In 2026, middle-class families are discovering that a simple bill review can be their financial lifeline, saving up to $1000 each month. Amidst rising living costs, this strategy offers a lifeline by uncovering overlooked savings on everyday expenses. From renegotiating service fees to eliminating redundant subscriptions, these savings opportunities empower households to protect their budgets and build a more secure future. As investors and financially-minded individuals, understanding these cost-reduction strategies is key to maximizing wealth and ensuring financial stability. Join us as we delve into practical tips that can make a significant impact on your monthly bottom line.

Brief Overview

Middle-class families can save up to $1000 monthly by 2026 through strategic financial planning, including thorough bill reviews to uncover hidden expenses. Prioritizing effective bill management and leveraging savings accounts can enhance financial health while reducing monthly costs. Tax strategies, such as maximizing standard deductions, play a key role in minimizing tax burdens and freeing up funds for investment. Additionally, managing debt efficiently paves the way for financial freedom, while open family communications help align financial goals. Start building financial resilience with practical tips on savings and debt management—download our free guide today!

Key Highlights

- Thorough monthly bill reviews can save middle-class families up to $1000 by identifying hidden expenses.

- Effective bill management uncovers financial leaks, aligning funds with essential family goals.

- Utilizing the standard deduction and tax credits can reduce tax liabilities significantly.

- Debt management strategies help free up cash flow for savings and investment opportunities.

- Communication within the family ensures collective financial goals and optimized resource allocation.

Understanding the Importance of Bill Reviews

In today’s economy, reviewing your monthly bills is more crucial than ever. Middle-income families often find hidden expenses that can add up significantly. By effectively managing bills, families can achieve remarkable savings. This process not only impacts your immediate financial situation but also contributes to long-term financial goals. As middle-class taxpayers navigate these complexities, a strategic look at your bills can lead to substantial benefits. For investors, uncovering these potential areas of savings aligns with maximizing returns.

How Bill Reviews Can Identify Hidden Expenses

For many middle-income families, understanding where each hard-earned dollar goes is vital. A meticulous review of bills can reveal costs that often slip under the radar. These expenses, be it small subscription fees or unnoticed rate hikes, can be significant over time. The realization that these charges accumulate underscores the importance of a detailed bill review. For families seeking savings, pinpointing such hidden costs can result in considerable deduction opportunities.

Modern families juggling numerous obligations might overlook mischarges or forgotten subscriptions. Comprehensive bill assessments bring these issues into sharp focus. When actively engaged in a review, it provides the chance to negotiate better rates or eliminate unnecessary services. For middle-class families aiming for a budget-friendly lifestyle, these actions can lead to savings of thousands annually.

From an investment standpoint, trimming wasteful expenses effectively reallocates resources to more productive uses. This way, families contribute to a broader financial strategy. An investor recognizes these seemingly small tweaks as impactful steps toward financial efficiency. With more disposable funds due to reduced monthly bills, families can consider allocations to higher-return investments, enhancing their financial portfolio.

The keyword here is proactivity. By regularly scrutinizing household expenses, families remain well-prepared for financial challenges. It ensures a cushion during fiscally constrained periods. For any family aiming for financial resilience in 2026, periodic, thorough bill evaluations are not merely advisories, they’re essential. Taking this step fortifies financial health, allowing for tactical planning and future-ready strategies.

Having recognized the importance of uncovering hidden expenses, families can adopt a strategic approach to meticulously examine their bills and optimize their financial health.

- Start by collecting all bills and statements, reviewing each line item to spot any unfamiliar charges or recurring fees.

- Utilize budgeting apps or spreadsheets to methodically track every expense, ensuring even the smallest costs are accounted for and scrutinized.

- Contact service providers to negotiate better rates or eliminate unnecessary services, capitalizing on competitor offers or bundling options to reduce costs.

- Establish a routine billing review schedule, such as monthly check-ins, to stay vigilant and swiftly respond to any discrepancies or unnecessary expenditures that may arise.

