As the year 2026 approaches, planning for a financially stable future becomes more crucial than ever, especially if you’re nearing the golden age of 50. Whether you’re an experienced investor or just beginning your financial journey, understanding the significance of effective saving strategies can empower you to meet your retirement goals. This guide delves into practical tips and strategies to ensure you save intelligently, optimize growth, and secure your financial freedom. Start making informed decisions today for a worry-free tomorrow and take control of your financial destiny with confidence.

Brief Overview

As you approach the milestone of age 50, preparing for a financially stable future by 2026 becomes essential. Whether you’re an experienced investor or just beginning, this guide offers practical saving strategies to help you achieve your retirement aspirations and secure financial independence. Key insights include setting a clear retirement plan, understanding your lifestyle needs, managing expenses efficiently, and creating a robust investment portfolio. By focusing on maximizing contributions and diversifying investments, you’ll ensure your financial stability and enjoy a fulfilling retirement. With thoughtful planning and guidance, you can confidently embrace your future.

Key Highlights

- Plan for 2026 with clear retirement goals and concrete strategies for financial stability.

- Assess retirement lifestyle needs to understand and prepare for future financial requirements.

- Identify saving opportunities within fixed and variable expenses to boost savings.

- Maximize contributions to retirement accounts and leverage tax advantages.

- Diversify investments for robust growth and seek personalized advice from financial planners.

Defining Your Financial Goals for the Future

Envisioning your financial future is crucial as you approach 50. Planning for 2026 and beyond involves concrete strategies in retirement planning, personal finance, and setting clear retirement goals. An effective retirement plan will guide you through the complexities of financial planning, ensuring your savings align with future aspirations. Establishing a clear idea of your retirement lifestyle and understanding the costs involved can ease the stress of financial uncertainties. From assessing your retirement lifestyle needs to setting a precise plan, these elements will serve as a foundation for your financial stability in the upcoming years.

Setting a Clear Retirement Plan

At 50, having a structured retirement plan becomes more than just desirable; it’s essential. Retirement planning isn’t just about stashing your money away in dusty old savings accounts. It’s about strategically investing in your future, ensuring that your financial decisions today will secure the comfort and lifestyle you desire in the years to come. Start by assessing your current financial landscape. Look at your savings, your personal finance habits, and your investments, and ask yourself if they align with your retirement goals.

A comprehensive retirement plan should factor in all aspects of your financial situation. Consider how much you’ve saved so far and if it aligns with your anticipated retirement expenses. Remember, costs won’t just magically decrease when you retire; they might increase due to healthcare or lifestyle changes. Forecast these expenses now to avoid surprises later. Envision what your ideal retirement looks like and the financial requirements to get you there. Are you planning on traveling the world? Or maybe you want to invest in estate planning to secure your legacy. Each choice will significantly impact your financial needs in retirement.

Don’t forget to incorporate a savings strategy that utilizes the power of compound interest. By maximizing contributions to your retirement accounts, such as 401(k)s or IRAs, you harness the potential growth of your savings over the years. Talk to a financial advisor for personalized advice and explore all your options, including ways to mitigate taxes on your future withdrawals. The sooner you start, the more control you’ll have over your retirement journey. A clear retirement plan is not merely a wish list but a roadmap to a stable and fulfilling future. Use your financial assets to craft a plan that secures not just survival but a thriving lifestyle once you cross that retirement threshold.

ake your savings work smarter, not harder, and embrace the financial freedom you’ve worked so diligently to create.

Assessing Your Retirement Lifestyle Needs

Contemplating your future lifestyle is a critical piece of retirement planning. Crafting a retirement lifestyle plan starts with determining personal finance priorities and what matters most to you. Consider your daily routine, leisure activities, and any potential new passions that could surface once you retire. How you imagine spending your time directly influences the type of financial support you’ll need. It’s all about balancing your financial means with your desired lifestyle.

Firstly, dig into the expected costs of your post-retirement lifestyle. Do you see yourself maintaining your current lifestyle, or are there changes you’re planning to make? Maybe you’re dreaming of extensive travel, starting a new hobby, or even relocating to a more peaceful area. Each life choice brings different expenses, so it’s essential to accurately forecast these costs as part of your retirement plan. Outline the fixed and variable expenses that will define your day-to-day reality when you retire. By preparing detailed estimates, you can establish financial goals that support these dreams.

