When most people think about big upside in the markets, they think stocks, tech, and speculation. Joel Litman and Rob Spivey at Altimetry are arguing that in 2026, the real “no‑brainer” opportunity is hiding in plain sight—mispriced, blue‑chip corporate bonds that could deliver 10%-plus annual income and 40%–100%+ total gains, with a risk profile they compare to Treasurys or better.

Their premium research service, Credit Cashflow Investor, is the vehicle they’ve built to help individual investors tap into this unusual credit anomaly. In this review, you’ll see why they call it their No. 1 trade for 2026, what you actually get when you join, and why they believe now—before Trump’s May 15 Fed deadline—is the moment to act.

The 2026 “This Simply Doesn’t Happen” Anomaly

The entire pitch revolves around a market setup Joel and Rob insist “simply doesn’t happen in a normal world.” They believe political and economic extremes—especially President Trump’s stated plan to “break the Fed” by replacing Jerome Powell and forcing rapid rate cuts back toward 1% or even zero—have created a once‑in‑a‑generation opening in high‑grade corporate bonds.

Here’s the core of their thesis:

-

The Fed’s ultra‑fast hikes in 2022–2023 drove short‑term Treasury yields to levels where even elite corporate bonds could not compete, forcing their prices down to 70, 60, even 50 cents on the dollar.

-

Now Trump is openly pushing for aggressive cuts, has attacked Powell, and plans to install a loyal Fed chair when Powell’s term ends May 15—what they call the key timing catalyst.

-

Once the market sees rates heading sharply lower, they expect money to flow out of Treasurys and back into high‑quality corporate bonds, driving those battered prices quickly back toward—or above—par.

Because bond prices and interest rates move like a seesaw, they argue this reversal could mean 40%–70% gains just from price normalization, plus rich interest streams that can push total returns toward 100% or more in 1–2 years. And crucially, they’re not talking about speculative “junk,” but debt from Magnificent Seven‑type giants like Apple, Microsoft, and Alphabet—names they say are as safe to lend to as the U.S. government.

To Joel and Rob, that combination—Treasury‑like risk with tech‑stock‑like upside in a tight window—makes these bonds “the financial move of the year” and the best risk‑reward setup they’ve seen in 15–20 years.

Why Bonds, Why Now, and Why Joel Litman?

Bonds as a “Port in the Storm”

In the presentation, Joel leans hard into the emotional reality of today’s markets: bubbles, AI hype, geopolitical shocks, and economic anxiety. His message is simple:

-

You can’t control politics, wars, or headlines.

-

You can move a meaningful chunk of your savings into contracts that are legally obligated to pay you interest and principal on a set schedule.

-

In this anomaly, doing that doesn’t mean settling for 2%–3% yields—it could mean aiming for 50%–70%+ total gains with what he calls “port in the storm” safety.

He emphasizes the comfort of:

-

Knowing exactly what you’re owed and when.

-

Having the U.S. legal system on your side if a company doesn’t pay.

-

Sitting above stockholders in the capital structure—bondholders get paid before dividends and buybacks.

For investors burned out on speculation, that mix of peace of mind and potential for outsized returns is the emotional cornerstone of Credit Cashflow Investor.

Joel Litman’s Track Record and Institutional Credibility

Altimetry isn’t positioning this as a new or untested idea. They lean heavily on Joel and Rob’s record:

-

In June 2008, Joel warned institutional investors about a coming “credit‑market heart attack” just before the market plunged 49%.

-

In March 2020, he urged clients to get into stocks almost at the pandemic bottom, catching the ensuing 100%+ rally.

-

Their institutional business serves all 10 of the world’s 10 biggest money managers plus hundreds of elite funds and even government agencies, with some clients paying up to $100,000 per month for their work.

