As retirement looms on the horizon, many investors eagerly anticipate the freedom it promises, yet a surprising number of retirees continue to underestimate crucial expenses that can derail their plans. In 2026, an evolving financial landscape has seen these costs shifting, catching even seasoned planners off-guard. Beyond the standard budget lines, unexpected healthcare needs, rising inflation, and increased leisure spending are carving deeper holes in retirement savings. Understanding these underestimated expenses can empower you to build a robust, strategic plan that ensures you enjoy your golden years without financial strain. Let’s explore these often-overlooked aspects of retirement planning in 2026.

Key Highlights

- Retirees often underestimate expenses like healthcare, inflation, and leisure, risking financial stability in 2026 retirement planning.

- Unexpected healthcare costs, including long-term care, can quickly deplete retirement savings if not adequately planned for.

- Establishing a dedicated emergency fund helps manage unforeseen financial challenges without touching primary savings.

- Long-term care insurance and regular financial plan reviews are crucial for protecting against unexpected costs.

- Comprehensive home maintenance assessments and efficient management prevent budget strain from unforeseen repairs.

Understanding Unexpected Retirement Expenses

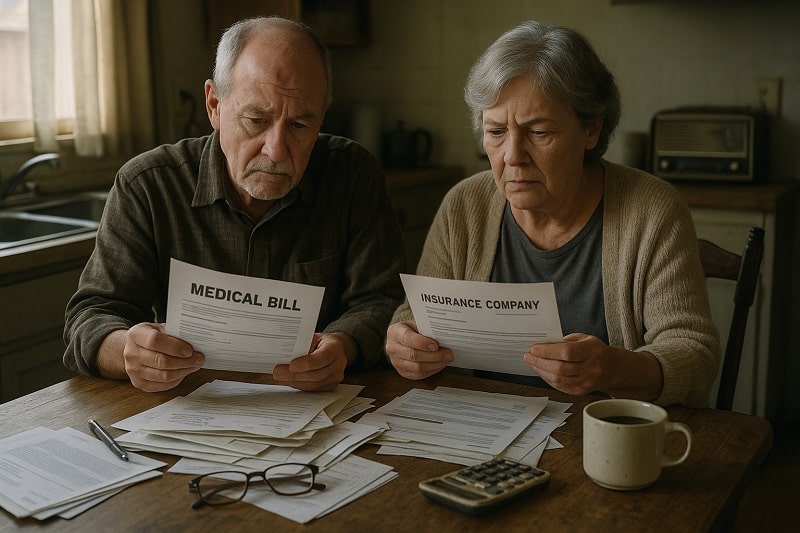

Many retirees find themselves blindsided by unexpected expenses that were not part of their initial financial plans. These unplanned expenses can quickly derail even the most carefully crafted retirement strategy, underscoring the importance of comprehensive retirement planning. Understanding these potential financial pitfalls is crucial for maintaining stability and maximizing your income and savings during your golden years.

From underestimating healthcare costs to the often-overlooked tax implications, these oversights can pose significant risks to retirees’ wealth and income. For example, long-term care expenses, such as nursing home care or home health aides, are frequently underestimated, draining savings more quickly than anticipated. Recognizing these gaps in planning enables retirees to implement effective strategies for managing and mitigating unexpected financial challenges, preserving financial independence and security.

Identifying Gaps in Retirement Planning

Retirement planning can sometimes feel like navigating a financial minefield, with unexpected expenses lurking around every corner. Many retirees underestimate the sheer variety and magnitude of expenses that can arise during retirement, often neglecting to consider unexpected tax liabilities or the long-term impact of inflation on their fixed income. Income streams that appeared ample during the planning phase might not stretch as far as anticipated when unplanned expenses surface. This oversight can lead to taking on avoidable burdens like credit or loans to cover shortfalls, eroding carefully accumulated savings.

It’s critical for retirees and those nearing retirement to scrutinize their financial plans meticulously, ensuring every potential expense is accounted for, including healthcare costs, property taxes, and potential dependency on medications. Failing to incorporate these expenses in the initial plan can result in significant financial stress. Moreover, lifestyle changes, such as traveling more or maintaining a large home, can unexpectedly inflate expenses. By anticipating these financial challenges, retirees can safeguard their income and preserve their financial independence, preventing a reduction in life quality due to unforeseen expenses.

