Navigating Social Security decisions is critical as you approach retirement, choices made can have long-lasting impacts on your financial well-being. Once certain decisions are locked in, they can be challenging or even impossible to reverse. Understanding the consequences of these choices will empower you to make better-informed decisions to maximize your benefits. In this article, we’ll explore key Social Security decisions you need to get right the first time, ensuring you safeguard your financial future. So, whether you’re approaching retirement or planning ahead, these insights can help you achieve peace of mind and financial stability.

Brief Overview

Navigating Social Security decisions is crucial for retirees aiming to secure their financial future. Making informed choices about when to claim benefits, considering factors like full retirement age and potential tax implications, can greatly impact long-term financial stability. Avoiding common mistakes, such as claiming benefits too early or misunderstanding spousal benefits, is essential. Careful planning and possibly consulting with financial advisors can help retirees maximize their Social Security benefits, ensuring a stable and fulfilling retirement. Taking the time to strategize effectively can provide peace of mind and bolster financial security in the golden years.

Key Highlights

- Maximizing Social Security benefits involves strategic timing and understanding spousal and survivor options.

- Early Social Security claims may lead to reduced lifetime benefits and long-term financial effects.

- Consider the impact of taxation on Social Security to avoid unexpected financial setbacks.

- Understanding full retirement age can help increase monthly payouts and avoid penalties.

- Avoid common Social Security mistakes by planning thoroughly and consulting financial advisors.

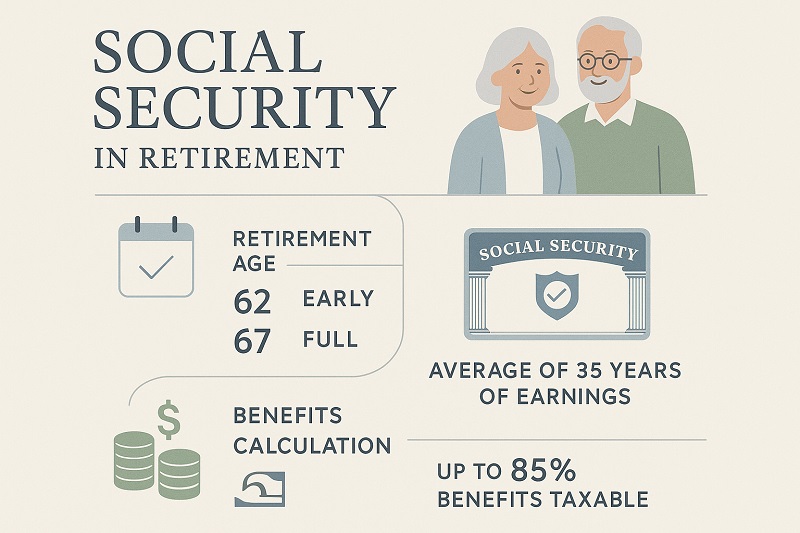

Understanding Social Security In Retirement

Social Security is a cornerstone of retirement planning, offering retirees a financial lifeline in their golden years. Understanding the intricacies of Social Security benefits is essential for making informed decisions. Whether it’s the timing of your claim or navigating full retirement age (FRA), each choice impacts your financial well-being. With insights into key social security decisions and a focus on avoiding common mistakes, retirees can safeguard their monthly benefit. This journey into personal finance requires careful planning and consideration to maximize the benefits and minimize irreversible decisions that could affect long-term financial stability.

Key Considerations for Social Security Decisions

Deciding when and how to claim Social Security benefits can significantly influence your retirement lifestyle. It’s pivotal to weigh several factors, such as your full retirement age (FRA), health, and overall financial strategy, before filing. Each choice dictates the monthly benefit you’ll receive, making it critical to approach these decisions with a comprehensive mindset. An early claim might seem tempting, offering immediate financial relief. However, it reduces your lifetime benefits, impacting your financial security in the long run.

Consulting financial advisors can provide insights into optimizing your benefits. They can aid in assessing whether delaying your claim post-FRA might behoove you, potentially increasing your monthly payouts. Additionally, understanding the potential filing penalties if you continue to work can save from unexpected financial pitfalls. Retirees must recognize that Social Security isn’t just about the immediate dollar amount but about maintaining a stable financial foundation through strategic planning.