-

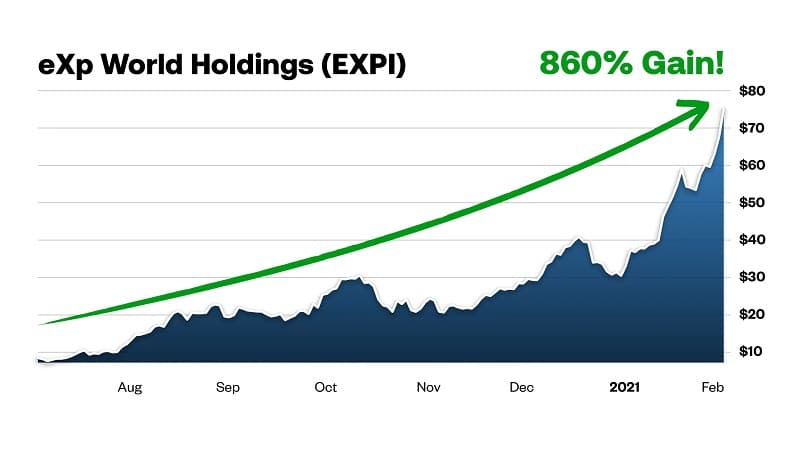

Using their framework, they’ve highlighted wins like 1,000% in Meta, 860% in eXp World Holdings, and hundreds of percent in other names for institutional clients and retail readers.

On the credit side:

-

Their institutional credit recommendations have delivered 105% cumulative gains versus 70% for the benchmark—about 50% outperformance.

-

For Altimetry subscribers, the bond strategy they’re now packaging in Credit Cashflow Investor has notched a 100% win rate on closed recommendations since launch, with examples like a 40% winner last summer and open positions with yields nearing 20%.

The message: this is not theory; it’s the same credit lens that institutions and agencies already rely on, now applied to a very specific 2026 window that Joel and Rob want individual investors to exploit.

The Secret Engine: Uniform Accounting and Credit Analysis

A big part of the appeal is the proprietary “plumbing” behind the recommendations: Uniform Accounting.

Joel argues that:

-

GAAP accounting—the system all public companies must use—is “worse than useless” at showing true business performance, echoing Warren Buffett’s criticisms.

-

Regulations have created a Frankenstein system with more than 70,000 pages of tax and reporting rules, which companies can use (legally) to obscure economic reality or even manipulate earnings.

Uniform Accounting aims to fix that by:

-

Making over 130 standardized adjustments to every financial statement.

-

Deploying a 100+‑person team plus algorithms built over decades.

-

Even analyzing deception and confidence in earnings calls using technology employed by Israel’s Mossad.

This same framework has already been used to:

-

Find massive stock winners for institutions (e.g., Lam Research, Broadcom, Meta).

-

Deliver multi‑bagger gains and large open winners to Altimetry’s stock research readers.

About two years ago, they extended Uniform Accounting directly into the credit markets for the public—giving regular investors the same bond‑screening edge their institutional clients have used for years. Credit Cashflow Investor is the distilled result of that shift.

How the Strategy Works: From “Distressed” to “Distressed‑Lite” Blue Chips

Bond Basics, Seesaws, and Legal Contracts

Rob spends a good portion of the presentation demystifying bonds. Key points:

-

A corporate bond is a simple legal contract: you lend, say, $1,000; the company owes you interest (usually semiannual) and your $1,000 back at maturity.

-

That $60 interest on a 6% coupon is fixed—no matter whether you paid $1,000, $700, or $500 for the bond in the market.

-

If the bond’s market price falls to $500, your yield doubles to 12%, and if it later gets paid at $1,000, you’ve also doubled your money in capital gains.

Because bond math is tied to contracts and maturity dates, Rob argues it’s far simpler than forecasting stock values, which depend on countless variables and future scenarios. The outcome is “binary”: you get paid or you don’t—and bondholders stand in line ahead of equity.

“Distressed” Branding vs. Reality

The huge opportunity, in their view, comes from mislabeling:

-

When a bond trades down to 70, 60, or 50 cents on the dollar, the market tends to brand it “junk” or “distressed,” scaring off most investors.

-

Using Uniform Accounting, Joel and Rob can look under the hood and see if the company truly struggles—or if it has plenty of cash and cashflow to pay its debts.

-

When they find a bond trading at distressed levels but sitting on fortress‑like fundamentals, they see a rare chance to lock in double‑digit yields and large, contract‑driven capital gains with risk they consider modest.