By implementing these practical steps, families can significantly enhance their financial awareness and control, paving the way for sustained financial stability and reduced financial stress.

The Impact of Effective Bill Management on Families

Why does effective bill management prove pivotal for middle-income families? Quite simply, it creates a structured framework to handle finances efficiently. Regular monitoring and tracking of monthly expenses allows each family member to become a more informed participant in financial discussions. This holistic approach translates into substantial savings, ensuring that money saved on bills is money that can be redirected toward other family goals.

Through astute bill management, families often uncover steady areas of financial leakage, such as overlapping services or unused memberships. Redundant insurance policies or underutilized utilities can be rationalized, delivering immediate cost benefits. Such evaluations not only foster savings but hand families the tools to make educated decisions about future spending. Investors understand the importance of resource allocation, and likewise, families must allocate wisely to avoid financial pitfalls.

Furthermore, efficient bill management influences a family’s comprehensive financial well-being. Regular savings, even small ones accumulated from better bill management, add up significantly over time. Imagine if this approach led to saving hundreds monthly, over the years, such diligence could contribute to a considerable investment fund. Families committed to this level of management witness the dual benefits of having more available cash flow and an enhanced capacity for investment.

Lastly, the utility of consistent bill evaluations cannot be overstated for taxpayers looking to maximize their qualified deductions. As tax laws evolve, so do the opportunities to benefit from available deductions; meticulous record-keeping ensures no money is left on the table. With adept bill management practices, families can position themselves not only for present savings but for long-term financial stability, and that’s a wise investment indeed.

Strategies for Reducing Monthly Expenses by 2026

In the pursuit of financial stability, middle-class families can adopt strategies that significantly reduce their monthly expenses by 2026. Incorporating savvy financial planning techniques, such as optimizing savings accounts and leveraging tax benefits, can lead to considerable savings. By understanding the role of savings accounts and the impact of the standard deduction, families can methodically reduce their financial burden. These proactive measures align with an investor’s mindset, promoting long-term fiscal health and enhanced financial prosperity.

Maximizing the Benefits of a Savings Account

As 2026 approaches, a well-managed savings account becomes a vital tool for middle-class families aiming to bolster their financial situation. With economic trends shifting, savvy investors know that a savings account can offer both security and growth potential. By prioritizing contributions to such accounts, families not only exercise discipline but also prepare for unexpected financial challenges. These accounts serve as a foundation for financial planning, providing a buffer against economic volatility and offering opportunities for higher interest earnings compared to traditional checking accounts.

One strategy to maximize savings involves evaluating different account types. Some savings accounts offer better rates or terms that might align more closely with a family’s specific financial goals. For instance, high-yield savings accounts are designed to provide better returns on deposits, potentially doubling as both a savings refuge and an interest-generating mechanism. Middle-class savers should explore these options, comparing rates and terms to ensure that they are making informed decisions that bolster their savings strategy.

It’s also prudent for families to automate their savings. By setting up regular transfers from checking to savings accounts, families can instill a discipline that often results in accumulated wealth almost effortlessly. Additionally, reevaluating one’s monthly direct debits to incorporate a dedicated savings contribution ensures not just the growth of the principal but resilience during lean financial periods.

Moreover, taking advantage of tax benefits related to savings can prove financially savvy. For example, utilizing tax-advantaged accounts like IRAs or 529 plans can compound the benefits of saving by adding the potential for deferred tax liabilities. This multifaceted approach to savings does more than park funds for future use; it positions families to maximize wealth accumulation while minimizing tax burdens. Investors understand the dual advantage of growing savings while reducing taxable income, making this a strategic move towards robust financial health by 2026.

The Role of Standard Deduction in Reducing Tax Burden

The standard deduction is a powerful tool in the arsenal of any middle-class family seeking to reduce their tax burden. As tax season approaches each year, understanding how to utilize the standard deduction effectively can lead to significant savings on one’s tax return. In 2026, leveraging this deduction will become increasingly vital as tax policies evolve and financial landscapes shift.

