Achieving the maximum Social Security benefits at retirement can significantly enhance financial security, making it a crucial consideration for savvy investors planning their golden years. This guide will delve into the essential steps needed to qualify for these top-tier benefits, focusing on strategic earnings, optimal retirement timing, and the impact of inflation adjustments. Understanding these factors empowers you to craft a retirement plan that maximizes your benefits, supporting a comfortable and stress-free retirement lifestyle. Ready to unlock the full potential of your Social Security benefits? Dive into our expert insights and start planning today.

Brief Overview

Achieving the maximum Social Security benefits at retirement age involves strategic planning around your earnings, retirement timing, and tax considerations. By understanding the importance of reaching maximum taxable earnings and delaying benefits claims, you can significantly enhance your retirement income. This guide emphasizes the role of careful financial planning and offers practical tips for investors to optimize their Social Security benefits. Dive into expert advice to ensure a well-funded, stress-free retirement and avoid leaving money on the table. Start planning today for financial security in your later years.

Key Highlights

- Maximize Social Security by strategizing your retirement age, earnings, and work lifespan.

- Delaying retirement past full retirement age can boost monthly benefits significantly.

- Consistent maximum-taxable earnings enhance potential Social Security payouts.

- Track earnings meticulously to identify shortfalls and optimize benefits calculations.

- Early retirement leads to reduced benefits; plan financial strategies accordingly.

Understanding the Maximum Social Security Benefits

Diving into the world of Social Security, it’s vital to comprehend how you can qualify for the maximum social security benefits. Every investor should know that the path to achieving the highest benefits involves strategic planning and understanding certain factors. With an eye on maximizing your retirement benefits, understanding the full retirement age (FRA) and how your earnings play a crucial role is essential. Oh, and let’s not forget to consider aspects like maximum-taxable earnings and retirement credit. With a keen focus on these elements, you’ll be better equipped to navigate personal finance decisions and secure your financial future.

Factors Influencing the Maximum Benefits

To ensure you’re on the right path toward securing the maximum social security benefits, it’s crucial to understand the key factors influencing this outcome. First and foremost, your earnings history plays a pivotal role. Consistently maximizing your earnings over your career is fundamental to attaining the highest benefits. The Social Security Administration (SSA) calculates your retirement benefits based on your average indexed monthly earnings (AIME) during your 35 highest-earning years. For many, this means the longer you engage in full-time work with a substantial salary, the better your chances of qualifying for increased benefits.

Aiming for maximum-taxable earnings each year is another influential factor. The SSA sets a cap on how much of your income is subject to Social Security tax, known as the maximum taxable income. By consistently hitting this ceiling, you ensure that your earnings will effectively contribute toward achieving the highest possible benefits. It’s also vital to consider your full retirement age (FRA). Choosing to retire at or after your FRA allows you to receive full benefits, while retiring earlier results in reduced payments.

Retirement credits are an additional layer to consider when strategizing for financial success. By delaying retirement beyond your FRA, you can earn retirement credits, thereby increasing your benefits amounts. This strategy requires careful planning, taking into account both immediate and long-term financial goals. Incorporating these factors into your financial planning offers you a way forward to not only secure a substantial benefits but also craft a well-rounded retirement strategy. Eager investors must dive deep into these elements, optimizing their work, earnings, and timing to reap maximum rewards from their social security benefits.

Strategies to Maximize Your Security Benefits

Having understood the various factors influencing your Social Security benefits, it’s time to delve into actionable strategies to maximize your security benefits. One primary approach is maintaining consistent, high earnings, particularly during your peak earning years. This means not only aiming for a high salary but also considering additional revenue streams that contribute to your maximum taxable income. As an investor, being strategic with your earnings allows you to reap a richer harvest when it comes to your retirement benefits.

Another critical strategy involves astute timing of when to start collecting your Social Security benefits. While you can begin withdrawing benefits at age 62, waiting until you reach your full retirement age or even opting for delayed retirement credits can vastly increase your benefits. The SSA offers an increase of up to 8% per year for each year you delay your benefits past your FRA until age 70. Deciding the right time to apply requires balancing your current financial needs with longer-term earnings potential.