Such informed choices ensure that your retirement benefits effectively support your lifestyle now and in the future. Evaluating your personal health circumstances and expected longevity also plays a role. If longevity runs in your family, delaying your claim often aligns with maximizing benefits. With a strategic approach and emphasis on avoiding common social security mistakes, retirees can ensure ongoing financial stability and peace of mind during their retirement years.

Common Social Security Mistakes to Avoid

Understanding and avoiding common social security mistakes is vital to maintain your financial foothold during retirement. One frequent error is underestimating the impact of incorrectly timing the start of your benefits. An early decision to claim can diminish the monthly benefit you’ve worked hard to accrue. It’s easy to be enticed by the thought of accessing funds as early as age 62, yet financially, this often means receiving reduced benefits over your lifetime. Another pitfall is not accounting for the potential tax implications on your benefits.

Many retirees overlook that their Social Security could be taxable depending on other income, leading to financial surprises. Planning those tax implications requires careful management of your income streams. Missteps also occur in misunderstanding spousal or survivor benefits, which form a crucial aspect of your financial planning. For married couples, coordinating the timing and strategy of when to claim can maximize total household benefits and enhance financial security.

Moreover, neglecting to incorporate potential changes in health expenses or lifestyle needs into your decision-making process can lead to funding gaps. A strategic review of your expenses, paired with awareness of your benefits, plays a crucial role in avoiding irreversible decisions. Continuous education and reassessment, alongside professional guidance, can further safeguard against unforeseen pitfalls. Embracing a proactive approach to your social security allows for adaptability and security throughout your retirement journey. Neglecting these aspects could leave you with irreversible decisions that erode financial stability and peace of mind.

Claiming Social Security requires careful navigation to maximize retirement benefits. Early filing can seem appealing but often leads to irreversible decisions that impact long-term financial stability. Determining the optimal retirement age involves understanding the interplay between full retirement age (FRA), financial strategy, and personal health. These factors help retirees avoid filing penalties and ensure that benefits align with their lifestyle needs. By evaluating these elements, investors can make informed choices that enhance their financial security and enjoy peace of mind during retirement.

The Impact of Claiming Benefits Too Early

Claiming Social Security benefits prematurely has a significant impact on those looking to secure their financial future during retirement.

Early claims typically result in reduced monthly benefits, which can affect one’s economic security. Although receiving funds as soon as 62 can be tempting, this decision often leads to a substantial decrease in lifetime benefits. Those who file early effectively lock in a lower payout, which is a crucial factor investors need to consider when planning their retirement income strategy. Financial advisors can provide valuable insights and assist in understanding the adverse effects of claiming early, especially since once the choice is made, it’s hard to reverse. It’s essential to consider the broader picture, such as potential penalties and the influence of each decision on financial stability.

Moreover, filing too soon can lead to unforeseen financial repercussions, particularly for those who continue working. Penalties might substantially reduce the benefits, negating the advantage of early access. Importantly, these irreversible decisions can shape the overall retirement plan, leaving retirees with a less stable economic foundation. Reflecting on personal health and expected longevity is another component to assess. For those anticipating a long retirement period, delaying claims can offer higher financial returns, securing a robust economic stance in the later years. Therefore, strategically planning the timing of Social Security benefits can significantly impact the sustainability of retirement income, safeguarding against potential financial shortfalls. Conclusively, evaluating both immediate needs and long-term effects can make all the difference in securing financial autonomy in retirement.