Consider also the potential for unforeseen medical expenses. Quality healthcare becomes increasingly vital and often costlier, so planning for these future expenses is wise. You’ll want to ensure that your savings and investment strategies are robust enough to handle such variables without straining your budget. Proactively setting funds aside can provide peace of mind, knowing you’re covered no matter what health challenges might arise.

Lastly, revisit your estate planning needs as part of this lifestyle assessment. How do you wish to secure your legacy? Ensuring that your estate planning is up-to-date and reflects your current desires protects your family and guarantees that your hard-earned assets are distributed according to your wishes. Engaging with a financial planner can provide additional insights tailored to your lifestyle aspirations.

hey’ll assist you in refining your financial strategy, helping you to frame a retirement lifestyle that’s not only sustainable but also richly rewarding. Investing this time and careful thought into assessing your retirement lifestyle needs will solidify the financial foundation necessary for your peace of mind and future enjoyment.

Evaluating Current Expenses and Income

Navigating your financial path at 50 requires a clear understanding of your current financial position. By examining your expenses and income, you lay the groundwork for robust money management. This insight is crucial for personal financial planning and will help align your spending with your retirement goals. Emphasizing the role of fixed and variable expenses ensures a focus on what can be controlled, optimized, or reduced. Once you identify where money flows, you’ll uncover opportunities to save, ensuring financial stability. Whether you’re prepping for retirement or optimizing savings, understanding these financial components is key to reaching your future objectives.

Understanding Fixed and Variable Expenses

Your journey toward financial stability at 50 significantly hinges on grasping the distinction between fixed and variable expenses. Fixed expenses are those predictable costs that remain constant each month, such as mortgage payments or rent, utility bills, and insurance premiums. From an investor’s perspective, understanding these steadfast outlays is crucial since they form the bedrock of any personal budget. Evaluating your fixed costs allows you to align them with your income, ensuring a steady cash flow essential for personal financial planning.

On the other hand, variable expenses, which fluctuate from month to month, like dining out, entertainment, or travel, offer room for financial flexibility and saving. These are the areas where savvy planning can have the most impact. By analyzing past spending patterns, you can anticipate your money needs, ensuring these costs don’t spiral unchecked. As an investor, strategically managing these variable costs can increase your savings potential, a vital component as you prepare for retirement. The goal is to transform these expenses into savings without compromising the quality of life.

To balance fixed and variable expenses, consider incorporating a monthly review process into your financial regimen. This ensures that your expenses align with your retirement savings goals and helps you stay on track with your personal money management plan. By keeping an eye on these financial metrics, you allow room for adjustments, ensuring your finances are always working towards your benefit rather than against it. Taking control of your financial situation now can lead to significant rewards in the future, securing the lifestyle you desire in retirement. As you assess these costs, remember that saving isn’t just about trimming expenses but directing money where it most benefits your financial growth.

Identifying Opportunities to Save

Once you’re clear on your expenses, the natural next step is to pinpoint where you can save money effectively, compounding your financial gains as you head toward retirement. Opportunities to save are often hidden in day-to-day financial activities. Begin with evaluating each category of your expenses for potential savings. Fixed expenses might seem unmovable initially, but refinancing your mortgage or negotiating better insurance rates can significantly reduce costs. Savvy investors often find these adjustments are potent tools in their financial arsenal for planning a brighter future.

Variable expenses, however, often house the most immediate opportunities for savings. By setting a reasonable budget for discretionary spending, dining out, entertainment, and non-essential purchases, you carve out a space for more deliberate spending, which frees up money for more important goals, say, boosting your retirement accounts. Implementing a tracking system could provide the additional insight needed to spot overspending trends, offering a chance to redirect those funds into savings or investments.

Engaging regularly with your financial plan helps identify these opportunities before they pass. Regular financial reviews not only keep you on track but also ensure your money aligns with your long-term goals. As you leverage these opportunities, consider maximizing contributions to tax-advantaged savings accounts or diverting funds into more lucrative investments that position you better financially by the time retirement rolls around.