Joint filers, in particular, can benefit greatly from the standard deduction, as it allows them to simplify their tax filing process while reducing taxable income significantly. By opting for the standard deduction, families may sidestep the often cumbersome task of itemizing each potential deduction. This streamlined approach not only saves time but ensures they capitalize on an increased deduction limit, which is adjusted annually based on inflation rates.

Awareness of the changing limits and provisions surrounding the standard deduction is crucial for maximizing its benefits. As an investor, staying informed of these changes enables families to plan effectively, aligning their financial decisions with tax-advantaged outcomes. A well-considered application of the standard deduction can free up funds that would otherwise go to tax payments, allowing for reinvestment in savings accounts, education funds, or debt reduction.

For families who also manage credit cards or have an auto loan, understanding the intersection of the standard deduction with other deductions is essential. While itemizing can sometimes yield higher deductions, the broad application of the standard deduction often covers the majority of what families need to minimize their tax liabilities. By strategically incorporating savings account deposits and proactive financial planning into their annual budgeting, families can ensure they’re optimizing their taxable status and preparing for future fiscal goals.

Ultimately, the standard deduction serves as a cornerstone for tax planning, offering a simple yet effective means to reduce taxable income and enhance savings potential. Families who embrace this efficient tax strategy by 2026 can enjoy a profound impact on their overall financial health, yielding both immediate tax savings and long-term investment opportunities. Such an approach underscores the wisdom of aligning one’s financial strategies with evolving tax incentives, securing a stable and prosperous financial future.

As middle-class families tackle financial hurdles, tax planning becomes pivotal to maximizing savings and reducing financial strain. Understanding the impact of taxes and timely decisions can safeguard against unnecessary expenses. From grasping key tax considerations to the importance of filing on time, optimizing tax strategies can significantly enhance financial stability. Investors appreciate the benefits of proactive tax management, as it aligns closely with long-term fiscal goals and minimizing liabilities. This balanced approach not only aids in immediate savings but also builds resilience against future economic uncertainties.

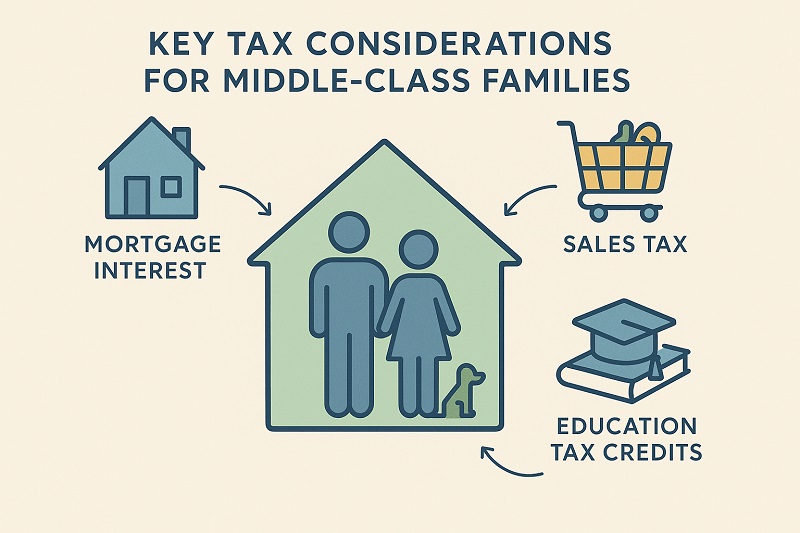

Key Tax Considerations for Middle-Class Families

For middle-class families, understanding tax considerations is essential to manage finances efficiently and capitalize on potential savings. The standard deduction stands out as a critical factor, offering a streamlined way to reduce taxable income. For many taxpayers, opting for the standard deduction simplifies the filing process by eliminating the need to track deductible expenses. This option can offer significant savings, especially for those who might not have enough deductions to surpass the standard amount. It’s crucial for families to stay informed about yearly changes to the deduction limits, as these directly influence the potential tax benefits.