Strategies for Managing Unexpected Expenses

Managing unexpected retirement expenses requires a proactive and dynamic approach. One of the most effective strategies is to establish a dedicated emergency fund specifically designed to cover unforeseen costs, acting as a financial buffer that mitigates the need to dip into primary retirement savings when unplanned expenses arise. This fund should be kept in a high-yield savings account to remain accessible and inflate over time. Retirees should also consider reallocating their investment portfolios to prioritize liquidity and lower-risk assets, ensuring quick access to funds without incurring significant losses.

Such strategic adjustments can significantly reduce vulnerability to market volatility, which can otherwise severely impact fixed income streams. Additionally, continuous financial planning is crucial; regularly reviewing and adjusting plans helps ensure they remain aligned with current economic conditions and personal circumstances. It’s also advantageous to explore supplemental income options, such as part-time work or monetizing hobbies, which can provide an additional financial cushion.

Engaging with financial services and seeking advice from a wealth management professional can offer invaluable insights for optimizing resources. By employing these strategies, retirees can maintain their financial health, ensuring a stable and secure retirement. Moreover, being open to lifestyle adaptations, such as downsizing to lower living expenses or relocating to areas with reduced cost of living, can substantially lower financial burdens. Practicing frugality, prioritizing spending, and avoiding unnecessary debt are also integral measures for managing financial health post-retirement.

The Impact of Healthcare Costs on Retirement

Healthcare costs have emerged as a dominant concern for retirees, frequently underestimated in retirement planning. As people age, healthcare becomes a significant financial priority, with Medicare covering only a portion of expected expenses. A detailed understanding of potential healthcare costs can prevent financial strain and ensure a secure retirement.

Retirees need to integrate healthcare expenses into their financial plans to safeguard their savings and maintain quality of life. From unexpected medical emergencies to routine services, navigating health care expenses without a clear strategy can deplete financial resources faster than many anticipate. Let’s explore how to adequately plan for these costs in your retirement strategy.

Estimating Healthcare Costs in Your Retirement Plan

Incorporating healthcare costs into your retirement plan is essential for financial stability. Traditionally, retirees inaccurately gauge how much they’ll spend on health care, often only considering Medicare as a comprehensive solution. But Medicare doesn’t cover everything. As you age, your need for medical services generally increases, potentially leading to unplanned expenses that surpass your initial estimates. Common services, like routine checkups and unexpected hospital visits, should be figured into your average yearly costs, and healthcare insurance premiums should also be accounted for as they fluctuate depending on age and health status.

Additionally, prescription medications can turn into significant expenses, especially when your income is fixed, and prices keep climbing. Having a detailed financial plan that considers these costs can prevent the erosion of your savings over time and ensure that you don’t inadvertently underestimate potential expenses. Allocating a portion of your resources to a flexible healthcare savings account can also be an advantageous step. This kind of planning, coupled with a strong focus on emergency healthcare funds, allows a more precise estimation, steering clear of common pitfalls. Engaging a financial advisor adept at retirement planning can provide tailored insights into estimating these unavoidable costs, ensuring your medical expenses don’t hinder your retirement quality.

Navigating health care expenses during retirement requires a proactive and informed approach, given most retirees underestimate these costs. While Medicare provides a safety net, it should not be considered a catch-all solution. Consider additional insurance options, such as Medigap or Medicare Advantage plans, to cover costs that Medicare doesn’t. These plans can mitigate expenses for services like dental, vision, and long-term care, which tend to go overlooked.

It’s crucial to stay informed about the health care market and any policy changes that could impact your costs. Beyond insurance, adopting a healthy lifestyle can reduce future healthcare expenses, potentially lowering the need for frequent medical intervention. Routine physical activity, a balanced diet, and regular health check-ups can delay the onset of chronic conditions common in seniors, offering indirect financial savings. Additionally, communicating transparently with your healthcare providers about your financial concerns can lead to more affordable treatment options.

