advisors to manage market fluctuations effectively.

How can retirees preserve income sustainability during a market drop?

Retirees can preserve income sustainability by reviewing and adjusting withdrawal strategies. This might involve adopting conservative approaches like the “4% rule.”

Why consult financial advisors during market volatility?

Consulting financial advisors can offer retirees tailored advice, helping to effectively adjust portfolios and manage spending to withstand economic turbulence.