Consulting with a financial planner can provide personalized insight tailored to your unique financial situation, optimizing your saving strategy. By harnessing every savings opportunity, you enhance your financial resilience, ensuring that at 50, you’re not just secure but primed for a financially free retirement. In this effort, never underestimate the power of small, consistent savings; they truly can compound into substantial financial freedom over time, allowing your income to work as hard as you do.

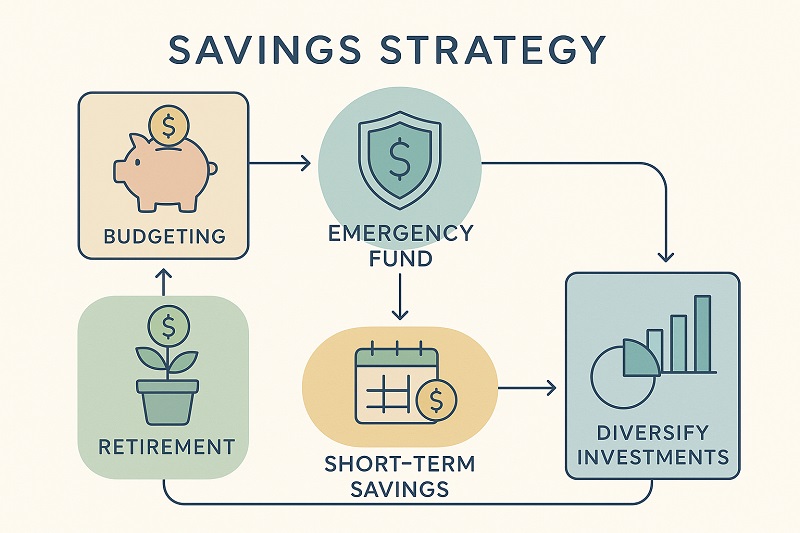

Creating a Comprehensive Savings Strategy

Planning for financial stability at 50 demands a well-rounded savings strategy that aligns with your long-term aspirations. As you set the stage for 2026, focusing on maximizing contributions to retirement accounts and saving effectively is key. These approaches not only enhance your retirement planning but also ensure your savings grow substantially over time. Developing a strategy that considers current financial planning and future stability will pave the way for a thriving retirement lifestyle. Understanding how to manage your accounts and optimize contributions can significantly impact your financial future, securing the lifestyle you desire.

Maximizing Contributions to Retirement Accounts

For investors approaching 50, maximizing contributions to retirement accounts is more than just a smart move, it’s a necessity. With 2026 on the horizon, you’ll need to leverage every opportunity to beef up your retirement savings. Start by examining your existing accounts, primarily 401(k)s and IRAs. These tax-advantaged vehicles are powerful tools in building a future-ready financial portfolio. The key to maximizing contributions lies in understanding the contribution limits for each account type, which can vary yearly. For instance, take advantage of catch-up contributions if you’re over 50, allowing you to deposit extra money annually. This is a small adjustment that can have significant compounding effects on your savings strategy.

Part of your financial planning should involve a deep dive into your current contributions to ensure you’re aligning with the maximum allowable limits. Many investors overlook the potential benefits of employer matching, which, while often seen as a bonus, should be viewed as a central component of your strategy. If your employer offers a match, not contributing enough to grab the full amount is essentially leaving free money on the table. For many, this match could be the difference between a stable and precarious retirement. As an investor, seek to consistently increase your contributions, even if incrementally. Small increases, like a one or two percent bump annually, can lead to substantial growth by the time you hit retirement.

Beyond adjustments in contributions, review the allocation of funds within your accounts. A diversified mix of stocks, bonds, and other assets tailored to your risk tolerance will enhance growth potential. Consider speaking with a financial advisor to ensure your investment choices align with your long-term goals and risk appetite. They can also assist in navigating the complexities of rollover accounts to avoid penalties or unnecessary taxes. Finally, automate your savings to minimize the temptation of skipping contributions during tighter financial periods. Consistency is crucial, and by automating, you build a hassle-free strategy that supports your 2026 financial planning goals. Embrace these strategies today, and you’ll ensure that your contributions are working as efficiently as possible, pushing you towards the financial freedom that comes with a well-funded retirement.

Here are actionable steps to optimize your retirement contributions now:

- Set a specific retirement savings goal to focus your contributions and track progress effectively.

- Maximize employer-matched contributions for a quick boost in your retirement savings balance.