Historically, they’ve used this approach to:

-

Lock in 15%–17% annual yields in beaten‑down oil‑sector bonds when crude crashed, with some positions jumping 23%–32% in just two months.

-

Spot 64‑cent bonds from strong companies during 2008 that could deliver 12.5% yields plus 56% capital gains, more than doubling money during a 50% stock market crash.

Normally, these kinds of gains come from “true” distressed situations with high uncertainty about survival. What’s different now, they say, is that the Trump/Fed anomaly has created similar payoff structures in the bonds of world‑class, investment‑grade companies—“distressed‑lite” or better.

The Trump–Fed Catalyst: Why They Say You Must Act Before May 15

The political angle is foundational to the urgency of the offer.

According to the presentation:

-

President Trump has already demonstrated a willingness to tear up long‑standing norms, from appointing unconventional cabinet officials to reshaping agencies and even redeveloping parts of the White House.

-

Facing weak economic numbers and a critical midterm election year, he needs to juice the economy quickly.

-

He has repeatedly demanded faster and deeper rate cuts, launched investigations that Powell says are attacks on Fed independence, and stated his desire to replace Powell with a loyal chair when Powell’s term expires May 15.

Joel and Rob’s view:

-

Trump will get his way, pack the Fed with loyalists, and drive rates toward 1% or lower at record speed—not in response to crisis, but to solve an “affordability” and electoral problem.

-

The bond market will respond to the “writing on the wall” even before cuts are fully implemented, bidding up the very bonds they are recommending.

-

This makes the coming months—and especially the period before and around May 15—the key window to position yourself.

They note that Powell has already cut rates three times in recent months, and bond prices are already moving. A change at the Fed could mark the end of the best entry prices, not the beginning, which is why they frame the trade as urgent.

What You Get With a Credit Cashflow Investor Subscription

Credit Cashflow Investor is sold as the culmination of 20+ years of Joel and Rob’s work on credit, packaged for individual investors with a time‑sensitive 2026 focus.

One Full Year of Credit Cashflow Investor (50% Off)

Regular price: $5,000. Under the current offer, you get:

-

One year for $2,500—a 50% discount they emphasize is likely the best they’ll ever offer on this package.

-

Monthly issues with new high‑yield, blue‑chip bond recommendations designed to target double‑digit yields and often 50%–100%+ total return potential.

-

Access to the full model portfolio, including all open bond recommendations, target ranges, and sell guidance as events unfold.

-

Commentary and updates as the credit crisis and Trump anomaly develop, helping you decide when to add, hold, or exit.

This is the core engine that steers you through the 2026 bond play with step‑by‑step guidance.

Flagship Bond Reports: The Core Trades

You also get immediate access to several anchor reports that spell out the specific opportunities Joel and Rob consider their “No. 1 trade of 2026.”

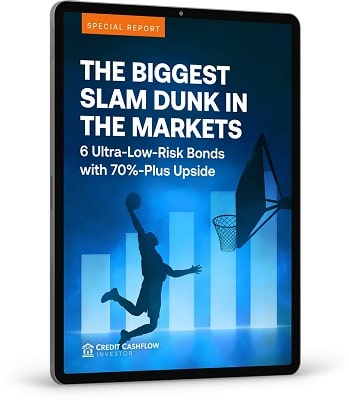

The Biggest Slam Dunk in the Markets: 6 Ultra‑Low‑Risk Bonds With 70%-Plus Upside

In this lead report, they lay out six investment‑grade, blue‑chip bonds that:

-

Currently trade at steep discounts—below 70 cents on the dollar.

-

Offer roughly 41%–44% upside just to reach par, based on recent pricing.

-

Traded above par—around $1,200—in the last era of ultra‑low rates, implying 67%–72% upside if history rhymes.

-

Come from elite issuers they regard as “fortress” credits, with risk profiles similar to Treasurys.

Rob explains that even buying one or two bonds in each of these issues could produce gains that exceed the subscription cost, before counting interest.

The Best Bond Opportunities We’ve Ever Seen

After assembling the “slam dunk” six, the team identified two more standout ideas they consider even better.

This report highlights:

-

A bond from a world‑famous tech giant—used daily by millions—with a credit rating higher than the United States, yet trading below 60 cents on the dollar.