Tax considerations shouldn’t be overlooked either. Planning for taxes on your benefits and structuring your retirement income to minimize unnecessary reductions can enhance your overall financial outcome. By thinking proactively about taxes, social security benefits, and retirement, you can optimize for a more favorable financial position. And, of course, staying informed about changes in social security policies and adapting your strategies accordingly keeps your plan dynamic and responsive. For motivated individuals focused on personal finance planning, leveraging these insights and strategies will not only maximize your security benefits but also position you for a prosperous retirement. Remember, the goal is to achieve financial stability through careful and informed planning.

Role of Maximum-Taxable Earnings in Social Security

Understanding the role of maximum-taxable earnings is essential for investors eyeing the highest social security benefits. These earnings directly affect your retirement benefits by influencing how much of your income is assessed for Social Security taxes. Consistently reaching the cap on these earnings can significantly elevate your retirement benefits. Additionally, tracking these earnings throughout your career is a crucial strategy in financial planning. It ensures that you’re precisely calculating your potential benefits as you aim for monetary growth in retirement.

How Maximum-Taxable Earnings Impact Benefits

Delving into maximum-taxable earnings reveals how they form the backbone of achieving the best financial outcomes in retirement. The Social Security Administration has set a cap on these earnings, known as the maximum taxable income, which determines how much of your income is subject to Social Security tax. This cap impacts your retirement benefits because only earnings up to this limit will count toward your social security taxes, influencing the benefits amount you’ll receive at full retirement age (FRA). By consistently reviewing and understanding this annual limit, which adjusts for inflation, investors can strategically plan their career earnings to hit this ceiling yearly, maximizing their contributions and, hence, their potential benefits.

Your earnings play a significant role in your average indexed monthly earnings (AIME), a factor the SSA uses to compute your retirement benefits. Only the 35 years of your highest earnings impact this calculation. Therefore, ensuring that each of these years meets or surpasses the maximum-taxable earnings threshold can substantially enhance your social security outlook. This consideration becomes even more critical for those in full-time work, where maximizing yearly contributions can effectively lock in higher monthly benefits upon retirement.

Furthermore, planning your retirement timing also dovetails with assessing your maximum-taxable earnings. If you retire post-FRA, you’ll benefits from retirement credits that add up beyond just hitting the earnings cap. Inflated benefits due to delayed retirement credits can be a game-changer in ensuring a robust financial future as you transition out of work. Therefore, understanding and maximizing these earnings is not just a routine financial task but a tactical move towards a successful retirement strategy, offering practical benefits for those willing to plan meticulously.

Tracking Your Earnings for Optimal Benefits

For investors aiming to snag the maximum benefits from Social Security, keeping a close watch on your earnings is crucial. This proactive approach ensures you draw the highest retirement benefits possible. It requires a well-crafted strategy to track your career-long earnings, ensuring that they consistently maximize your social security inputs. You must have earned a maximum taxable income frequently to optimize your retirement benefits fully. This entails thoroughly planning your career path, ensuring high earnings, and utilizing a reliable financial calculator to project your future social security benefits accurately.

Tracking should begin with a detailed review of your annual Social Security Statement. This document offers a glimpse of your expected retirement benefits, based on your recorded earnings. By regularly verifying this statement, you ensure it correctly reflects your earnings history and helps you plan for your full retirement. Discrepancies in reported earnings can lead to reduced benefits calculations, undercutting the substantial retirement life you’re planning. An integral aspect of financial planning is also forecast adjustments needed if earnings fluctuate due to changes in employment or reduced hours of work later in your career.

Another benefits of monitoring your earnings is the early identification of periods when your earnings fall below average. By recognizing these gaps or downturns, you can strategize to boost earnings through additional work, investments, or engaging in freelance efforts to counter these low periods. Such steps ensure you’re always in a position to maximize the taxable income needed for an optimum retirement benefits. The key takeaway for any investor is that consistent, proactive earnings monitoring can contribute significantly to your financial health. It’s about strategically positioning yourself to achieve the highest return on your social security benefits come retirement, aligning your work-life contributions with a financially rewarding retirement strategy.