Families should also be aware of various tax credits available, which can further reduce their tax liabilities. Credits like the Child Tax Credit and Earned Income Tax Credit (EITC) can provide substantial savings, especially for those with dependents or lower income brackets. Unlike deductions that reduce taxable income, credits directly lower the tax owed, making them particularly valuable. Knowing which credits apply to their situation allows families to reduce their overall financial burden significantly.

In addition to deductions and credits, proper tax planning involves long-term strategies. Effective planning not only addresses immediate tax needs but also aligns financial decisions with future goals. For instance, contributing to retirement accounts such as IRAs or 401(k)s can reduce taxable income while simultaneously growing savings. These contributions often qualify for deductions, further enhancing their value. Families might also explore Health Savings Accounts (HSAs), which offer tax advantages for healthcare-related expenses.

Investors recognize these strategies as smart measures to optimize financial health and increase overall wealth. By understanding and leveraging available tax benefits, families can ensure they don’t miss out on potential savings. This comprehensive approach to tax considerations enables middle-class families to manage their resources more effectively, allowing for a balanced financial strategy that supports both current and future fiscal objectives.

The Importance of Timely Tax Filing

Filing taxes on time is more than a legal requirement; it’s a vital aspect of maintaining financial health for middle-class families. Timely filing helps avoid costly penalties and interest charges, ensuring that more of your hard-earned money stays in your pocket. By addressing tax obligations promptly, families can better manage their finances and allocate funds towards other crucial areas like savings or debt reduction.

Investors understand that efficiently handling tax matters aligns with broader financial management principles, reinforcing fiscal stability.

One crucial advantage of timely filing is the opportunity to plan financial activities around tax refunds. For many taxpayers, receiving a tax refund can significantly impact financial planning for the year. This influx of funds can be directed towards paying down debts, contributing to savings accounts, or investing in long-term goals. By filing early, families not only expedite their refund process but also have the chance to make proactive decisions about how best to utilize these funds.

Moreover, timely tax filing is an opportunity to review previous year’s finances, identifying areas where adjustments may be necessary. This review can highlight wasteful spending or uncover potential deductions and credits overlooked in previous years. For instance, families may recognize unclaimed deductions, such as charitable contributions or education expenses, which can be used to their advantage in the current tax year. This reflective process empowers families to make adjustments that address financial inefficiencies, enhancing overall budgeting strategies.

Lastly, consistent adherence to tax deadlines builds a disciplined financial routine. This routine assists families in managing their resources more predictably and with less stress. It ensures that taxes don’t become a frantic, last-minute scramble, but rather a managed aspect of an annual financial plan. For investors, this methodical approach to tax management exemplifies financial prudence, supporting both stability and growth over time.

In essence, timely tax filing equips middle-class families with the tools needed to navigate their financial landscape effectively. By incorporating proactive filing strategies into their annual routine, families can minimize tax-related stress and leverage financial opportunities that promote long-term security and prosperity. As families align their tax practices with other financial objectives, they lay a strong foundation for a resilient and successful future.

Managing Debt for Financial Stability

Managing debt effectively is crucial for ensuring financial stability in the middle class. As families face various financial obligations, understanding the nuances of debt management can pave the way for significant monetary savings. From reducing liabilities associated with auto loans to leveraging debt management strategies, the journey toward achieving financial freedom by 2026 can be systematically achieved. Employing these approaches can not only relieve financial pressures but also enhance the overall potential for investment and savings. With a clear plan, middle-class families can turn financial management into a tool for building a prosperous future.