-

A blue‑chip name trading near 50 cents on the dollar, with the prospect of doubling your money on capital gains alone if it returns to par, plus ~5% annual interest while you wait.

Together, these eight bonds constitute the core trade Joel and Rob are urging readers to make in 2026.

The List: 29 Blue‑Chip Bonds That Could Rapidly Reprice Higher in 2026

To broaden your opportunity set, they also include a high‑value shortlist derived from a proprietary screen of tens of thousands of bond issues.

Criteria:

-

Investment‑grade bonds trading below 70 cents on the dollar.

-

Minimum current yields of at least 5%.

-

Issued by strong companies that pass their Uniform Accounting checks.

The resulting 29 names are not tracked recommendations but serve as a powerful “watch list” you can use to build diversification or hunt for additional bargains as rates move.

Barbell Strategy: Bonds Plus Breakout Stocks

While they call these bonds the “no‑brainer trade of the year,” Joel and Rob are clear that they still want subscribers to own stocks. To round out the package, they add a high‑momentum equity angle.

Three Breakout Stocks That Could Double in 2026 (Value: $1,000)

This report pulls from their new Breakout Profits research (read full review here), which:

-

Uses a momentum‑plus‑quality framework: stocks that have already doubled in the current bull market and pass a seven‑factor screen based on Uniform Accounting.

-

Targets names that have a statistically higher chance of doubling again, rather than chasing crowded trades like Nvidia purely on hype.

These three stocks aren’t being followed elsewhere in Altimetry’s lower‑priced services; they’re carved out of a $5,000‑per‑year service and conservatively valued at $1,000 for this report—then included at no extra cost.

Joel and Rob present this as a “barbell” approach: ultra‑low‑risk bonds with big upside on one end, carefully selected breakout stocks on the other, together forming a balanced 2026 game plan.

Tools and Education: Turning You Into a Credit‑Savvy Investor

Beyond recommendations, Credit Cashflow Investor aims to change how you see the markets by giving you professional‑grade tools and training.

The Secrets of Credit: Our Credit Cashflow Investor Strategy

This handbook is the educational backbone of the offer. It explains:

-

How bonds work in practice—mechanics, maturities, coupons, and where to buy them.

-

How Joel and Rob screen for opportunities, evaluate credit health, and confirm that bonds will likely pay in full and on time.

-

How credit leads equity, acting like the “wind” that moves the stock‑market “weathervane,” and why understanding credit gives you an edge most investors lack.

Joel himself says this knowledge is worth more than anything else in the package because it can reshape how you invest for the rest of your life.

Credit Analyzer (1 Year Free – $2,388 Value)

The Credit Analyzer is Altimetry’s new credit‑screening engine built specifically for individual investors.

It lets you:

-

Quickly pull up the credit profile of almost any U.S. company.

-

See through the distortions of GAAP and credit‑rating labels to the firm’s true ability to service debt.

-

Avoid owning stocks or bonds in businesses with hidden credit rot.

Altimetry values this at $2,388 annually, and until now, their detailed credit work has been reserved for institutional clients, including the world’s largest asset managers and even intelligence agencies. You get a full year included with your membership.

Altimeter Pro (1 Year Free – $2,388 Value)

Altimeter Pro is the equity cousin of the Credit Analyzer:

-

It grades virtually any U.S. stock using the full Uniform Accounting framework.

-

It corrects the 130 most common accounting distortions, giving you a simple “buy” or “sell” style grade based on real economic earnings and valuation.

-

It helps you vet any stock in your portfolio or watchlist on demand.

During an uncertain stock environment, Joel and Rob view this as critical for cutting through noise and spotting mispriced quality.

Timetable Investor (1 Year Free – $199 Value)

Timetable Investor is a monthly macro letter designed to keep you ahead of big picture shifts:

-

It summarizes key signals—credit spreads, rates, macro trends—and spells out how to position for the next 3–24 months.

-

It currently focuses on the Trump–Fed standoff, the unusual rate setup, and how those forces could ripple through bonds, stocks, and the broader economy in 2026.

This gives you context for why the Credit Cashflow Investor strategy exists and when to press harder or ease off.