- Automate contributions to consistently fund your retirement account without manual intervention.

- Increase your contribution rate annually, potentially timed with salary raises for minimal lifestyle impact.

- Ensure you’re using tax-advantaged accounts to reduce taxable income and grow wealth efficiently.

- Review investment options to ensure your retirement portfolio aligns with your financial goals and risk tolerance.

- Consider diversifying retirement accounts beyond the traditional offerings for broader asset exposure.

Implementing these steps can solidify your retirement strategy while maximizing your savings potential.

Saving Effectively for Future Financial Stability

Saving effectively is key to securing financial stability, particularly as you edge closer to 50. Balancing short-term desires with long-term retirement goals requires a focused financial planning strategy. Begin by taking a comprehensive view of your personal and retirement accounts, setting ground rules for future stability. Establishing a disciplined savings routine excludes room for haphazard financial decisions, which could derail years of careful planning. Start by creating a detailed budget that earmarks a percentage of your income specifically for savings and investments. Aim for balance, prioritize necessary expenses while leaving room for savings and contributions to flourish.

One of the most impactful ways to enhance your financial stability is through a detailed understanding of how your money flows. Categorize all expenses carefully, distinguishing between needs and wants. Cut back on unnecessary costs and redirect those funds into retirement or savings accounts. This approach aligns with a strategic foundation, which is crucial for future-focused planning. Key financial tactics include setting automatic transfers to savings accounts, fostering discipline and consistent growth, and ensuring no opportunity slips through the cracks due to oversight or procrastination.

Looking towards 2026, be conscious of inflation’s effect on your purchasing power. It’s an investor’s foresight to account for economic fluctuations. Your retirement funds need to outpace inflation, ensuring they retain their value and effectively fulfill your future needs. Engage in investments that promise resilience against inflation, assets like stocks, real estate, or inflation-protected bonds can be valuable additions to your portfolio. Each step toward financial planning should be intentional, with your future stability as the central focus.

Consider professional guidance to fine-tune your strategy as well. A financial planner can provide insights tailored specifically to your circumstances, offering wisdom that might not be apparent in your review. They can help identify unconscious biases in your spending habits or highlight changes in tax laws that could affect your savings approach. Embrace a personal financial review to assess progress, adjust plans, and cement savings practices that promise long-term security. Effective saving is about more than just setting money aside; it’s about driving your future stability by channeling your resources wisely, preparing robust defenses against the uncertainties of life. Take these steps now to pave the path for a financially sound retirement where your stability is unwavering and your lifestyle dreams are fully realized.

Building a Robust Investment Portfolio

Reaching 50 marks a pivotal moment to refine your investment strategy for a financially secure 2026. A robust investment portfolio is key to securing a comfortable retirement and managing financial risk. This involves diversifying investments to cushion against market volatility and seeking personalized advice from financial planners. With a deep understanding of your financial goals, you can build a tailored portfolio that meets your retirement aspirations while minimizing potential downfalls, ensuring that your wealth continues to grow steadily towards a stable future.

Diversifying Investments for Security at 50

Diversification remains a cornerstone of protecting your investment portfolio, especially as you approach 50. At this stage, you want to mitigate risks while ensuring steady growth, preparing for retirement with confidence. The aim is to spread investments across various asset classes such as stocks, bonds, real estate, and emerging markets. Each asset class reacts differently to economic shifts, helping stabilize your portfolio during unpredictable market turns. For instance, while stocks might offer robust growth, they also carry higher risks. Bonds, though offering lower returns, provide stability and can counterbalance more volatile assets in your portfolio.

One effective method is allocating assets based on your risk tolerance and retirement timeline, a pivotal aspect of personal financial planning. For those comfortable with heightened risk, aligning a larger portion of your portfolio in equities might be advantageous. Conversely, if preserving capital is your priority, consider tilting towards bonds or even gold, which has historically been a safe haven during economic downturns. Additionally, diversifying globally can provide further insulation against domestic market fluctuations. Investing in international markets opens up opportunities for growth and reduces reliance on a single economy, crucial for long-term investment, especially approaching 2026.