To fully leverage these strategies and secure your financial future, consider implementing these additional tips:

- Consider delaying your Social Security benefits claims to potentially increase your monthly payouts.

- Explore spousal benefits if you’re married, as it can offer a larger benefits based on your partner’s record.

- Understand the impact of taxes on your Social Security benefits and strategize accordingly to minimize tax liabilities.

- Stay informed about legislative changes that could affect your benefits and continuously update your retirement plan.

- Engage with a financial advisor specializing in retirement planning for personalized insights and strategies.

- Evaluate your health and longevity prospects to make informed decisions about the timing and structure of your benefits.

These additional measures can help ensure a comprehensive approach to maximizing your retirement benefits, making your post-career years both secure and satisfying.

The Importance of Retirement Age in Benefits Calculation

Finding the right retirement age is more than just picking a date to stop working; it’s a strategic decision that profoundly impacts your maximum social security benefits. Understanding how retirement age affects the calculation of your benefits is crucial if you want to maximize your financial rewards in later life. If you’re considering retiring early or later, it can shape your benefits amounts significantly. We’ll explore how timing plays a role in retirement planning and how your choices today can lead to fulfilling financial years ahead.

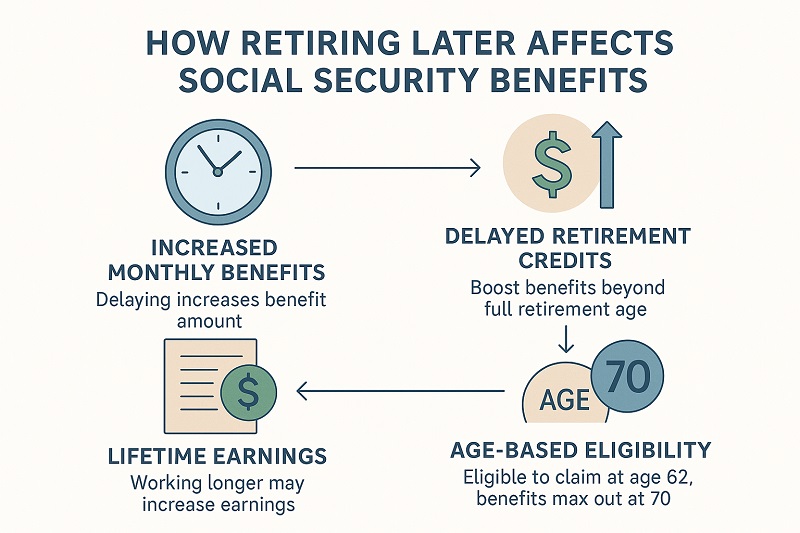

How Retiring Later Affects Your Social Security

Retirement is a significant milestone, and the timing of when you commence this new phase can influence your financial well-being profoundly. When you choose to retire later, specifically beyond your full retirement age (FRA), you’re in a position to accumulate what are known as delayed retirement credits. These credits, calculated by the Social Security Administration, can increase your monthly payout by up to 8% for each year you delay retirement past FRA, up to the age of 70. This percentage might not seem significant at first glance, but over time, the compounded effect can lead to substantial increases in your overall social security benefits.

The decision to work longer also means additional years of earnings, which can be crucial in the calculation of your average indexed monthly earnings (AIME). Since Social Security utilizes your highest 35 years of earnings to determine your benefits amount, additional years at a higher income can replace lower-earning years, boosting your AIME and, consequently, your benefits amounts. For investors, this means more than just waiting for higher payouts; it involves strategic career planning to align high earning years with your decision to delay retirement.