Practical steps, like double-checking your medical bills for errors and negotiating lower charges when possible, can also help manage expenses. Building up a dedicated savings layer specifically for healthcare emergencies ensures access to necessary services without dipping into your primary retirement savings. Cultivating this holistic approach, combining smart insurance selections, healthy living, and vigilant financial management, enables retirees to navigate health care expenses without compromising their financial well-being or quality of life.

Long-term Care: A Hidden Retirement Cost

Long-term care is one of the most underestimated expenses that retirees face, yet it can have a significant impact on one’s retirement savings. As you age, the need for extended care services like nursing homes or in-home aids often becomes a reality. This underscores the importance of understanding and planning for these long-term care costs, which are frequently omitted from initial retirement calculations. Ignoring these expenses can drastically lower household wealth, leaving retirees financially vulnerable. Exploring long-term care insurance options and understanding income implications are essential steps in safeguarding your financial future.

Planning for Long-term Care Needs

Effective planning for long-term care is crucial for ensuring that these often substantial and unexpected expenses don’t derail your retirement. Many retirees underestimate the average long-term care costs, which can quickly deplete savings. To mitigate this, it’s vital to integrate long-term care expenses into your overall retirement plan. Start by evaluating your household’s specific needs; consider potential services such as in-home health aides or nursing facilities. This type of planning requires a detailed analysis of your income, projected expenses, and available resources. It’s not just about the financial impact but also about maintaining the quality of life in your later years without undue stress or sacrifice.

Utilizing tools like predictive calculators to gauge future care costs can be invaluable. These estimates allow you to visualize how expenses might evolve with inflation and other economic variables. Additionally, fortifying your financial plan with an emergency fund specifically for long-term care can act as a safeguard. Such a fund ensures you won’t need to liquidate critical assets prematurely.

Don’t overlook the potential contribution of Medicare in your planning. While Medicare covers some costs, it falls short for comprehensive long-term care needs. Therefore, understanding Medicare’s limitations and integrating this knowledge into your planning is essential. Begin discussions with family members early to align expectations and responsibilities. Collaborating with a financial advisor can provide further insights, ensuring that your long-term care planning is both thorough and realistic. By taking these proactive measures, retirees can better shield themselves from unforeseen financial burdens associated with long-term care expenses.

Long-term Care Insurance Options

Exploring long-term care insurance options is a critical step in mitigating future financial strain related to care costs. A myriad of insurance products exists, each designed to address diverse needs and income levels among retirees. When evaluating insurance, focus on policies that offer flexibility in terms of coverage settings, ranging from in-home care to full-time nursing facilities. This allows for customization based on individual preferences and financial situations, preserving your income and wealth longer.

Insurers often offer hybrid policies that combine long-term care coverage with life insurance, which can be a valuable option. These hybrid plans can provide benefits even if the long-term care coverage is not utilized, thereby safeguarding your total investment. Another approach involves considering policies with inflation protection to ensure that your coverage remains adequate as costs increase over time. It’s also essential to understand how your long-term care insurance impacts taxes, as certain tax benefits might be applicable depending on the policy’s structure.

When selecting long-term care insurance, assess the policy’s financial stability by evaluating the insurer’s ratings and history. Establish a comparative analysis of premium costs vs. benefits, and ensure it aligns with your financial planning goals. Consulting with a knowledgeable insurance agent can clarify the complexities surrounding long-term care policies, helping you to identify which options best fit your specific retirement needs. Through informed planning and an understanding of available insurance options, retirees can effectively lessen the risk of financial depletion due to unexpected long-term care costs, maintaining a more secure and comfortable retirement.

Managing Home Maintenance in Retirement

Retirees frequently underestimate the expenses linked to home maintenance, which can lead to financial strain. Maintaining a home involves ongoing costs, from routine upkeep to unexpected repairs, all of which can quickly add up and impact your savings and financial stability. For many, housing continues to be a significant part of their budget, prompting the need for prudent planning to control these expenses. This section will explore assessing home maintenance costs and provide practical tips for reducing these expenses during retirement, ensuring a manageable balance between housing needs and financial resources.