Regularly reassessing your portfolio’s diversification strategy with a keen eye on market trends is crucial. Over time, some investments will outperform others, potentially skewing your original allocation. Rebalancing ensures your portfolio remains aligned with your financial strategy. As an investor nearing 50, consider consulting a financial planner to tailor an investment diversification plan specific to your unique financial situation. This partnership can offer personalized insights to refine your portfolio approach, thus enhancing your overall financial security as you prepare for retirement. Such strategies ensure that your portfolio not only safeguards your assets but also positions you robustly for whatever the financial world may offer.

Working with a Financial Planner for Personalized Advice

Partnering with a financial planner can be a game-changer as you carve out a path toward retirement. This collaboration ensures that your investment strategy is aligned with your personal goals and risk tolerance, offering the personalized advice crucial for sound financial planning. A financial planner wears many hats, analyst, strategist, and confidant, helping you navigate the complexities of investments while planning for retirement. With their expertise, you can efficiently manage your assets and prepare for the evolving financial landscape, especially as 2026 draws closer with its unique economic challenges.

For investors at 50, who may have complex portfolios and diversified interests, the role of a financial planner is to provide strategy optimization. They conduct in-depth analyses of your current financial standing, evaluating existing investments while offering insights on potential improvements. By understanding the scope of your retirement ambitions, a planner ensures your portfolio is poised to meet those specific needs. This could include advice on expanding into international markets or crafting a retirement account strategy that maximizes tax advantages and employer contributions.

Moreover, financial planners serve as accountability partners in your financial journey, keeping you focused and disciplined. They conduct regular financial health check-ups, recalibrating strategies as needed to ensure alignment with your long-term goals. This constant reassessment is vital as life circumstances and market conditions change, requiring nimble adjustments. They can also illuminate opportunities you might have overlooked, be it estate planning tactics or advantageous shifts in market conditions ripe for investment. Engaging a financial planner transforms your retirement planning into a dynamic and informed process, reducing potential risks and enhancing the security of your investments.

The value of working with a financial planner rests in the peace of mind that comes from knowing your financial future is charted by a seasoned expert. Their guidance allows you to embrace retirement with assurance, knowing your investments are tailored to secure the lifestyle you desire. As an investor, this partnership sets the foundation for not just any retirement, but one where financial freedom is a lived reality, marked by stability, growth, and fulfillment. It’s a strategic move that ensures your portfolio supports, rather than hinders, your retirement aspirations.

Achieving financial stability by age 50 is a practical goal with effective planning, smart saving, and strategic investments. By prioritizing savings now, leveraging tax-advantaged accounts, and diversifying your investment portfolio, you can ensure a comfortable lifestyle for the years to come. Start today by assessing your current financial situation and projecting your future needs to avoid any pitfalls. Remember, the earlier you start, the better positioned you’ll be to meet your financial goals. Consider consulting with a financial advisor to tailor a plan that suits your unique future needs and aspirations.

FAQ: The Savings You Need in 2026

What are the essential steps for planning a financially stable future by age 50?

Planning for a financially stable future involves several key actions:

- Maximize contributions to retirement accounts.

- Set clear retirement goals.

- Understand your retirement lifestyle needs.

- Efficiently manage and review your expenses.

- Create a robust investment portfolio by diversifying.

How can I optimize my investment portfolio as I approach age 50?

To optimize your investment portfolio:

- Adjust your risk exposure to align with your retirement timeline.

- Diversify across asset classes such as stocks, bonds, and real estate.

- Consistently review and rebalance your portfolio.

- Consider seeking personalized advice from financial planners.

Why is it important to assess retirement lifestyle needs?

Assessing your retirement lifestyle needs helps:

- Achieve a balanced approach between financial means and aspirations.

- Forecast retirement expenses accurately.

- Understand financial requirements based on desired lifestyle.

- Prepare for potential changes in healthcare and living costs.

What strategies can boost my savings as I plan for retirement?

Effective savings strategies include:

- Implementing strict budgeting and automatic savings.

- Identifying saving opportunities within fixed and variable expenses.

- Maximizing contributions to tax-advantaged retirement accounts.

- Utilizing the power of compound interest.

How can working with a financial planner benefit my retirement planning?

Benefits of working with a financial planner include:

- Assistance in navigating complex tax and estate planning.

- Expert advice tailored to your unique financial needs.

- Strategies to maximize investment and savings opportunities.

- Regular financial check-ups to reassess goals and strategies.