Another factor to consider is life expectancy. If you have a family history of longevity or are in good health, retiring later to maximize social security might be financially beneficial. It’s also crucial to factor in how long your retirement savings need to last. Delaying claiming your social security benefits can be a safeguard against outliving your savings. Moreover, if you’re thinking about maintaining your lifestyle well into retirement, those few extra years of working can offer financial advantages that go beyond the immediate increases in monthly benefits. The critical takeaway for investors is to balance the potential larger benefits from delayed retirement with personal health, lifestyle plans, and financial needs.

Choosing the Right Retirement Age for Maximum Benefits

Choosing your retirement age is indeed a pivotal decision, with direct implications for the maximum social security benefits you can receive. While the allure of early retirement might be tempting, claiming benefits before reaching full retirement age (FRA) generally results in a permanent reduction of your monthly benefits. This reduction can be as much as 25-30%, which signifies a considerable drop over the retirement span, impacting your financial stability. On the other hand, waiting until you reach FRA, or possibly delaying further, ensures you receive full benefits, and you can even increase your total benefits amount by using retirement credits for delays beyond FRA.

Planning when to retire is not merely about the numbers; it’s about assessing your overall financial health, lifestyle aspirations, and long-term goals. For investors, it’s instructive to integrate social security into a broader retirement strategy that accommodates other income sources, investments, and personal savings. By aligning this strategy with your expected and planned retirement age, you ensure a more comprehensive approach to securing financial stability. An investment in planning can provide enduring rewards, aiding in reaching full retirement with peace of mind.

Additionally, it’s vital to consider the concept of life-span financial balance. This approach involves weighing how your work life and retirement plans impact each other. For instance, you might choose to work part-time as you ease into retirement while receiving social security benefits or structured withdrawals from 401(k) plans. By doing so, you’re not just relying on social security but building a diversified income plan, allowing you to live comfortably while benefiting from social security’s structured increases. The right planning can lead to achieving not just the highest benefits, but a sustainable, rewarding retirement that aligns with your financial forethought and lifestyle choices. Hence, identifying the right retirement age is crucial for shaping a financially secure future that harmonizes well with your personal and family goals.

Strategizing Work and its Impact on Benefits

Your work and earnings significantly shape the Social Security benefits you can expect in retirement. Understanding how to strategize around your employment life, from the timing of retirement to maximizing your earnings, can lead you to a substantial financial reward in your later years. Approaching this with a clear plan not only influences your potential benefits but also offers a pathway toward achieving maximum security benefits. Considerations include working longer for higher benefits or understanding potential losses with early retirement, which can impact your financial planning goals. Let’s explore these strategies further.

Work Longer, Earn More: Increasing Your Social Security Benefits

When it comes to securing the maximum social security benefits, extending your work life can be a game changer. The longer you work and contribute to the Social Security system, the higher your monthly benefits will likely be upon retirement. Each year you delay retirement past your full retirement age (FRA) up to age 70 accrues delayed retirement credits, bumping your benefits by approximately 8% each year. For investors, this isn’t just about waiting out the clock; it translates to tangible financial gains that can significantly impact your retirement lifestyle. The math is straightforward – by working longer, you not only increase your earnings which affect your average indexed monthly earnings (AIME) but also optimize the retirement credits that boost your security benefits.

Moreover, each additional year worked within this time frame could potentially replace lower earning years in the calculation of your AIME, which is based on your highest 35 years of earnings. This contributes to securing the maximum social security benefits as it ensures your most financially productive years are reflected in your benefits. Not only does this impact your monthly checks, but it also compounds over your retirement, potentially leaving you in a much healthier financial position.

It’s also crucial for investors to integrate these decisions with broader financial and retirement planning strategies. By synchronizing your extended work plans with investment growth, you can harness the ultimate benefits of compounded savings alongside increased social security payouts. This approach means not just surviving financially through retirement but thriving with ample resources to enjoy this new phase of life. If you’re visualizing a retirement filled with opportunities rather than constraints, working longer may pave a path to achieving the ultimate financial freedom. Think of it not just as stretching your career, but strategically sculpting your most financially rewarding life chapter. It’s a strategy that requires careful planning but leads to a robust retirement foundation.