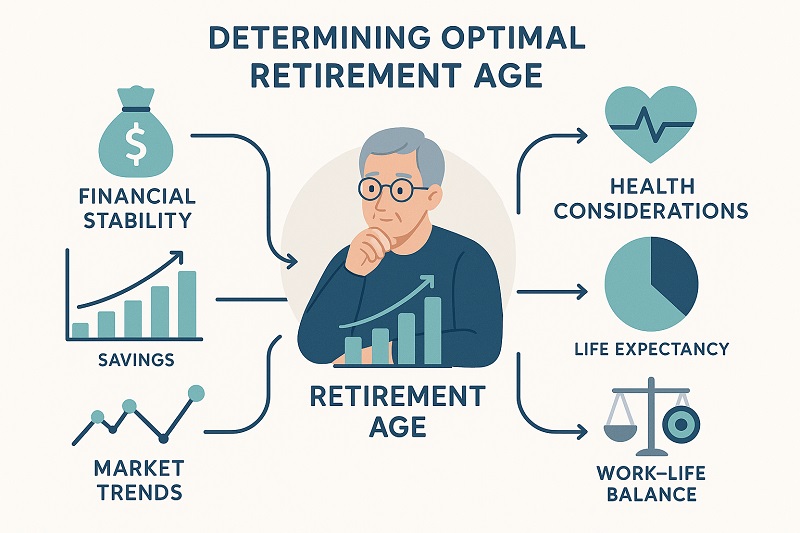

Strategies for Determining Optimal Retirement Age

Determining the optimal retirement age is paramount for maximizing Social Security benefits, allowing for a healthy financial standing throughout retirement. Starting with an analysis of Full Retirement Age (FRA), investors can better grasp the implications of timing and benefit optimization. FRA represents the age when one can claim their full Social Security benefits without penalties, typically ranging between 66 and 67, depending on the birth year. Delaying benefits beyond FRA often results in increased monthly payouts, offering significant long-term financial benefits. In contrast, early filings, though providing immediate financial relief, generally reduce overall benefits.

Advisors often recommend evaluating health and life expectancy when considering the timing of benefit claims. If longevity is in your genes or if your current health indicates a long retirement horizon, delaying retirement benefits can prove financially rewarding. Such a strategy increases lifetime benefits, providing a cushion against unforeseen future expenses. Furthermore, aligning retirement age decisions with spousal benefits can amplify household financial security. Married couples can benefit from synchronized claiming strategies, ensuring that both parties maximize their benefits and avoid losing potential payouts.

Planning extends beyond sheer number-crunching; it involves assessing lifestyle goals, anticipated retirement expenses, and potential income streams. By incorporating comprehensive financial management into retirement age strategies, retirees can avoid filing penalties and make choices that foster long-term economic stability. Effective planning can mitigate tax implications on benefits, letting retirees retain a greater portion of their income. As you navigate these choices, consulting with a financial advisor is a wise step. Their expertise can help in crafting a tailored approach, factoring in personal circumstances and ensuring benefits align seamlessly with your financial goals. Ultimately, a strategic approach to claiming Social Security bolsters financial freedom, aiding in a smooth transition into the golden years.

Exploring how to fine-tune your retirement strategy involves several key considerations:

- Assess your expected retirement lifestyle needs and related costs.

- Evaluate the impact of health care costs on overall retirement planning.

- Explore potential income sources to supplement Social Security benefits.

- Consider taxation of benefits depending on your total retirement income.

- Research the role of pensions and other retirement accounts in your plan.

- Analyze the benefits of annuities and other retirement income products.

- Contemplate the implications of working part-time during retirement.

These pointers can sharpen your strategy, ensuring a well-rounded approach to retirement planning.

Maximizing Social Security Benefits

Maximizing Social Security benefits isn’t just about when to start claiming; it’s a comprehensive strategy involving spousal and survivor benefits, as well as avoiding common oversights. Understanding these facets can ensure a secure financial foundation in retirement, enhancing your overall quality of life. The decisions you make about your Social Security payouts have profound impacts on your long-term security. With thoughtful planning and a keen eye for detail, retirees can maneuver through the complexities of these benefits, ensuring they make the most out of what they’ve earned.

How to Leverage Spouse and Survivor Benefits

Leveraging spouse and survivor benefits can significantly enhance the financial stability of retirees. These benefits are designed to provide security for households, ensuring that both partners maximize their social security entitlements. A keen understanding of how these benefits work can optimize your overall financial framework in retirement. For married couples, strategic planning around when each partner should claim benefits is crucial. Aligning these claims with your overall financial goals allows you to maximize the household income over the long term.

Spouse benefits primarily cater to households where one partner may not have a substantial work record. In such cases, a spouse might be eligible for benefits based on the other partner’s Social Security work record, often leading to a larger cumulative benefit. Understanding this can significantly impact your overall retirement planning, particularly if one spouse was a higher earner. Delaying the higher earner’s benefits could increase the future benefit size, adding long-term security.

Survivor benefits come into play after the death of a spouse. These benefits ensure that the surviving spouse receives the larger of the two Social Security payouts. This mechanism aims to provide some financial continuity, softening the impact of income loss after the loss of a partner. Misunderstanding survivor benefits and their timing can lead to financial pitfalls. Therefore, it’s crucial to incorporate them into your planning early on.

A comprehensive approach to these benefits includes a careful assessment of your household financial needs and overarching retirement goals. By being proactive and informed about the available options, retirees can avoid critical mistakes and secure a stable financial footing for both themselves and their spouses. Consulting with financial advisors can further illuminate opportunities to maximize these benefits strategically, ensuring a well-rounded approach to social security planning.