Evaluating the Costs of an Auto Loan

Auto loans often represent a significant portion of a family’s monthly expenses, making it essential to evaluate their costs thoroughly. For many investors, a critical look at the terms and conditions of an auto loan can reveal opportunities for significant savings. The interest rates, loan duration, and types of fees associated with an auto loan must be critically assessed to ensure that families are not overspending. With interest rates projected to shift by 2026, evaluating these costs today can safeguard families from future financial strain.

Starting with the interest rates, families should evaluate whether their current rate is competitive. Refinancing might be a viable option if there’s potential for lower rates, leading to reduced monthly payments and significant money savings over the life of the loan. Additionally, exploring options for shortening the loan term can lower the amount of interest paid, though this involves higher monthly payments. Understanding the balance between interest cost and monthly obligation is key to making informed decisions.

Beyond interest rates, it’s important to consider additional fees associated with auto loans, such as origination fees or prepayment penalties. Families might find themselves paying extra if they haven’t closely examined these terms. By negotiating with lenders or opting for loans without such fees, families can save money on their auto loans. Over time, these savings can be redirected to essential areas like savings accounts or allocated to other investments to boost the family’s financial health.

Finally, a frequently overlooked aspect is the potential benefit of consolidating debts, including auto loans. By wrapping them into a single, lower-rate loan, families can simplify their financial obligations, potentially seeing thousands in annual savings. To maximize these benefits, regular reviews and adjustments of the family’s financial strategy are crucial. Evaluating auto loans not only sharpens the family’s financial insight but also strengthens their capability to achieve greater financial freedom well before 2026. These strategic considerations enable families to meet unexpected challenges and foster a proactive financial stance.

How Debt Management Can Lead to Financial Freedom by 2026

Entering the realm of debt management can seem daunting, yet its successful implementation is a pathway to financial freedom, especially for those targeting significant savings by 2026. Middle-class families, often juggling multiple financial responsibilities, can harness debt management techniques to optimize their financial health and achieve greater economic stability. Effective debt management strategies not only provide relief from immediate financial pressures but also pave the way for long-term savings and investment opportunities.

One critical element is understanding the potential synergy between debt reduction and savings. By prioritizing high-interest debts such as credit cards or loans, families can actually free up monthly cash flow, which can then be directed towards savings or investments. A balanced strategy includes listing all debts by interest rate and focusing repayments on the highest rates first. This approach reduces the total interest paid over time, offering substantial savings that build financial resilience over the years.

Tax advantages, too, play a significant role in debt management. Families comparing deductions, whether through the standard deduction or itemizing, should assess how these impact their tax liabilities and ultimately, their debt repayment capacity. Investing in retirement accounts or making deductible investments can further reduce taxable income, enhancing the family’s ability to manage debts. Understanding the interplay of taxes and debt can result in an optimized financial blueprint that aligns with long-term goals.

Engaging in regular financial reviews is another essential tactic. These reviews allow families to assess their progress toward debt reduction targets and refine strategies as needed. External factors, like changing interest rates or economic conditions, can influence debt management plans, making it vital for families to remain adaptable. By setting achievable milestones, families can maintain motivation and focus, vital elements for enduring the often challenging journey to debt freedom.

Investors approach debt management as a powerful growth strategy. By reducing liabilities efficiently, families can shift focus toward wealth-building opportunities, such as investing in equities or expanding retirement portfolios. This shift not only enhances financial freedom but also fortifies families against economic downturns. As 2026 draws nearer, the foresight provided by debt management serves as a foundational pillar for financial growth and security, amplifying a family’s potential to enjoy their wealth and plan ahead with confidence.

Leveraging Family Resources for Financial Success

Families aiming for financial success often overlook the power of leveraging internal resources. Communicating effectively within the family can set the foundation for achieving shared financial goals. By aligning on savings strategies, budget management, and understanding the impact of taxes, families can use their collective strength to achieve financial stability. Engaging every family member in open discussions about financial planning ensures informed decisions that align with long-term aspirations, such as reducing tax burdens. As investors know, the unity of purpose unlocks potential prosperity, making family collaboration an essential asset in financial endeavors.