Assessing Home Maintenance Costs

Before diving into retirement, it’s crucial for retirees to comprehensively assess potential home maintenance expenses. Housing costs are a significant part of your budget, and failing to accurately estimate these can deplete more of your financial savings than expected. Think about routine maintenance like lawn care, HVAC servicing, and minor repairs, adding up quickly over time. One effective way to manage these costs is by creating a detailed home maintenance plan that outlines expected services and their associated costs. Services like pest control, gutter cleaning, and appliance maintenance should be routinely scheduled and funded to prevent larger, more costly problems from sneaking up later.

Another aspect often overlooked is the aging condition of your home, which directly influences maintenance costs. Older homes may require more frequent repairs or replacements, which can put a real dent in your financial and income reserves if not accurately accounted for. Conducting a professional home inspection can provide a better idea of potential future expenses, giving you a clearer understanding of how to allocate your financial resources. This type of planning is crucial for retirees aiming to maintain their household without succumbing to unexpected costs. Furthermore, considering energy efficiency upgrades can not only reduce ongoing utility expenses but also add to your home’s value while cutting down future maintenance costs.

Tax implications of home maintenance expenses can also be a boon. Understanding allowable deductions can enhance your financial plan, increasing savings through strategic tax management. Consulting with financial advisors can provide insight into optimizing these savings opportunities. By thoroughly assessing maintenance costs ahead of time, retirees can create a robust plan that covers all potential expenses, safeguarding their income and savings.

Practical Tips for Reducing Home Maintenance Expenses

Reducing home maintenance expenses can make a significant difference to a retiree’s financial outlook. One practical tip is conducting basic maintenance yourself when possible, saving on the labor costs of hiring professionals. Routine tasks such as changing air filters, cleaning gutters, and maintaining outdoor spaces can reduce the need for costly services. For retirees who prefer professional assistance, negotiating prices or seeking bundled services at a reduced rate is advisable. Many service providers offer discounts to retirees, providing a financial reprieve while ensuring home maintenance needs are met efficiently.

Additionally, prioritizing preventative maintenance over repair can significantly cut down expenses. Routine checks and timely upkeep of your home’s critical systems, like electrical and plumbing, are far less expensive than emergency repairs. Employing the use of technology, like home maintenance apps, can keep track of all scheduled services and alert when attention is needed, optimizing both financial planning and time management. Also, seeking sustainable solutions, like switching to energy-efficient appliances or utilizing green energy, often results in long-term savings both on utilities and maintenance costs.

For larger expenses that may require additional funding, consider financial products like home equity loans, which often provide favorable terms for retirees. However, these should be factored into your long-term financial and income plan to avoid undue burden. For comprehensive financial management, seeking advice from professional financial services can help tailor personalized strategies that enhance savings and minimize financial impact. Also, consider relocating to areas with a lower cost of living where housing expenses are diminished, freeing up more of your retirement income for other pursuits. Adapting these practical tips ensures retirees manage their housing expenses effectively, preserving crucial savings and bolstering financial security.

As you strategize for retirement in 2026 and beyond, it’s crucial to have a comprehensive view of potential expenses. While it’s easy to focus on visible costs like housing and travel, don’t overlook unexpected medical bills or the rising cost of out-of-pocket health care. An informed approach, paired with a flexible budget, can mitigate financial surprises, ensuring a more comfortable and secure retirement. Consider consulting with a financial advisor to tailor a plan that aligns with your unique goals and lifestyle, keeping you prepared for the evolving landscape of retirement expenses.

FAQ: The Expenses Most Retirees Still Underestimate

What are some underestimated expenses in retirement planning?

Many retirees often overlook expenses like healthcare, inflation, and leisure activities. These costs can significantly impact retirement savings if not adequately planned for.

How can unexpected healthcare costs impact retirement savings?

Unexpected healthcare expenses, including long-term care, can quickly deplete your retirement savings. It’s crucial to have a plan in place to address these potential costs.

Why is it important to establish an emergency fund during retirement?

An emergency fund acts as a financial buffer, allowing you to handle unforeseen expenses without dipping into your primary retirement savings.

What should retirees consider when planning for long-term care?

Retirees should consider long-term care insurance to cover potential costs. Evaluating your specific needs and available resources is crucial to plan effectively.

How can retirees manage home maintenance costs during retirement?

It’s important to have a home maintenance plan in place. This includes assessing potential repair costs and considering energy-efficient upgrades to manage expenses effectively.