Avoiding Oversights in Security Decisions

Avoiding oversights in your Social Security decisions is essential to preserving your financial health in retirement. These benefits form the backbone of many retirees’ incomes, so ensuring every choice is well-informed and strategically planned is crucial. Missteps can lead to significant losses in potential benefits, affecting your retirement lifestyle and financial independence.

One of the most common oversights is failing to consider the impact of taxation on your Social Security benefits. Depending on your total income, a portion of your benefits could be taxable, which can surprise those unprepared for this eventuality. Planning your income streams and understanding how they interact with tax thresholds can mitigate unexpected tax burdens and preserve more of your retirement income.

Furthermore, many retirees overlook the strategic use of spousal benefits. The timing and method of claiming these benefits can significantly influence total household income. Failing to coordinate spousal benefits with a broader financial plan can result in lost opportunities for increased payouts. Planning with an eye on these details can ensure you take full advantage of what you’re entitled to, enhancing your overall financial security.

It’s also common to misunderstand the nuances of full retirement age (FRA) and its effect on monthly benefits. Claiming Social Security before reaching FRA typically results in a permanent decrease in monthly payouts, impacting the long-term financial picture. Conversely, delaying claims beyond FRA can increase monthly benefits , a strategy that should be considered if feasible.

Addressing these potential oversights early, with the help of advisors if necessary, can significantly enhance the effectiveness of your Social Security strategy. Ensuring that you are fully informed about your options avoids irreversible decisions and maximizes the sustainability of your financial resources. The right decisions can provide peace of mind and a stronger financial footing during your retirement.

Financial Planning and Security Mistakes

Navigating retirement with confidence requires a clear understanding of the common financial planning and security mistakes that many face. Social Security decisions play a vital role in ensuring steady income during retirement, yet several missteps can jeopardize one’s financial health. These mistakes range from underestimating tax implications to misunderstanding benefit coordination. By exploring effective strategies and avoiding these pitfalls, retirees can enhance their financial stability and maximize their benefits. Awareness and precision are essential in maintaining a secure financial foundation as you transition into retirement.

Mitigating Tax Implications on Social Security

For investors, understanding the tax implications on Social Security benefits is crucial to maintaining financial health in retirement. Many retirees underestimate the extent to which their benefits might be taxable, leading to unforeseen financial challenges. This oversight can materially affect one’s financial planning, as taxes can reduce the net income received from Social Security, threatening overall economic security. It’s important to recognize that your Social Security benefits may be subject to taxation if your total income exceeds specific thresholds. For example, if you’re filing as an individual and your combined income is over $25,000, your benefits may become taxable. For married couples filing jointly, this threshold is higher. Proper financial management and planning can help mitigate these taxes.

Partnering with financial advisors can provide valuable insights into strategies for reducing taxable income, such as adjusting the timing of withdrawals from retirement accounts. These advisors can guide you in structuring your income streams more effectively to minimize tax penalties. Additionally, incorporating investment strategies that focus on tax efficiency can bolster retirees’ financial security without sacrificing income. By consulting with professional advisors, retirees can employ strategies such as Roth IRA conversions or tax-efficient asset allocations that align with personal finance goals, effectively reducing tax implications on Social Security.

Balancing income streams to remain below taxable thresholds can be a practical approach to managing personal finance effectively. This strategy involves careful planning of other income sources, such as pensions or part-time work, to ensure that Social Security benefits remain as untaxed as possible. Moreover, considering the timing of claims in relation to other income sources can further refine your tax strategy. As you navigate these decisions, leveraging insurance products that offer tax-deferred growth might provide further opportunities to shield benefits from excessive taxation. Ultimately, an informed and strategic approach to managing Social Security’s tax implications can significantly enhance financial freedom and stability, ensuring that retirees make the most of their benefits.

Deciding when and how to claim Social Security benefits is a critical choice with lasting implications. With potentially irreversible outcomes, it’s wise to approach this decision with a well-informed strategy. Consider your financial needs, retirement age, and potential health scenarios to make the most out of your benefits. By thoroughly examining your options and perhaps consulting with a financial advisor, you can avoid common pitfalls and optimize your income in retirement. Remember, patience and careful planning can significantly enhance your financial security in your golden years.

FAQ: Social Security Decisions That Are Hard to Undo in Retirement