Communicating Financial Goals Within the Family

Communication is the cornerstone of any successful financial plan, especially for middle-class families. When it comes to setting financial goals, it’s not just about the numbers; it’s about fostering an environment of openness and participation. Start by having regular family meetings to discuss financial objectives. This encourages transparency and ensures that every family member is part of the conversation. It’s crucial to set both short-term and long-term goals. For instance, a short-term goal might be to reduce utility bills by a certain percentage, while a long-term aim could focus on maximizing deductions from tax filings. By establishing clear targets, families can work collectively to achieve savings and minimize their tax burden.

Bridging generational gaps is also key in these discussions. Younger family members might have a different outlook on saving and spending, heavily influenced by digital trends and social media. Meanwhile, older members may have insights on traditional saving methods and tax strategies that have stood the test of time. Bringing these perspectives together allows for a comprehensive plan that respects diverse viewpoints while aiming for a common financial future. This inclusivity is critical, especially as financial decisions often involve sacrifices and shifts in lifestyle.

Another aspect of effective communication is education. Ensure all family members understand how tax laws affect their financial goals. This could include the importance of filing taxes on time, the benefits of different tax credits (like the Earned Income Tax Credit), and how deductions work. Providing this knowledge empowers everyone involved, highlighting why certain financial decisions, such as saving with the aid of tax-advantaged accounts, are made. Knowing the ‘why’ behind financial strategies can inspire younger members to take a proactive approach in contributing to the family’s economic plans.

Additionally, it’s essential for families to agree on a budget and stick to it. A budget functions as a financial roadmap, guiding spending and savings according to pre-established goals. Allocating funds towards essentials, like maintaining a savings account or paying off high-interest debt, should be prioritized. Families might find tools like budgeting apps helpful in tracking spending, ensuring that everyone is accountable and spending aligns with the shared objectives.

Investors often look for growth opportunities, and internal family resources can function similarly. By creating a strong communication network and mutually understood financial ambitions, families can cultivate an environment conducive to financial health. Structured family dialogues about spending, saving, and taxes can lead to significant deductions in unnecessary expenses and optimize resource allocation. Thus, an effective family communication strategy is not merely about discussing money but creating a culture that values informed financial decisions, paving the way for a prosperous future.

In 2026, the power of simple bill reviews can’t be overstated for middle-class families looking to bolster their savings. By staying informed and proactive about your monthly expenses, you can uncover hundreds or even thousands of dollars in potential savings. Start by examining routine bills, negotiating better rates, and prioritizing essential services. The journey to financial empowerment begins with these small steps, ultimately leading to greater financial security and freedom. For more strategic tips in reducing household expenses effectively, download our free guide today and pave the way towards a more financially stable future.

FAQ: Monthly Bill Review To Unlock Significant Savings in 2026

What is the benefit of reviewing monthly bills for middle-class families?

By reviewing monthly bills, middle-class families can identify hidden expenses and save up to $1000 each month. Effective bill management uncovers financial leaks and ensures alignment of funds with essential family goals.

How can families maximize their savings through tax strategies?

Families can maximize their savings by understanding and utilizing the standard deduction and available tax credits, which can significantly reduce their tax liabilities. Awareness of these opportunities helps free up funds for investment and savings.

Why is open family communication essential in achieving financial goals?

Open family communication ensures that all family members are aligned with financial goals and strategies. By discussing budgets, savings, and tax impacts, the family can make informed decisions that optimize resource allocation.

What role do savings accounts play in enhancing financial health for families?

A well-managed savings account offers security and growth potential, serving as a foundation for financial planning. By prioritizing contributions and exploring high-yield options, families can prepare for unexpected challenges and boost their financial prosperity.

How can debt management contribute to financial freedom?

Effective debt management, including focusing on high-interest debts and exploring refinancing or consolidation options, can free up cash flow for savings and investments. This approach supports long-term financial stability and growth potential.