Balancing Early Retirement with Potential Benefits Loss

The allure of early retirement draws many, but it’s a decision that requires careful financial consideration. Retiring before reaching your full FRA can lead to a reduction in your monthly benefits, often substantial enough to reshape your retirement finances. By electing to apply for benefits early, your monthly payout is permanently reduced, by as much as 25-30%. That could translate into a lower total lifetime payout, depending on your lifespan and financial needs post-retirement. This trade-off must be weighed carefully, especially for those whose retirement savings might not adequately compensate for the reduced social security benefits.

Financial planning for early retirement must include a detailed analysis of your available resources. For many investors, blending income streams might offer a feasible solution, allowing for a partial supplement to your early benefits withdrawals. This could involve structuring withdrawals from investment accounts like IRAs or 401(k)s, taking up part-time work, or gradually reducing work hours. Balancing these alongside your reduced social security benefits can offer a multifaceted approach to managing early retirement finances.

Moreover, it’s essential to consider the long-term implications, such as inflation and healthcare costs, which can erode your purchasing power over time. While you may plan to enjoy the early years of retirement filled with travel or indulgence, planning for the longevity of your financial health is crucial. Investors focus not only on the immediate freedom of early retirement but also on the sustained quality of life decades down the line, seeing their strategies as a marathon rather than a sprint. Effective financial planning can help align expectations with realities, ensuring that early retirement doesn’t lead to financial strain later. Thus, while early retirement is tantalizing, it is an investment in both time and money, requiring a structured approach to truly benefits all financial phases of your retirement journey.

Achieving the Highest Possible Social Security Benefits

Maximizing your Social Security benefits requires careful planning and strategic decisions, especially for investors. The quest for securing the highest benefits involves understanding how earnings, timing, and work-life balance play critical roles. By focusing on practical tips designed for investors, you can navigate these elements effectively. Whether it’s learning about earnings optimization or strategizing retirement age decisions, these insights can significantly impact your financial outcomes. Engaging with these factors will not only help you qualify for a maximum benefits but also safeguard your financial stability in retirement.

Practical Tips for Investors and Traders

For those looking to maximize their social security benefits, it can’t just be about going through the motions. Investors and traders have unique opportunities to strategically plan for an optimal payout. A significant step is understanding how to align your earnings with the goal of achieving the maximum benefits. By focusing on maximizing your earnings, especially during your 35 highest-earning years, you can ensure that you hit the maximum taxable earnings threshold as often as possible. This isn’t just about earning more; it’s about structuring your income streams to benefits most from the social security system. For traders, this might mean balancing volatility in investment income with stable, taxable earnings that contribute toward your benefits calculation.

Besides, timing plays a pivotal role. Retiring early may sound appealing, but if you’re aiming for the maximum benefits, delaying your claim until at least full retirement age – or later, to 70 – can significantly enhance your benefits due to the delayed retirement credits. This decision must be balanced with your personal financial situation and life expectancy considerations. Trading off immediate smaller payouts for substantially larger monthly benefits later is often a wise financial move but requires a disciplined approach to other income sources during the intervening years.

Investors should also not overlook the importance of continued financial education and staying updated on how changes in policy or market conditions could impact their social security benefits. Making informed decisions requires constantly learning and adapting strategies to align with current opportunities and challenges. Furthermore, engaging with experienced financial planners who understand personal finance nuances can offer personalized advice to ensure your paths align with your financial goals. All these practical approaches are crucial, not just for securing a maximum benefits, but for laying down a robust roadmap for financial stability throughout retirement. Therefore, the focus shouldn’t solely be on the figures but on the strategies that can mold financial success in both present and future retirement landscapes.

Understanding the nuances of qualifying for maximum Social Security benefits can significantly impact your retirement planning. By fully leveraging your earning years, delaying your benefits claims strategically, and optimizing your work history, you can boost your future financial security. Don’t leave money on the table; proactively manage your qualification journey. Consider professional advice to personalize your strategy. Start today to ensure a comfortable, financially stable retirement, paving the way towards peace of mind for you and your loved ones.